No matter what the situation, it’s good to have a well-thought-out plan rather than acting on instinct. Financial matters are no exception. Based on statistical studies, people who work on a budget and investment strategies are better at both paying bills and tackling capital accumulation tasks.

Here are some basic financial planning tips to help you take the first steps towards wealth.

Table of Contents

Financial Planning Intro

A financial planning checklist is essential to address short-term goals while keeping an eye on long-term goals. It will also help you quickly track the growth rate of your assets over the years.

Unveiling the Concept of Financial Planning

Annual financial planning includes the analysis of all assets and liabilities. As a result, a document that clearly shows a person’s current situation and contains a strategy for achieving the set goals is in hand.

The main condition is to draw up as detailed a “map” of your financial path as possible. This is the basis for making key decisions.

Why a Little Planning Goes a Long Way

Through planning, a person can see the stage they are in. It provides a starting point for determining further financial strategy. One cannot neglect to assess their current state of affairs and still make effective progress towards the goal.

The main tasks for which financial planning is used are:

- Ensuring financial security and being prepared for emergencies;

- tracking progress towards long-term goals;

- reducing debt;

- increasing cash flow.

The “financial map” aspect that will be key depends on the person’s current situation. For some people, it will be debt reduction and the creation of an emergency fund. For another, it will be estate planning documents.

Your Personal Guide: The Financial Planning Checklist

Here are 7 key steps to creating a financial plan annually.

Plan your Life changes (retirement, marriage, new family members, change of residence, etc.)

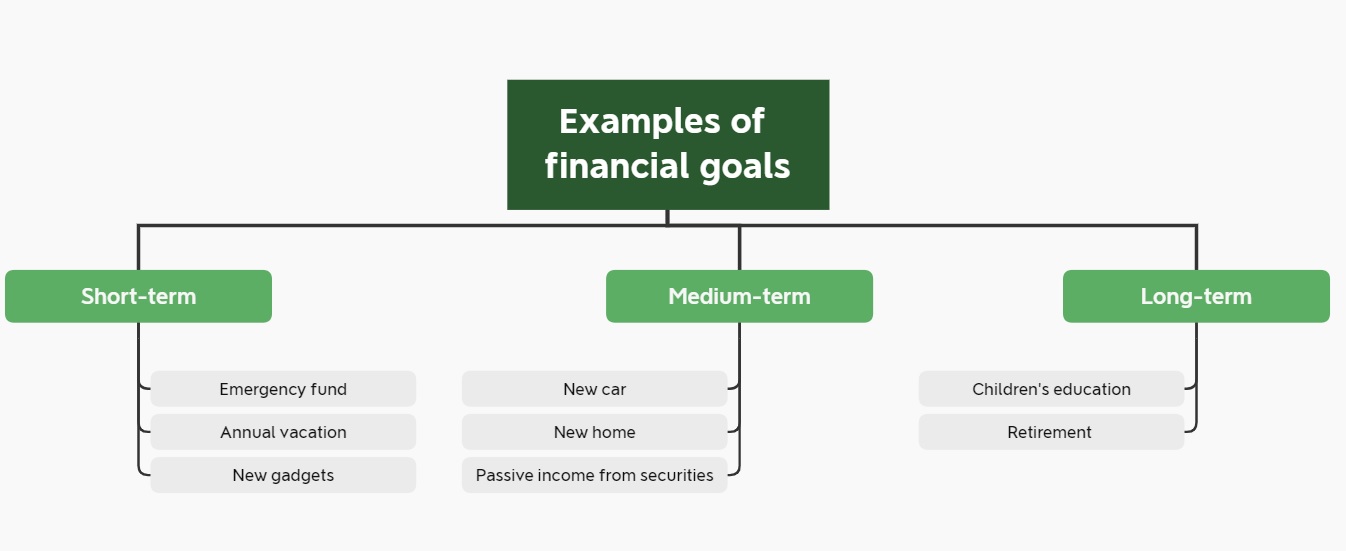

All major life events involve expenses. Therefore, the first step is to set goals and determine the timeframe when they should be realized. It is recommended to organize them by time horizon:

- short-term (less than 5 years);

- medium-term (5-10 years);

- long-term (more than 10 years).

For each point (getting married, buying a new house, etc.), the plan specifies the desired amount of money and the expected date by which it will be needed. The more detailed the list, the better the chances of achieving all the goals.

Regular financial plan updates

It is recommended that the frequency for reviewing your financial plans is once a year. But sometimes it is useful to conduct an extraordinary review. For example, you might need it in the following cases:

- A significant change in income, such as getting a new job;

- Significant events that affect a person’s spending, such as divorce or health problems;

- An unexpected large sum of money that significantly changes a person’s financial situation, such as an inheritance.

Get Emergency fund (3-6 months of expenses)

An emergency fund is the basis for financial success. At this planning stage, you need to make sure of 2 things:

- the amount available will allow you to live for a minimum of 3 months unemployed, optimally 12 months;

- the money is deposited on favourable terms and can be accessed at any time.

Another aspect is the definition of an emergency situation. The person must decide in advance what the money can be used for.

Informed Insurance policies and coverage

This includes life and health insurance, car insurance, property insurance, etc. The purpose of this planning stage is to make sure that the amount of insurance coverage of the chosen policy is sufficient to ensure financial security. It is also useful to compare other companies’ offers. This will ensure that the cost of services is not excessive.

Check your loans and credit

At this stage you need to analyze your debts – mortgages, credit card balances, etc. The most convenient way to do this is to examine your credit report. This is a summary of all of a person’s accounts compiled by a credit bureau.

This step is necessary to make sure that all payments are made on time. It is also possible that some of the loans involve a rate that is too high. It is wise to refinance or close them as soon as possible, even if only at the expense of investing.

An equally important indicator to track is the loan utilization ratio. It is calculated as the ratio of available debt to a person’s total credit limit.

Including Gifts for heirs or charities to you financial plan

Gifts and inheritances are generally considered taxable income in the United States. But there is a limit up to which no tax is withheld. In 2023, it’s $17,000 for each giver/gifted couple.

Charitable contributions are one way to reduce your tax base. It is advisable to use this opportunity particularly for wealthy people.

Calculate the approximate amounts of taxes and/or commissions for the next year

At this stage, it is necessary to take into account all the potential income that a person plans to receive next year and analyze which tax deductions they may be entitled to.

For example, reducing the fiscal burden could be beneficial with:

- Crediting traditional retirement accounts, flexible spending account, child tuition account, etc..;

- collecting tax losses;

- locking in long-term rather than short-term gains, etc.

It is sensible to discuss this issue with a tax professional in advance. Planning ahead will allow you to find and take advantage of all opportunities.

The commission costs clause applies to people with financial advisors, brokers or investments in funds. It is helpful to make sure that the most cost-effective options are chosen.

Crafting a Prudent Budget: The Bedrock of Financial Stability

In order to achieve global goals, a person must have a good understanding of their current situation. Budgeting is the foundation that is essential for financial health.

The Intricacies of Income and Expense Management

The following are the main ways to manage your budget and find the best balance between income and expenses.

Employing Budgeting Apps for Financial Tracking

The most common reason for savings difficulties is the lack of a clear understanding of 2 issues:

- how much a person earns;

- whether they’re really spending rationally.

Budget tracking apps can help solve this problem. Once synchronized with financial accounts, such programs automatically take into account all income and expenses, categorizing them. This allows a person to find areas in which their spending is higher than it should be. Reducing such purchases allows one to save money and increase savings.

The Philosophy of “Paying Yourself First”

This expression means that having received any income, a person should primarily replenish their savings or investment account. Only then can the remaining amount be allocated to mandatory monthly payments and minor expenses.

The idea is based on the fact that people with low financial discipline will find it easier to resist spontaneous purchases when they limit their budget in advance. Otherwise, there is a risk that at the end of the month they will again discover that there is no money left.

The Saving Habit: Small Steps to Big Financial Wins

Often people give up on the idea of capital formation because of low income or high expenses. Many people believe that the modest amounts they can allocate to savings will not make a difference.

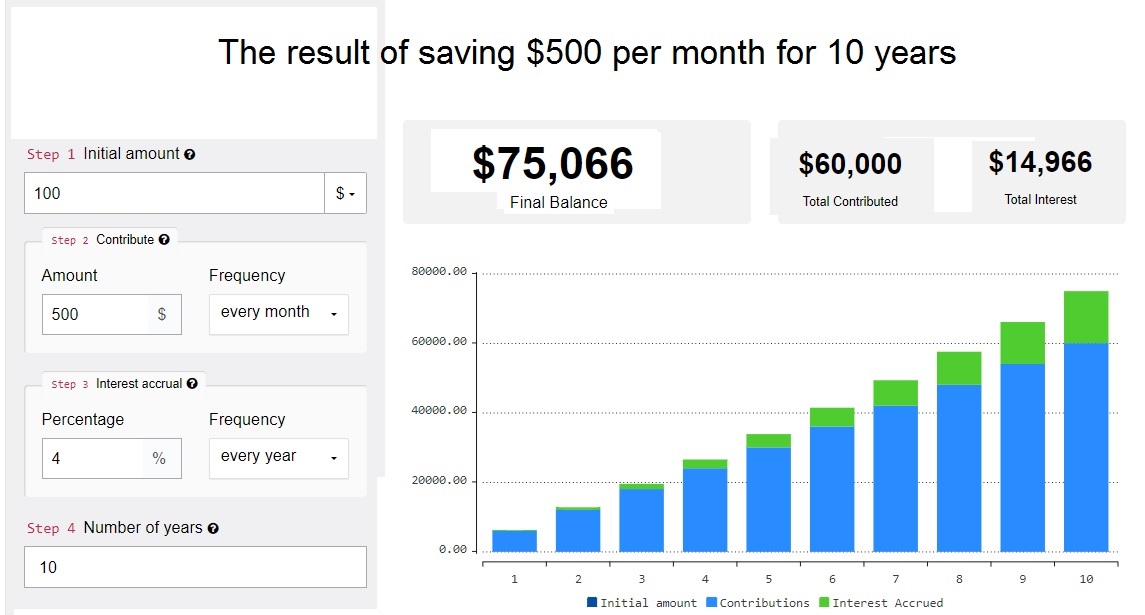

In fact, any progress starts with small steps. By setting aside even 10 percent of a small income, over the years a person can improve their financial situation.

Set It and Forget It: The Beauty of Automated Savings

The financial industry offers several types of savings automation tools:

- regular automatic crediting of a fixed amount from a current account to a savings or investment account;

- depositing a fixed amount of interest on each cash inflow;

- rounding up expenses to a set value and crediting the difference to a separate account;

- automatic reinvestment of dividends from mutual funds and other securities.

Thanks to such opportunities, accumulation no longer requires constant moral effort.

Dream Big and Save Bigger: Aligning Savings with Goals

Starting an emergency fund by setting aside a small amount of income is only the first step in a personal finances management strategy. When a person has already developed a savings discipline, it makes sense for them to build up their savings.

Therefore, the next step is to calculate how long it will take to accumulate the required amounts and find ways to shorten this period of time. It is also useful to split the money into different “piggy banks” rather than keeping it all in one account. This way, a person will clearly see if they are close to their goals.

Building Your Financial Safety Net: The Emergency Fund

Wealth accumulation starts with building emergency savings. Skipping this stage and directing all the money to investing is a mistake.

Why an Emergency Fund is Your Financial Best Friend

Unexpected negative events happen in everyone’s life. An emergency fund is a buffer that protects you from having to urgently sell your assets, losing value for a quick deal.

For someone who has no significant capital yet, an emergency fund is a defense against the need to take out high-interest consumer loans and use credit cards.

Crunching the Numbers: How Much is Enough?

This is the amount needed to cover emergency expenses or to maintain your current standard of living if you lose your source of income. The size of the emergency fund is directly dependent on the level of spending a person is accustomed to. To determine its optimal amount, it is necessary to:

- Keep track of your family’s expenses for several months (or better yet, a year);

- find the arithmetic average of the expenses per month;

- multiply the resulting number by the desired term.

The minimum term a mutual fund should be designed for is 3 months. The optimal period is 6-9 months. It is not advisable to keep in cash the amounts needed for more than a year of living with no income.

Keeping Your Fund Accessible When Life Happens

It is recommended that such a fund be held only in liquid assets, even when one has a high risk tolerance. The best options are high-yield savings accounts or money market accounts at a bank or credit union.

These allow a person to use their money at any time with no penalty or threat of losing part of the original amount. Other financial instruments offer no such opportunity. Even short-term Treasury bills have a risk of declining in value on the secondary market.

Stories from the Financial Trenches: The Emergency Fund in Action

The example below demonstrates how useful it is to have an emergency fund. Let’s say a person has a health problem that:

- prevent him from working for three months;

- require $7,000 worth of treatment that would not be covered by health insurance.

However, the individual created a six-month emergency fund of $30,000 in advance at the rate of $5,000 per month. This money was placed in a savings account. This will allow them to pay for treatment and live for 3 months with no income. The total cost would be $21k.

In the absence of an emergency fund, the person would be forced to live in debt. In August 2023, the average credit card rate was 22.77%. Suppose the borrower could pay off the debt in full in six months. In this case, the borrower would have paid about $2000 more to the bank.

A person who keeps all the capital in investments would also face unnecessary losses. Let’s say all their money is invested in a safe asset like US Treasuries through the iShares 20+ Year Treasury Bond ETF. Due to rising interest rates, this fund has lost 17.5% of its value in the last six months alone. Selling its stocks now is extremely unprofitable.

Thus, a maximally liquid emergency fund is the most effective solution to unexpected financial problems.

Sleeping Soundly with a Safety Net Below

The previous section showed that having an emergency fund is financially beneficial. This capital protects against the need to resort to loans and end up overpaying.

No less important is its psychological function. A person who has a deposit that covers basic needs for a few months feels much calmer than someone who lives with no savings.

Balancing Act: Juggling Debts and Keeping Finances Healthy

The average person cannot do without credit. Most have student debt for tuition, a mortgage, a car loan. Many have consumer loans and credit cards.

The main goal of financial planning is to make judicious use of all the tools available to the individual, rather than avoiding debt altogether.

Unraveling the Debt Web: Short-Term vs. Long-Term

All financial liabilities held by the average family can be divided into short-term and long-term liabilities. The former are usually high interest debt. The latter, such as mortgages, are usually much cheaper to service.

Finding ways to close costly loans as quickly as possible is an important part of financial planning. This is the next step in capital formation once an emergency fund has been established.

You should determine whether you should use your free money for early repayment of the loan or for investment by the ratio of interest rate and yield. The following priority distribution can be given as an example:

- closing a credit card debt with a 20% interest rate is more favourable than buying bonds with a yield of 5%;

- investing in an asset with a yield of 5% is more favourable than making a partial early repayment of a mortgage with a rate of 3%.

Tackling High-Interest Debts Head-On: A Game Plan

There are 2 ways to solve the problem of expensive loan:

- minimize expenses as much as possible and repay debts quickly;

- refinance debt (for example, even a consumer loan is often more favourable than a credit card).

Against the backdrop of rising interest rates, it can be difficult to find a favourable refinancing offer for a fixed-rate loan taken out several years ago. But it is of particular importance to close debts with floating rates (e.g., credit cards) during this period. The reason for this is that as the Fed Funds rate increases, the cost of such a loan will rise.

Wrapping Up: End of Year Financial Checklist

The final document that a person produces during a review of their financial life should answer the following questions:

- what income is expected for the next year;

- what expenses are planned for the next year;

- what employer-provided benefits can be used in the next year;

- what amount should be allocated to mandatory payments;

- what costly debts require closing as quickly as possible when this goal is reached;

- whether the size of the emergency fund is adequate;

- what amount should be set aside for long-term purposes;

- whether any adjustments to retirement planning need to be made;

- what the investment strategy is for the coming year;

- whether estate plans need to be reconsidered;

- how much will be set aside for gifts to children, spouse, charitable donations, etc.;

- what the expected tax bill is and how it can be reduced;

- whether available insurance policies meet your current needs;

- whether there is an opportunity to reduce your commission costs.

You need to go through all the items on the financial plan checklist, even when some of them seem irrelevant at first glance.

Final Tips

In conclusion, here are a few tips to make it easier to have a sound financial plan.

1. Seeking Professional Help

In some situations in life, seeking professional help from a financial professional will be helpful:

- The person has large debts with high rates and finds it difficult to choose refinancing options.

- The person has no savings skills and sees no opportunity to reduce their expenses.

- A person has a large number of assets (stocks and bonds, real estate equity, precious metals, etc.) and wants to optimize their capital structure and make it more transparent.

The assistance of a tax advisor will also be helpful. An expert can suggest numerous options for reducing tax liability.

2. Use Financial Tools: Your Digital Aides in Wealth Building

For those who prefer to avoid consulting an expert, online budget planning and investment management services will be useful. Examples:

- Kubera;

- Mint;

- Quicken.

There are also applications that allow you to work on tax optimization. The best of them can fully replace the tax advice of a live expert.

3. Staying Informed on Your Financial Path

One day deciding to save more is not enough to achieve financial independence. You need to constantly acquire new knowledge that will help you shorten the path to your goal. BeatMarket can help you do this. The platform has collected a large number of educational materials. They will be useful for those who make the first steps in the capital formation and want to form a high-quality investment portfolio.

FAQ

What should I do financially before the end of the year?

The main thing is to make sure that all the financial goals set for this year are met and to draw up a new list of tasks. For those who have never done any planning before, it is useful to first of all pay attention to whether they have utilized all the benefits available to them – tax deductions, etc.

How do I plan my finances for the year?

You need to roughly calculate your expected income and make a list of key expenses, taking into account both everyday spending and saving for long-term goals.