Key Takeaways:

- Verizon Communications, a wireless carrier, is considered a blue-chip stock. However, when investors ask ‘is Verizon a dividend aristocrat?’, the answer is no – its dividend history means that VZ cannot be included in the Dividend Aristocrat Index.

- Many telecommunications companies have high dividend yields, and Verizon is one of the industry leaders in this respect. At the same time, however, it has a moderate payout ratio.

- Verizon’s earnings reports for the first and second quarters earnings demonstrate an increase in free cash flow. However, the lack of significant revenue growth has raised investor concerns about the dividend safety.

In this article, we will answer the question, ‘Is VZ a good dividend stock?’ and explore whether there are any big warning signs that suggest an imminent reduction in payouts to shareholders.

Table of Contents

Verizon’s Business Overview and Market Position

Verizon Communications is a telecommunications giant whose business includes:

- wireless services;

- broadband;

- fiber-optic networks.

Verizon has lost a small portion of its market share amid a competitive landscape. For instance, the company has reported a slight decline in revenue in its corporate services sector. Its subscriber base in the wireline business segment is also shrinking. The main competitors are AT&T and T-Mobile.

Verizon business requires significant infrastructure investments, primarily for developing the 5G network. This is one of the key reasons raising questions: is Verizon dividend sustainable in its industry positioning and whether it remains a safe dividend investment.

Verizon’s Dividend History: Is Verizon a Dividend Aristocrat?

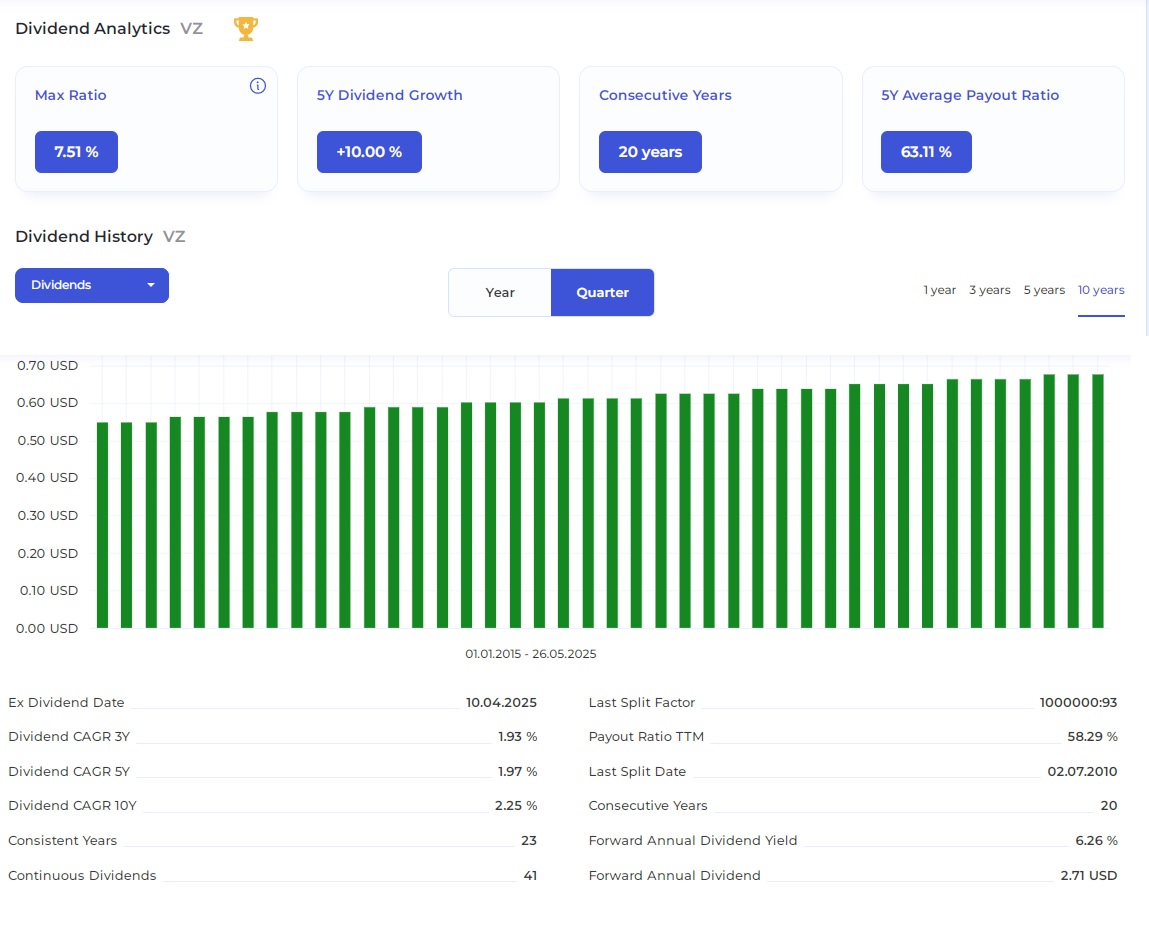

Verizon demonstrates a steady dividend growth streak. Over the past 10 years, its quarterly payments have increased by $0.12. The company has a consecutive annual increases record of 20 years.

This has enabled Verizon to join the ranks of high-yield dividend stocks. The company also offers an attractive dividend reinvestment plan (DRIP).

A yield comparison shows that Verizon’s payouts surpass those of both the industry average and the S&P 500 average. While the typical dividend yield for telecom stocks is less than 4.5%, Verizon’s dividend investment provides a yield of 6.2%.

The dividend policy includes management commitments to increasing shareholder earnings, and the company has the potential to achieve dividend aristocrat status within five years.

The forward dividend yield for May 2025 is higher than the 10-year average, suggesting that the stock of Verizon can currently be purchased at an attractive discount.

Key Financial Metrics: Is Verizon a Dividend Aristocrat Candidate?

In the first quarter, Verizon’s cash reserves declined by 5.81% YOY. Revenue growth for the same period was 1.53%. Debt levels remain stable, totaling $172.5 billion as of March 31, 2025. Other financial results for Q1 2025 are as follows:

- free cash flow (FCF) – $3.637 billion;

- operating income – $8.262 billion;

- operating cash flow – $7.782 billion;

- profit margins – 14.57%;

- leverage ratios – 1.69 (Debt / Equity Ratio) and 8.31 (Debt / FCF Ratio);

- interest coverage – 5;

- payout ratio – 58.29%.

Despite high capital expenditures the company incurred, analyst projections suggest that Verizon’s financial stability will be maintained.

Free Cash Flow Analysis

As of March 31, 2025, Verizon’s free cash flow had increased by 34.31% year-over-year comparison. This figure represents the difference between operating cash flow and capital expenditures.The company uses these funds for dividend payments. Therefore, according to quarterly results, the current FCF trend is a positive sign, indicating the sustainability of dividends.

Verizon has demonstrated strong free cash flow generation capabilities. Its free cash flow margin has gradually increased to reach 15.34% over the past 12 months.

According to annual projections for 2025, the company’s free cash flow is expected to be between $17.5 billion and $18.5 billion. This corresponds to a dividend coverage ratio of 1.6, supporting Verizon’s status as a safe dividend stock.

Dividend Payout Ratio Assessment

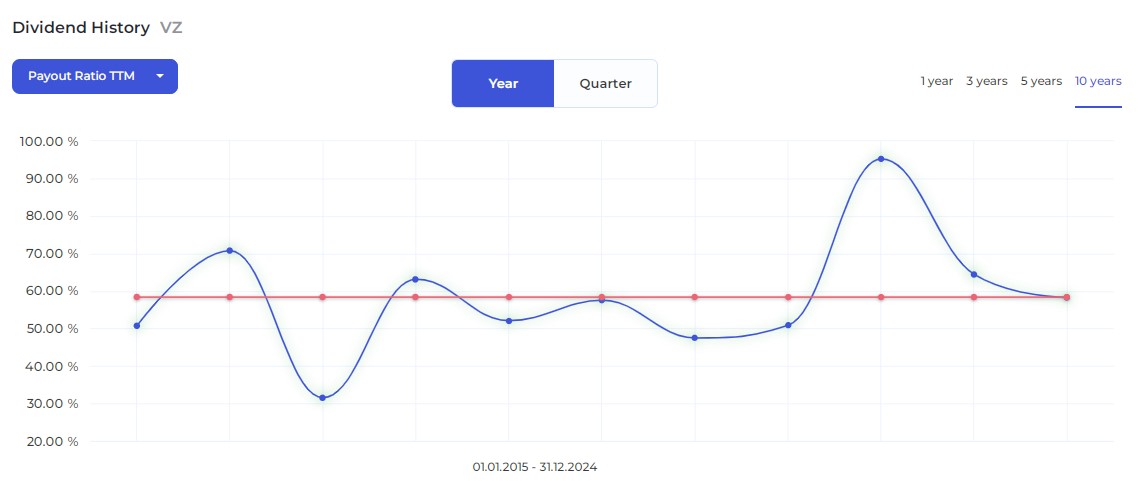

The historical comparison shows that the earnings-based payout ratio of 58.29% is within the average range over the past 10 years. This indicator aligns with industry benchmarks. The FCF-based payout ratio also remains within a sustainable range.

Management’s target is to achieve earnings growth of up to 3% by the end of 2025. The dividend CAGR over 5 years is 1.97%. The company has a safety margin for further dividend increases.

Debt and Financial Leverage

Verizon’s total debt and its debt-to-EBITDA ratio have remained at approximately the same level for several years. As of March 31, 2025, the debt service coverage ratio, as measured by free cash flow (FCF), stood at 3.12.

In 2023-2024, there was an increase in interest expenses, primarily due to rising interest rates. Nevertheless, it was business as usual with Verizon steadily growing its top line each quarter in 2024.

The company’s financial flexibility and balance sheet strength are reflected in its credit rating of A- from Fitch.

A common question among dividend investors – is Verizon’s dividends safe considering refinancing risk. According to its debt maturity schedule, Verizon is expected to pay $24.562 billion over the next 12 months out of total debt of $172.533 billion.

Recent Financial Performance and Guidance

Verizon recently reported the following results:

- quarterly earnings – $4.879 billion;

- annual results for net income – $17.783 billion;

- revenue trend – 0.93%;

- quarterly wireless service revenue growth – $23.25 billion;

- consumer wireless postpaid average revenue per user (ARPU) – $146.46;

- profit margins – 14.57%.

According to management forecasts, by the end of 2025, internet subscriber growth is expected to reach up to 8 million.

Based on analyst expectations, EPS for the year is projected to be between $4.52 and $5.01. Assuming no negative surprises in profits occur, this allows a positive assessment of ‘Is Verizon dividend safe?’

Capital Allocation Priorities

Any company’s capital allocation strategy includes:

- dividend payments;

- share repurchases;

- debt reduction;

- acquisition strategy and capital expenditures (primarily the 5G network investments).

In the case of Verizon, management priorities are focused on increasing shareholder returns through dividend growth.

Competitive and Regulatory Challenges

Market saturation and competitive pressures from T-Mobile and AT&T influence the pricing dynamics and Verizon’s earnings. Negative factors that dividend investors should consider during stock picks include:

- subscriber churn risk;

- ongoing wireless industry changes and changing regulatory environment;

- FCC policies regarding antitrust concerns;

- expenses related to spectrum auction participation.

5G Infrastructure Investments and Future Growth

The 5G network deployment requires significant capital expenditures and infrastructure investments. Additionally, expenses related to subscriber adoption of fixed wireless access are necessary.

However, new business segments offer additional revenue opportunities. Providing current enterprise solutions and capturing market share in the Internet of Things (IoT) will ensure the return on invested capital. Nevertheless, so far, the company’s reports do not demonstrate growth in wireless service revenue.

Management’s Commitment to the Dividend

Management statements during investor presentations and quarterly earnings calls confirm the dividend priority.

Executive compensation is aligned with shareholder alignment. The management of Verizon forecasts a continued dividend increase history.

Therefore, the stock of Verizon is recommended for a dividend strategy. However, it is unlikely that they will produce monster returns through share price growth.

Potential Risks to Dividend Safety

Potential threats to Verizon’s high yielding dividend include:

- industry disruption;

- technological change;

- competitive threats;

- market saturation;

- regulatory challenges;

- capital expenditure requirements;

- subscriber losses;

- margin pressure.

Although the company has a moderate debt burden, it is important to consider the risk of interest rate sensitivity.

Analyst Perspectives on Dividend Safety

Dividend coverage estimates and other factors provide Verizon with high sustainability ratings. Expert opinions and investor sentiment are generally positive. According to Investing.com, the distribution of buy/hold/sell recommendations from Wall Street analysts is 13/13/0. The consensus view on price targets is an increase to $48.07 within the next 12 months.

The Bottom Line: Is Verizon’s Dividend Safe?

The positive answer to ‘Is VZ dividend safe?’ is supported by the fact that this company is often included in investment recommendations for income investors and retirees. While investors may ask ‘is Verizon a dividend aristocrat?’, the company is on track to achieve this status within five years given its 20-year dividend growth streak.

The company’s long-term outlook strengths include:

- dividend sustainability;

- yield attractiveness;

- total return potential;

- dividend growth prospects.

Its incredibly high yield compared to the average S&P 500 figure makes Verizon’s stock a bargain buy. In the context of declining interest rates, Verizon can help maintain portfolio fit by preserving the required return. Today, VZ’s stock is undervalued. However, according to analyst expectations, it will soon become a popular investment again.

FAQ on Verizon’s Dividend

How often does Verizon pay dividends and what are the important dates?

Verizon’s dividend frequency is quarterly payments. The next ex-dividend date is October 7, 2025.

How does Verizon’s dividend yield compare to other telecommunications companies?

The yield comparison shows that Verizon is a top telecom stock in terms of dividends. The company typically pays an annual dividend of over 6% of its stock price. Due to dividend taxes, it is most advantageous to invest in these stocks within retirement accounts, which provides favorable reinvestment options.

Has Verizon ever cut or suspended its dividend?

According to Verizon’s dividend history, the last dividend cut was in 1998. According to BeatMarket estimates, the suspension risks are minimal compared to competitors. For example, the AT&T stocks mentioned have a lower safety rating.

What is Verizon’s dividend growth rate and is it likely to continue?

The dividend growth rate (CAGR) 3Y is 1.93%. Experts expect the company to maintain this dynamic, but they do not promise to produce monster returns.