Master limited partnerships (MLPs) combine the tax benefits of a limited partnership with the liquidity of common stock. Understanding the best MLP stocks is essential for investors seeking high-yield opportunities. They are organized as publicly traded partnerships (PTPs), meaning their securities are traded on national exchanges in the USA.

The legal basis for the existence of MLPs is the Tax Reform Act and the Revenue Act, enacted in 1986 and 1987 respectively. The main requirement for using this form of ownership is that at least 90% of the income is derived from activities in sectors such as:

- natural resources (e.g., pipeline operators);

- energy, energy infrastructure;

- commodities;

- real estate.

Despite high yields and tax-deferred distributions, the number of MLPs has declined in recent years due to legislative changes and investor interests. Many of these companies have restructured into C-corporations.

This article provides an overview of publicly traded limited partnerships with information on dividend yields and Dividend Safety Scores.

Table of Contents

Key Takeaways About MLPs

- MLP is a company that exists in the form of a publicly traded partnership. This structure offers tax advantages.

- The general partner manages the operations of the MLP, while investors are classified as limited partners.

- MLP distributions are primarily tax-sheltered distributions. Therefore, MLP shares are considered a reliable long-term income stream and low-risk investments.

- Most MLPs operate in the real estate sectors, natural resources, and energy sectors.

Tax Benefits of MLPs

Unlike commercial companies, master limited partnerships (MLPs) are organized as pass through entities. They are not subject to double taxation and are therefore exempt from paying corporate tax. All tax liabilities are passed on to unitholders. Each unitholder receives an annual K-1 statement, which contains the information necessary for tax purposes with respect to their income.

Note! Distributions from LPs represent distributable cash flow (DCF). This is similar to free cash flow (FCF). Therefore, unlike dividends, these distributions are not taxed in the year they are received. MLP shareholders benefit from the tax deferral as the distributions are treated as a return of capital which reduces their cost basis.

As a result, taxable income is only 10-20% of the total amount received. The remainder falls into the category of return of capital due to depreciation and other tax deductions. This method of tax optimization is particularly advantageous for pipeline companies in the oil and gas industry.

Historical Context of MLPs

The first MLP was established in 1981. Just six years later, Congress imposed limitations on such entities. Qualifying income required to maintain tax benefits may include profits from real estate, natural resources and energy activities. The changes were prompted by concerns about a sharp decline in budget revenues from corporate tax revenue.

MLP Cash Flows and Taxes

Let’s consider an example with the following assumptions:

- MLP shares are purchased for $100.

- Each year, the investor receives cash distributions of $6. Of this amount, $1.2 is the allocation of taxable income, and $4.8 is the return of capital, which reduces the cost basis.

- The master limited partnership units are sold after 3 years for $120.

- The individual income tax rate for the investor is 15%, and the capital gains tax rate is 22%. !

As a result of the cash distributions each year, the investor must pay the IRS $0.26 ($1.2 x 22%).

When investors sell MLPs, the tax is determined as follows:

- The capital gain is the difference between the original cost basis and the sale price, which amounts to $20. The tax on this gain is $3 ($20 x 15%).

- The reduction in cost basis totals $14.4 ($4.8 + $4.8 + $4.8). The deferred taxes amount to $3.17 ($14.4 x 22%).

Estate planning is possible with limited partnership units. When transferring units to an heir, accrued tax liabilities disappear. The heirs are tax free on the liabilities accumulated by the deceased.

A Quick Note on MLP Taxes

Most MLPs issue K-1 forms rather than 1099s, which comes with tax complexity. Many investors find it difficult to complete their tax returns.

The cost basis is recalculated annually. If it falls to $0, the investor must pay tax annually on the entire amount received from the MLP.

MLPs are considered suitable investments for taxable accounts because the return of capital is not taxed in the year it is received. However, such investment vehicles may result in tax liabilities in tax-sheltered accounts (IRAs).

Diversification Benefits

Master limited partnerships (MLPs) have a low correlation to asset classes such as stocks, bonds, commodities, real estate investment trusts (REITs), S&P 500 index funds, and others. They are therefore considered to be good diversifiers.

Such assets allow the unsystematic risk of the portfolio to be reduced. At the same time, the expected return remains at the same level. There is also the opportunity to invest directly in a portfolio of MLPs that is already diversified across sectors.

Higher Yields

LPs typically operate in slow-growing, capital-intensive industries, such as pipeline construction. These MLPs provide relatively slow investment returns compared to the financial sector.

However, they have long-term service contracts and generate stable income. Due to their flow-through entity structure and tax benefits, MLPs retain more funds for future projects.

As a result, in most cases, the growth rates of cash distributions from LPs outpace inflation. Combined with remaining tax deferred, this provides returns that exceed the dividend yield of many publicly traded companies.

2026 MLP List by Yield

| Ticker | Name | Industry | Dividend Yield | Safety |

| IEP | Icahn Enterprises L.P. | Conglomerates | 33.74% | Dangerous |

| UAN | CVR Partners, LP | Fertilizers and Crop Inputs | 13.49% | Safe |

| CAPL | CrossAmerica Partners | Midstream Services | 11.90% | Carefully |

| GHI | Greystone Housing Impact Investors LP | Real Estate Financing | 10.87% | Unsafe |

| ARLP | Alliance Resource Partners | Coal and Consumable Fuels | 9.37% | Very safe |

| AB | AllianceBernstein Holding L.P. | Asset Management and Custody Banks | 8.91% | Very safe |

| DKL | Delek Logistics Partners, LP | Midstream Services | 8.68% | Safe |

| BSM | Black Stone Minerals | Oil and Gas Production | 8.64% | Very safe |

| WES | Western Midstream Partners | Midstream Services | 8.38% | Safe |

| WLKP | Westlake Chemical Partners LP | Commodity Chemicals | 8.15% | Very safe |

| MPLX | MPLX | Midstream Services | 7.62% | Safe |

| USAC | USA Compression Partners | Oil and Gas Equipment and Services | 7.54% | Safe |

| PAA | Plains All American Pipeline | Midstream Services | 7.39% | Carefully |

| ET | Energy Transfer | Midstream Services | 6.96% | Safe |

| DMLP | Dorchester Minerals, L.P. | Oil and Gas Production | 6.91% | Very safe |

| SPH | Suburban Propane Partners | Gas Utilities | 6.75% | Carefully |

| GLP | Global Partners | Midstream Services | 6.23% | Safe |

| SUN | Sunoco | Oil and Gas Refining and Marketing | 5.98% | Safe |

| EPD | Enterprise Products Partners | Midstream Services | 5.82% | Safe |

| CQP | Cheniere Energy Partners | Midstream Services | 4.90% | Safe |

| BIP | Brookfield Infrastructure Partners | Multi-Utilities | 4.69% | Safe |

| GEL | Genesis Energy, L.P. | Midstream Services | 4.61% | Unsafe |

| BEP | Brookfield Renewable Partners | Renewable Electricity | 4.29% | Borderline Safe |

| NRP | Natural Resource Partners L.P. | Coal and Consumable Fuels | 2.84% | Unsafe |

| NEN | New England Realty Associates Limited Partnership | Real Estate Operating Companies | 2.67% | |

| MMLP | Martin Midstream Partners L.P. | Midstream Services | 0.95% | Very dangerous |

| NGL | NGL Energy Partners | Midstream Services | ||

| USDP | USD Partners LP | Midstream Services |

Potential Yield Levels

The potential yields of individual MLPs can reach 10%. This exceeds the highest dividends of stable payers (Dividend Aristocrats and Kings).

MLP Partnership Structure

Master Limited Partnerships (MLPs) have two components. The first part of the structure of the MLP is the limited partners. These are investors who buy units and receive income. The second component is the general partner. The general partner manages the business, has rights to incentive distribution rights (IDRs) and receives performance-based pay based on results. The measure of success is the cash distributions to the limited partners.

The simplest IDR structure with distribution levels is as follows:

- for income per unit of less than $1 per year, the general partner receives 2% of total cash distributions;

- for a range from $1 to $2, they receive 20%;

- for income over $2, they receive 50%.

Thus, as income per unit increases, the general partner receives a higher marginal IDR payment split.

In reality, the corporate structure of an MLP can be more complex, as can the IDR scheme. For example, Energy Transfer owns the general partner, USA Compression Partners, as well as approximately half of the total units.

General Partner Payment Calculation

IDRs depend on the LP distribution. This provides a financial incentive for quality management.

The formula for calculating the general partner’s payment in LPs is as follows:

(LP distribution ÷ limited partner’s IDR) × general partner’s IDR.

For example, if the cash distributions amount to $1 per unit and there are a total of 1000 MLP units, then the general partner will receive approximately $20.4 (($1000 ÷ 0.98) × 0.02).

In more complex cases, a general partnership may be publicly traded and have a general partner that is itself divided into two structures.

MLP Investor Suitability

Master Limited Partnership (MLP) shares are primarily purchased by private-client wealth managers. This investment vehicle is not in high demand due to low institutional ownership and limited sell-side attention. The reason is that mutual funds run the risk of receiving K-1 statements later than they should be providing Form 1099s.

Tax-exempt institutional investment funds (such as pensions, endowments and 401(k) plans) cannot own such assets. MLP distributions are classified as unrelated business taxable income (UBTI). This is income that is unrelated to the activities that grant tax-exempt status.

For the same reason, individual investors can only buy shares in a standard brokerage account. You receive current income with tax deferral. Buying through an IRA results in additional taxes.

Downsides to MLP

There are negative aspects and risks associated with investing in shares of Master Limited Partnerships (MLPs):

- Market volatility. The energy sector is particularly vulnerable. If oil prices or natural gas prices fall, the value of MLP shares also falls.

- Declining revenues. MLPs typically have limited access to capital markets. They cannot borrow at the same rate as leading corporations, which means they are forced to resort to distribution cuts during downturns.

- Regulatory risks and legislative risks. The benefits of the tax treatment can be revoked at any time due to changes in the tax structure.

- Interest rate risk. In this case, MLPs will face increased borrowing costs and decreased profits. Additionally, fixed-income assets will become more attractive to investors, which will also lead to a decline in the price of the MLP units.

Types of MLPs by Industry Sector

Below is a MLP list broken down by industry sectors. Tax issues have also been taken into account. The list does not include MLPs that do not issue K-1s. Over-the-counter traditional partnerships are excluded due to low liquidity.

It should also be noted that 2 of the listed MLPs do not pay a distribution. These are NGL Energy Partners (NGL), Steel Partners Holdings (SPLP), and USD Partners (USDP).

Top 5 MLP Stocks for High Dividends

The best MLP stocks offer high dividends. The yield reaches 10%. This is due to a durable business and stable income that provides distribution support. However, the highest-paying dividend stocks may have low safety ratings.

Oil and Gas Pipeline MLPs

Oil and gas pipeline MLPs own transportation pipelines, terminals, and storage facilities. They enter into long-term contracts with minimum volume commitments. These are fixed-fee contracts.

Often, refining companies establish such partnerships to optimize the management of logistics assets. For example, MPLX was created by Marathon Petroleum.

Oil and gas pipelines limited partnerships:

- Enterprise Products Partners;

- Energy Transfer;

- Plains All American Pipeline;

- MPLX;

- Delek Logistics Partners;

- Genesis Energy.

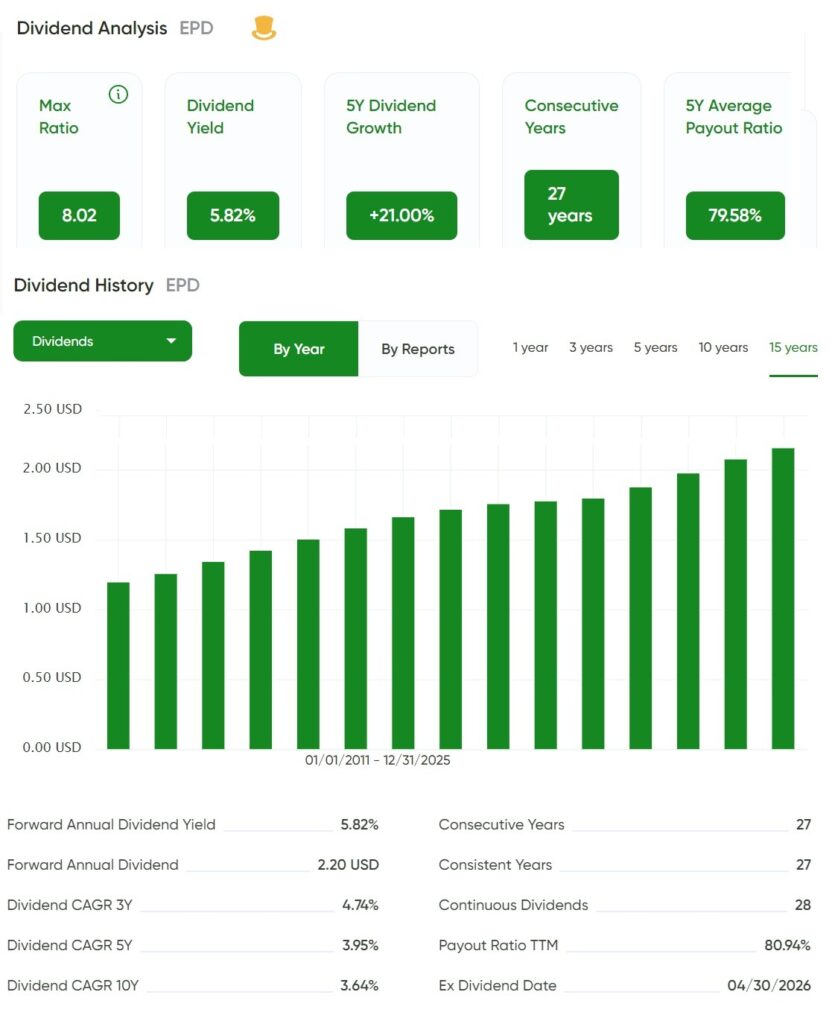

Enterprise Products Partners

- Sector: Energy – Oil and Gas Pipelines

- Dividend Yield: 5.82%

- Dividend Safety: Safe

- Uninterrupted Dividend Streak: 27 years

Enterprise Products Partners (EPD) provides a full range of midstream services. The entity’s operations include gathering, pipeline transportation, processing, and storage of natural gas, crude oil, and petroleum products. The majority of revenue comes from fixed-fee contracts. Enterprise Products Partners has an A- credit rating.

This MLP has the longest track record.

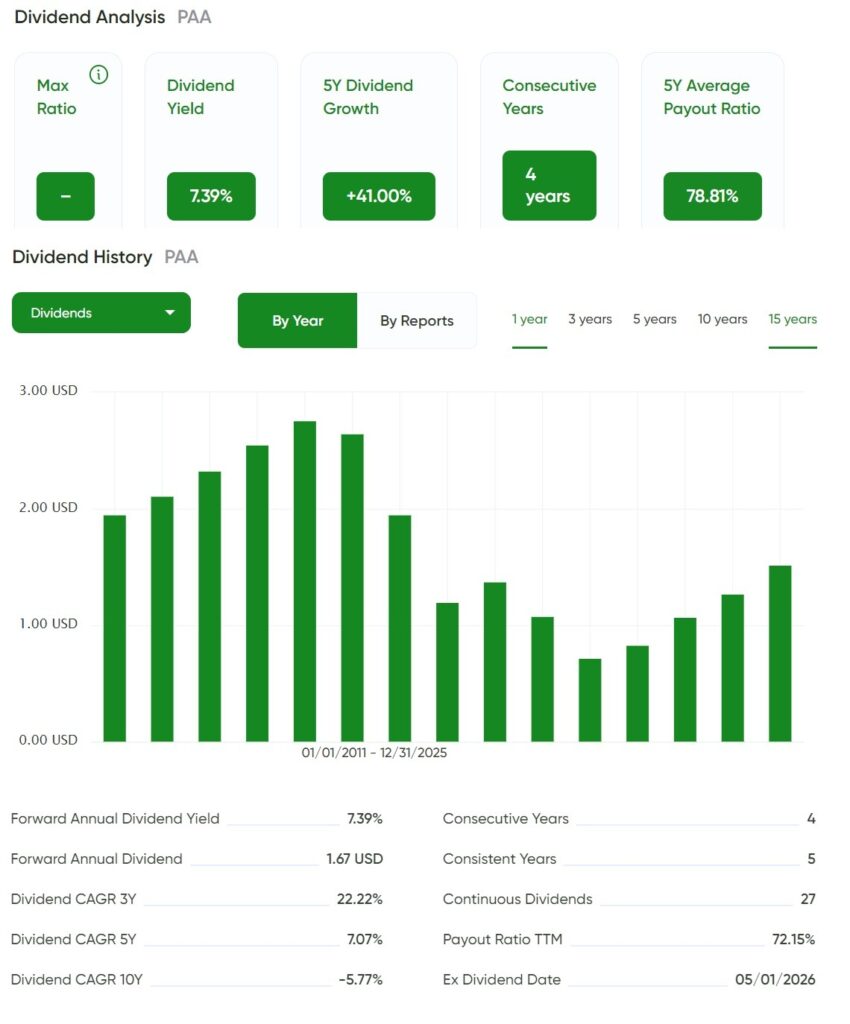

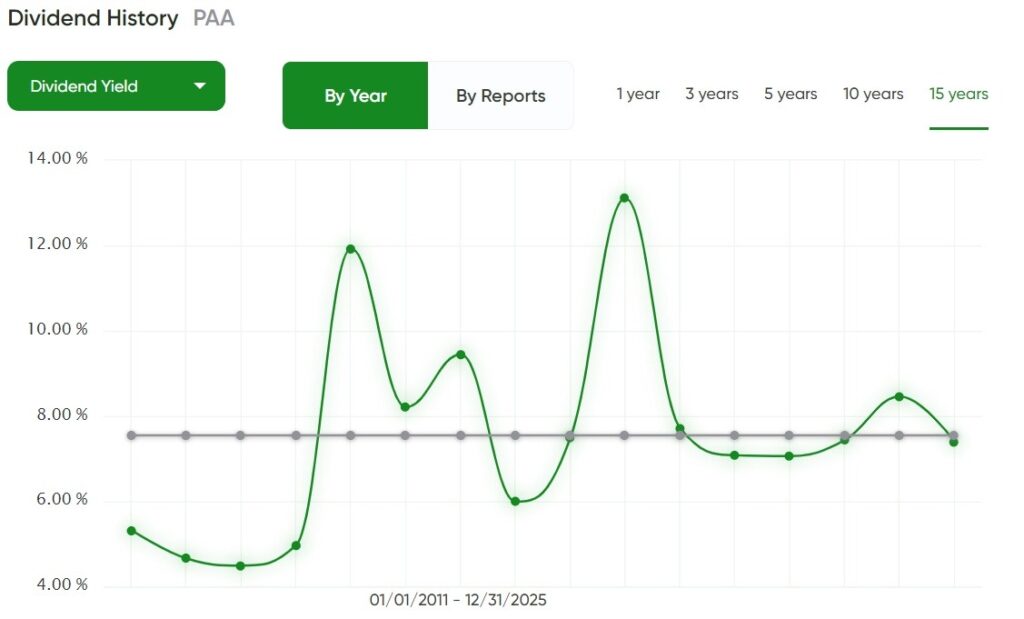

Plains All American Pipeline

- Sector: Energy – Oil and Gas Pipelines

- Dividend Yield: 7.39%

- Dividend Safety: Carefully

- Uninterrupted Dividend Streak: 4 years

Plains All American Pipeline (PAA) owns an extensive network of oil and gas pipelines and storage facilities connected to major production basins. However, more than half of the gas MLP’s revenues come from production in the Permian Basin.

The MLP’s cash flow is supported by fee-based contracts with minimum volume commitments.

Oil and Gas Gathering and Processing MLPs

This is the first link in the midstream process. Gathering and processing MLPs (G&P MLPs) gather natural gas and oil and transport it through their pipelines to processing points.

The contracts provide for fixed fees for field services. This measure ensures cash flow reliability. The volumetric risk lies in the fact that fewer wells are developed during downturns. Therefore, there is a possibility of distribution cuts.

The best MLPs engaged in gathering and processing include:

- Western Midstream Partners;

- USA Compression Partners;

- NGL Energy Partner.

Other Midstream MLPs

Midstream MLPs operate in the energy sector. They may produce liquefied natural gas, own storage terminals, and more. However, they do not engage in gathering or transportation. Cash flows are typically secured by take-or-pay contracts. For example, USD Partners previously has had distribution cuts to avoid increasing debt to its balance sheet.

Midstream LPs:

- Cheniere Energy Partners;

- USD Partners;

- Martin Midstream Partners.

Cheniere Energy Partners

- Sector: Energy – Other midstream

- Dividend Yield: 4.09%

- Dividend Safety: Safe

- Uninterrupted Dividend Streak: 18 years

Cheniere Energy Partners processes natural gas and owns LNG terminals. CQP generates steady cash flow through long-term fixed fee contracts with take-or-pay provisions.

A strong positive factor is the growing demand for natural gas liquids.

Infrastructure and Renewable Energy MLPs

Infrastructure MLPs and renewable energy MLPs utilize diverse business models. This includes not only energy infrastructure but also data centers and toll roads.

For example, Brookfield Infrastructure Partners owns assets such as transmission lines, railways, ports and pipelines. Meanwhile, Brookfield Renewable Partners has a portfolio of hydro, wind, solar and storage assets. Both companies were spun off from Brookfield Asset Management, which is now their general partner.

Long-term contracts provide these partnerships with regulated cash flows. These MLPs offer annual distribution growth of 5%-9%.

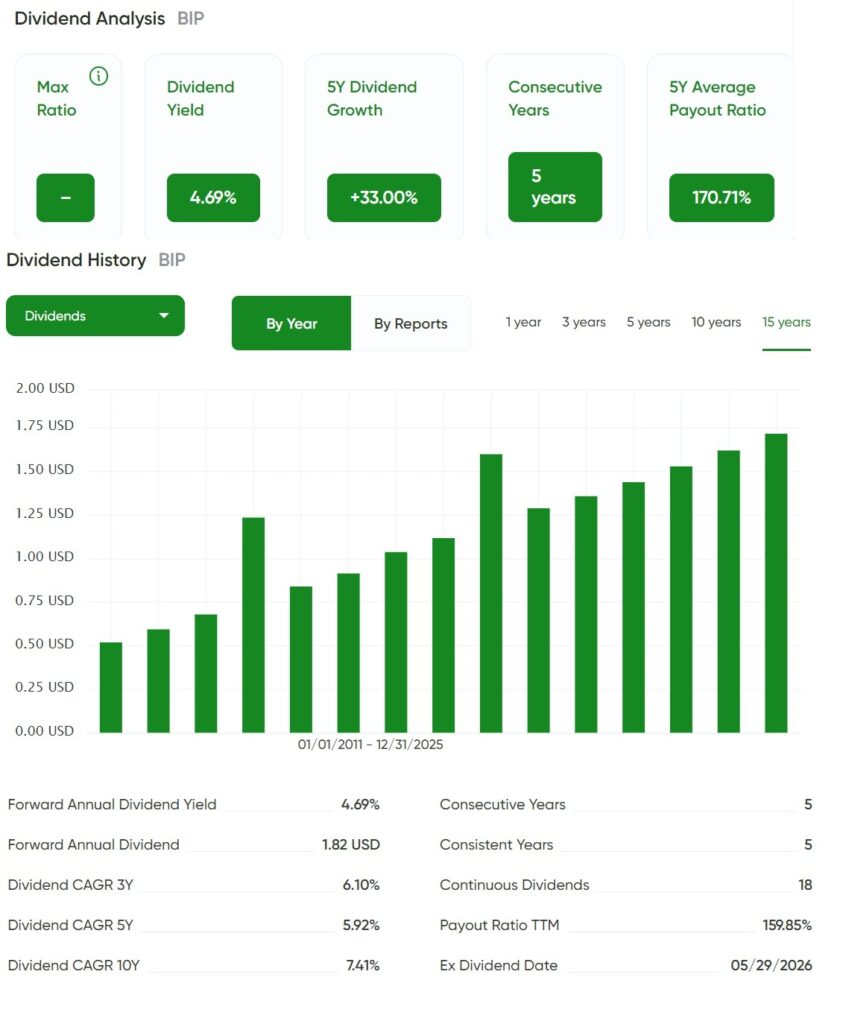

Brookfield Infrastructure Partners

- Sector: Utilities – Multi-utilities

- Dividend Yield: 4.69%

- Dividend Safety: Safe

- Uninterrupted Dividend Streak: 17 years

Brookfield Infrastructure Partners (BIP) has a portfolio of 40 infrastructure assets. The partnership delivers predictable results year after year.

The MLP cash flows are supported by revenues from regulated activities and long term contracts that include inflation indexing.

Fuel Distribution MLPs

Fuel distribution MLPs are engaged in the wholesale distribution and supply of motor fuel to gas stations. Take-or-pay contracts are also applicable in this sector. However, some MLPs have extremely low volume protection, which creates a risk of distribution cuts.

This category includes the following LPs:

- CrossAmerica Partners;

- Sunoco;

- Global Partners;

- Suburban Propane Partners.

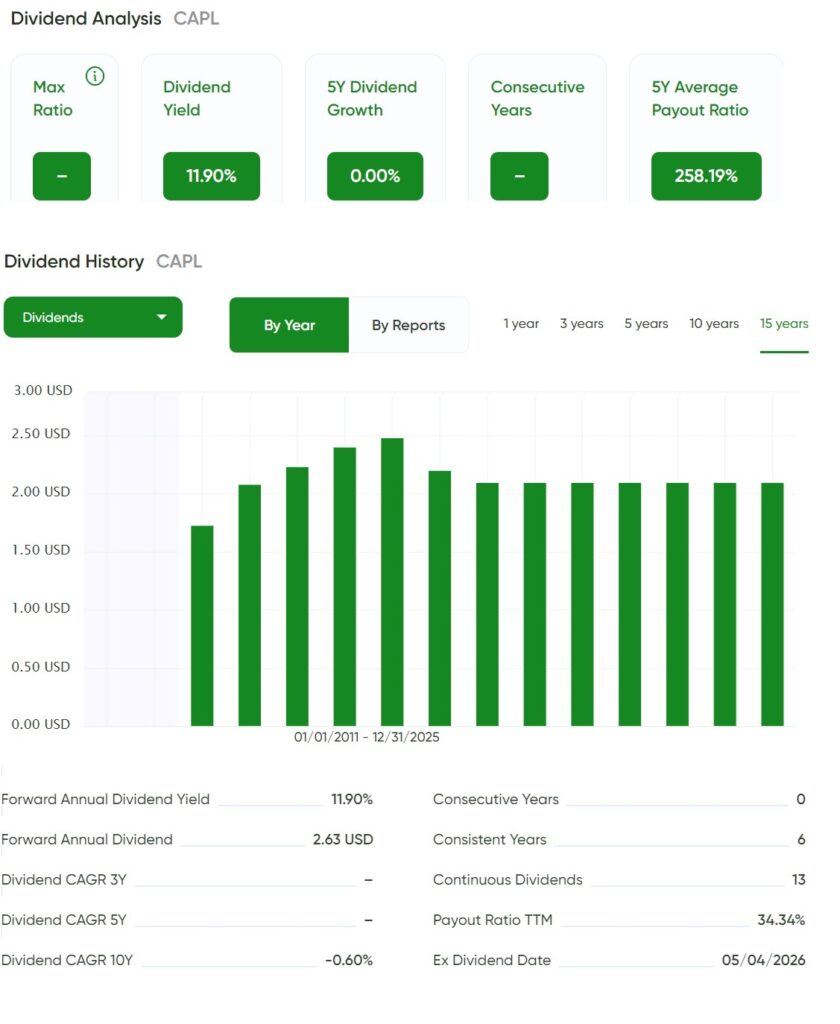

CrossAmerica Partners

- Energy – Fuel Distribution

- Dividend Yield: 11,90%

- Dividend Safety: Carefully

- Uninterrupted Dividend Streak: 6 years

CrossAmerica Partners (CAPL) supplies motor fuel to gas stations. Annual volume reaches 1 billion gallons. Part of the business has variable fuel margins, allowing CrossAmerica Partners to benefit in periods when oil prices fall faster than motor fuel prices.

An additional source of income that can provide stable cash flow is leasing space for convenience stores.

Non-Oil and Gas Commodity MLPs

These include LPs that are involved in the non-oil and gas commodities production. Examples include ethylene, coal, and fertilizer. This sector is characterized by higher price volatility than the oil and gas sector. As a result, the distribution reliability of these MLPs is lower.

Non-Oil and Gas Commodity MLPs:

- Westlake Chemical Partners;

- Alliance Resource Partners;

- CVR Partners.

Royalty MLPs

Royalty MLPs, such as Dorchester Minerals, own interests in mineral-rich land. Their income comes from fees for commodity extraction (oil, gas, coal). This provides high margins and a debt-free structure.

However, these partnerships have strong commodity prices sensitivity, resulting in high distribution volatility. Nevertheless, the amount of payouts typically increases again after the recovery of the energy market.

Examples of royalty MLPs include:

- Dorchester Minerals;

- Black Stone Minerals;

- Natural Resource Partners.

Investment Company MLPs

Investment company MLPs earn through transactions involving securities. Therefore, they are sensitive to the dynamics of financial markets. Investment MLPs offer high-yield distributions. Over the long investment horizon, the reward for volatility typically becomes total returns that exceed the performance of partnerships in the natural resources sector.

MLPs operating in financial markets include:

- Icahn Enterprises;

- AllianceBernstein;

- Greystone Housing Impact Investors LP.

Real Estate MLPs

An example of a real estate MLP is New England Realty Associates. This is a micro-cap partnership that owns apartment complexes. Long-term leases generate fairly stable cash flows. However, returns in this sector will lag behind those of natural resource MLPs. This makes these units less attractive to investors.

Understanding MLP Structure Variations

A publicly traded partnership (PTP) is a type of limited partnership (LP). Many of the master limited partnerships (MLPs) mentioned above are structured as PTPs. However, there are general differences between them. One of the first differences is that PTPs from energy-related businesses tend to pay higher quarterly income. This is due to the peculiarities of the tax regime.

An MLP may not be a PTP, i.e. it may not be publicly traded. Similarly, a PTP may not be an MLP. Such an entity may have the status of publicly traded limited liability companies (LLCs). These nuances affect partnership taxation.

Tax Implications When Selling MLPs

If investors sell MLPs held for less than a year, the gain is considered short-term capital gain. It is taxed as ordinary income. If the holding period exceeds one year, the long-term capital gains rate applies. Capital gains taxes are lower in this case, with rates ranging from 0% to 20%, compared to a range of 10% to 37% for ordinary income.

However, if a loss is incurred during a long holding period, it can only be used to offset capital gains. It will not reduce the tax basis for ordinary income.

Additionally, any return of capital received during the ownership of the units is taxed as ordinary income.

MLPs vs. REITs

A REIT must distribute at least 90% of its taxable profits to its shareholders. Only on this condition is it exempt from corporate income tax. There is no such requirement for MLPs, allowing them to retain more funds to maintain an investment-grade balance sheet and continued expansion of their business.

Many REITs offer dividend reinvestment plans for the compounding of gains. Their distributions are considered ordinary income, but a portion may be accounted for as capital gains. There is usually no return of capital. REIT shares are more suitable for deferred taxation accounts than MLP units.

Conclusion: Investing in MLPs

MLP stocks provide an opportunity to diversify a portfolio through business diversity. Master limited partnerships operate in industries such as natural resources, energy, commodities, and real estate.

Limited partnerships vary in terms of cash flow cyclicality, financial leverage, distribution coverage, and management structures. Therefore, it is essential to understand these factors before investing in such an asset.

Many MLPs offer high yields compared to common stock and come with moderate risk. However, their securities have lower liquidity. This is due to low investor awareness of the asset class, even though the first one was launched in 1986. Pipeline MLPs can offer the greatest stability in distributions..

This category of assets is particularly interesting to investors who value current income and seek double digit yields. A key advantage is the tax benefits in the form of tax deferral.

FAQ

What is an MLP investment?

MLPs investments involve purchasing a share of a commercial enterprise that exists in the form of a publicly traded partnership with limited liability. This provides the right to defer taxes on the distributions received.

Are MLPs worth investing in?

Investing in MLPs is worthwhile for those seeking high-yield stocks and wanting to gain tax advantages. This asset is not well-suited for building future retirement capital in deferred taxation accounts.

What is the downside of MLP?

The main downside is the volatility of the unit’s value. Additionally, these liquid securities are less liquid compared to blue-chip stocks, which attract a broader range of investors. As a result, they have higher trading volumes. Furthermore, the risk of distribution cuts is greater than the risk of dividend reductions.

Article Sources

- Roberts, J. & Thompson, K. (2023). “Master Limited Partnerships: Structure and Taxation in the Modern Economy.” Journal of Taxation and Regulation of Financial Institutions, 42(3), 114-132.

- Williams, M., Chen, L., & Rodriguez, A. (2024). “The Evolution of Energy MLPs in Modern Investment Portfolios.” Journal of Applied Finance, 36(2), 78-95.

- Harrison, P. & Miller, S. (2023). “Risk-Return Characteristics of MLP Investments: A Comparative Analysis.” Financial Analysts Journal, 79(4), 223-241.

- Anderson, T., Johnson, B., & White, C. (2024). “Tax Implications of MLP Investments: Current Regulatory Framework.” Journal of Accountancy, 238(1), 45-60.

- Zhang, H. & Peterson, D. (2024). “Correlation Between Energy Commodity Prices and MLP Performance.” Energy Economics, 118, 106358.

- Brown, R. & Garcia, E. (2023). “Institutional Investment in MLPs: Trends and Opportunities.” Journal of Portfolio Management, 49(3), 112-128.

- Mitchell, L., Davis, J., & Wilson, K. (2024). “MLPs in a Rising Interest Rate Environment: Historical Performance Analysis.” Journal of Investment Management, 22(2), 67-84.

- Smith, A. & Kumar, R. (2023). “Diversification Benefits of MLPs in Multi-Asset Portfolios.” Review of Financial Studies, 36(4), 1458-1476.

- Taylor, S., Martinez, J., & Lewis, N. (2024). “ESG Considerations in Energy Infrastructure Investments.” Journal of Sustainable Finance & Investment, 14(1), 33-52.

- Robinson, C. & Park, S. (2024). “The Future of Midstream Energy MLPs: Structural Changes and Investment Implications.” Harvard Business Review, 102(2), 88-96.

- Collins, M. & Washington, E. (2023). “MLP Valuation Methodologies: A Comparative Study.” Journal of Valuation Studies, 28(3), 205-224.

- Baker, D., Phillips, A., & Howard, J. (2024). “Regulatory Changes Affecting MLP Investments: Policy Implications.” Energy Policy, 175, 113420.

You Might Also Like

- What Is a Dividend Recap? Understanding This Financial Strategy

- What Is a Dividend Recapitalization? A Complete Guide for Investors

- What Is Dividend Recapitalization? Explained in Simple Terms

- How Does a Dividend Recap Work? Breaking Down the Process