Key Takeaways:

- Dividend taxation is a factor that influences an investor’s overall return. Understanding how are dividends taxed is essential for effective investment planning and tax optimization.

- Tax rates depend on a number of factors. The most important factor is the status of the investment income received.

- Qualified dividends are one way to reduce the tax burden. The maximum federal tax rate on such dividends is 20%.

- Tax is applied to ordinary dividends at rates up to 37%.

This article will provide comprehensive information about US tax on dividends, explaining the situations in which an investor might answer ‘no’ to the question: ‘Do I have to pay tax on dividends?’

Table of Contents

What Are Dividends and How Do They Work?

The dividend definition shows that they represent shareholder payments. These payments are sourced from corporate profits. Such payments reward investors for their investments.

Most shareholders of American companies receive dividend income quarterly. However, other frequencies are also possible, such as monthly, twice yearly, or yearly. The amount of dividends paid out is determined based on the company’s dividend policy and financial results.

The dividend yield is the ratio of the annual dividend to the stock price, expressed as a percentage.

Types of Dividends: Qualified vs. Ordinary

The dividend classification for tax purposes was intended to encourage companies to make regular payments and to motivate investors to hold shares in the long term.

Qualified dividends are subject to preferential tax treatment. They are taxed at the same rates as long-term capital gains.

Nonqualified dividends, also known as ordinary dividends, are taxed at the regular income tax rates.

Note: To be eligible for upcoming dividend payments, regardless of their classification, shares must be purchased before the ex-dividend date.

What Makes a Dividend “Qualified”?

Dividend qualification criteria are determined by the IRS requirements (Internal Revenue Service). They include four key conditions:

- Source of payments requirements.

- Type of payments requirements.

- Holding period rule.

- Hedge prohibition.

There are two types of payment source. The first type is an American corporation that pays taxes on its profits. Dividends from tax-exempt corporations or farm cooperatives are not considered ‘qualified dividends’. The second possible source is a qualified foreign corporation.

Only regular dividends can be recognised as qualified dividends. Capital gains distributions, liquidation dividends and other types of dividend are not included here.

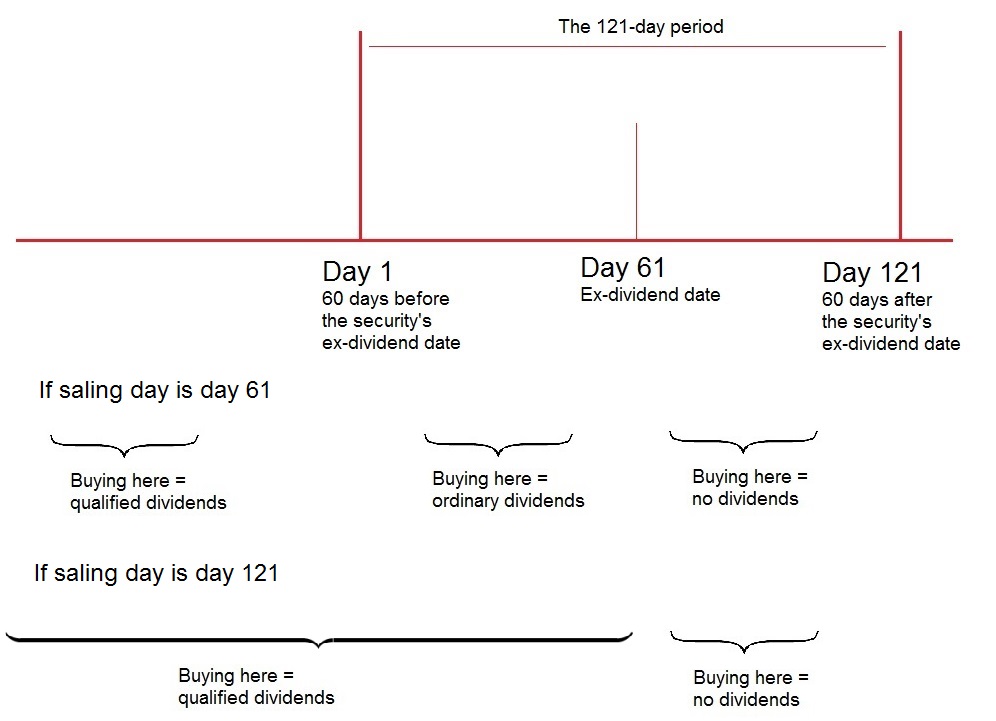

Under the 61-day rule, an investor must hold common stock for at least 61 days during a specific 121-day period. This period begins 61 days before the ex-date. Only then will the investor be eligible for special tax treatment. For preferred stock, these periods are 91 and 181 days, respectively.

The hedge prohibition means that investors can only hold long positions in dividend-paying company stocks. Using options and other derivatives based on these underlying stocks also disqualifies the investor from certain tax brackets. This must be taken into account when developing an investment strategy.

Special Cases: REITs, MLPs, and Foreign Dividends

Let’s discuss ‘how are dividends taxed for pass-through entities’? REIT dividends (Real Estate Investment Trusts) cannot be recognised as qualified dividends. They are typically taxed at ordinary income tax rates. Similarly, MLP distributions are not considered qualified dividends; most of them represent a return of capital.

Dividends from mutual funds can be recognised as qualified dividends, but only if the fund itself received qualified dividends, meaning that it met the holding and hedging requirements.

Tax is applied to dividends of a foreign corporation at reduced rates if the corporation is considered a qualified foreign corporation. There are three conditions for this:

- shares or ADRs are traded on U.S. exchanges;

- corporation is registered in the U.S.;

- corporation is in a country with a tax treaty with the U.S. that covers income taxes.

Dividends paid on credit union deposits cannot be recognised as qualified dividends; they are considered interest income. Furthermore, reduced rates do not apply to dividends received within an ESOP.

How Are Dividends Taxed: Current Dividend Tax Rates (2024-2025)

Qualified and nonqualified dividends are taxed differently based. The taxation on dividends is determined by income thresholds. Below are the income thresholds for each federal tax bracket depending on the filing status.

Capital gains rates.

2024

| Qualified dividend tax rate | Single | Married filing jointly | Married filing separately | Head of household |

| 0% | up to $47,025 | up to $94,050 | up to $47,025 | up to $63,000 |

| 15% | $47,026 – $518,900 | $94,051 – $583,750 | $47,026 – $291,850 | $63,001 – $551,350 |

| 20% | $518,901 and more | $583,751 and more | $291,851 and more | $551,351 and more |

2025

| Qualified dividend tax rate 2025 | Single | Married couples filing jointly | Married couples filing separately | Heads of household |

| 0% | up to $48,350 | up to $96,700 | up to $48,350 | up to $64,750 |

| 15% | $48,351 – $533,400 | $96,701 – $600,050 | $48,350 – $300,000 | $64,751 – $566,700 |

| 20% | $533,401 and more | $600,051 and more | $300,001 and more | $566,701 and more |

Ordinary income tax rates.

2024

| Tax rate | Single | Married filing jointly | Married filing separately | Head of household |

| 10% | up to $11,600 | up to $23,200 | up to $11,600 | up to $16,550 |

| 12% | $11,600 – $47,150 | $23,200 – $94,300 | $11,600 – $47,150 | $16,550 – $63,100 |

| 22% | $47,150 – $100,525 | $94,300 – $201,050 | $47,150 – $100,525 | $63,100 – $100,500 |

| 24% | $100,525 – $191,950 | $201,050 – $383,900 | $100,525 – $191,950 | $100,500 – $191,950 |

| 32% | $191,950 – $243,725 | $383,900 – $487,450 | $191,950 – $243,725 | $191,950 – $243,700 |

| 35% | $243,725 – $609,350 | $487,450 – $731,200 | $243,725 – $365,600 | $243,700 – $609,350 |

| 37% | $609,350 and more | $731,200 and more | $365,600 and more | $609,350 and more |

2025

| Tax rate | Single | Married filing jointly | Married filing separately | Head of household |

| 10% | up to $11,925 | up to $23,850 | up to $11,925 | up to $17,000 |

| 12% | $11,925 – $48,475 | $23,850 – $96,950 | $11,925 – $48,475 | $17,000 – $64,850 |

| 22% | $48,475 – $103,350 | $96,950 – $206,700 | $48,475 – $103,350 | $64,850 – $103,350 |

| 24% | $103,350 – $197,300 | $206,700 – $394,600 | $103,350 – $197,300 | $103,350 – $197,300 |

| 32% | $197,300 – $250,525 | $394,600 – $501,050 | $197,300 – $250,525 | $197,300 – $250,500 |

| 35% | $250,525 – $626,350 | $501,050 – $751,600 | $250,525 – $375,800 | $250,500 – $626,350 |

| 37% | $626,350 and more | $751,600 and more | $375,800 and more | $626,350 and more |

Net Investment Income Tax Considerations

The Net Investment Income Tax (NIIT) is an additional 3.8% surtax that high-income investors are required to pay.

The tax base is the lesser of two amounts, which are:

- net investment income (NII);

- the excess of modified adjusted gross income (MAGI).

Individual taxpayers must pay the NIIT if they have more than $200,000 in taxable income per year. For married couples filing jointly, the threshold is $250,000; for those filing separately, it is $125,000.

How Dividend Taxes Are Reported and Paid

At the end of the tax year, brokers and management companies send tax forms to investors. They are required to provide individuals who received more than $10 in dividend income during the year with Form 1099-DIV.

The task of an investor is to consolidate the tax reporting provided by different sources. A summary of dividend income must be included in the tax return (Form 1040). According to IRS requirements, investors who have received more than $1,500 in taxable dividends during the year must also complete Schedule B.

Understanding Your 1099-DIV Form

The key 1099-DIV boxes for dividend reporting are as follows:

- Ordinary dividends box. This figure represents the total amount of dividends received during the year.

- Qualified dividends box. It contains the amount of dividends that are taxed at capital gains rates.

- Non-dividend distribution. This includes the amount paid out from sources other than corporate earnings.

- Foreign tax paid. It contains information about withholding tax on dividends paid by foreign corporations.

How Are Dividends Taxed: Strategies and Planning

Tax-efficient investing uses tax-advantaged accounts. Primarily, these include retirement accounts. There are also health savings accounts, education savings accounts for children, and others. They also provide eligibility for tax benefits.

Another option for dividend tax planning involves holding period strategies. These strategies involve holding assets for a certain period to qualify for lower tax rates on qualified dividends.

Tax-Advantaged Accounts and Dividend Income

The advantage of tax-deferred accounts is tax-free growth of capital. Tax liabilities only arise when funds are withdrawn from the account. Consequently, by reinvesting these amounts, an individual can achieve higher overall returns.

For example, this is how IRA dividends work. There is a similar 401(k) dividend treatment. Contributions to these accounts reduce the current taxable income of the investor.

The Roth IRA tax advantages and ones of the Roth 401(k) lie in the fact that investment income is fully tax-free. Retirees do not have to pay tax on money withdrawn from these accounts.

However, these benefits only apply to stocks with dividends that are subject to taxation. Investments in MLPs, on the other hand, can lead to additional tax implications. Therefore, before purchasing such assets within a retirement account, it is advisable to seek tax advice or consult a personal finance professional or financial advisor regarding your investment objectives.

Dividend Reinvestment and Tax Implications

Dividend reinvestment plans (DRIPs) are designed to automate the purchase of new shares. The goal is to benefit from compounding and increase the investor’s capital. There may also be a cost basis advantage, as some companies offer shares at a discount below the market price within DRIPs. Furthermore, transaction fees are usually lower than those charged by brokers.

A common question is ‘Are dividends taxed if they are reinvested?’ The answer is yes. Reinvested dividends are subject to the same tax treatment. The applicable tax rate depends on the investor’s tax bracket and whether the dividends are ‘qualified’ or ‘ordinary’. If an investor receives shares at a reduced price within a DRIP, the difference is also considered taxable income.

If a company pays dividends in the form of additional shares, investors do not have to pay tax on them until they sell those shares.

Special Dividend Tax Situations

There are several dividend tax exceptions. The most common of these is return of capital. This amount can be found in Box 3 of Form 1099-DIV. Such payments are most often made by MLPs. Provided the original investment cost has not fallen to zero, distributions of this type are not taxed.

Extraordinary dividends are additional payments made by a company on top of regular dividends in special cases. As these are taxable distributions, they cannot be considered qualified dividends. The funds received are included in the amount shown in Box 1a.

Another exception is liquidating distributions. As they are often not made in cash, information about them appears in Box 9. However, if the distribution is in cash and exceeds the original investment, it is treated as a capital gain.

International Dividend Tax Considerations

Receiving international dividends also incurs tax liabilities. The amount depends on the legislation of the country in which the shares are issued. Foreign tax withholding at source is automatic. Often, these rates exceed those applicable in the United States. For example, the dividend taxation from Italian stocks is 27%, and from Swiss stocks it is 30%.

The issue of double taxation is also important. It depends on whether the country where the company is registered has tax treaties with the U.S. If such treaties exist, an investor can use a foreign tax credit. In order to do so, Form 1116 must be completed.

Conclusion: Maximizing After-Tax Dividend Returns

Investors must address the issue of dividend tax efficiency as a component of investment planning. Tax-smart investing can significantly boost overall after-tax returns. This is particularly pertinent for individuals with a high income. When selecting assets for long-term investing, understanding how are dividends taxed becomes crucial for accurate return calculations.

It is important to consider ‘what is the tax on dividends’. It is important to calculate after-tax returns. Some stocks, such as REITs, offer attractive ‘gross’ yields. However, the final result may be lower than for stocks whose dividends are considered ‘qualified dividends’.

Additional Resources

Additional information can be found in reliable tax resources and dividend tax guides, such as IRS publications. Publication 550, ‘Investment Income and Expenses’, is a good example.

Online tax calculators can help with calculations. They enable you to take into account factors such as filing status, income, age, and other factors.

If you have any questions about qualified dividends or dividends from foreign companies, we recommend consulting financial advisors or tax professionals. These experts can also help you choose a tax optimisation strategy that aligns with your investment goals.

FAQ

How much do you pay in taxes for dividends?

Taxes on dividends depend on the investor’s income and the type of investment account they use. They are also influenced by the type of dividends, the corporate structure of the payer, and the country of origin of the shares.

How much dividend is taxable?

Tax is applied to ordinary dividends at rates for ordinary income. These rates start at 10% and can reach up to 37%, depending on the federal income tax category in which the investor falls. Tax is applied to qualified dividends at 0%, 15%, or 20%.

How much tax do I pay on dividends received?

Taxation on dividends range from 0% to 37%. A financial advisor can help determine your individual tax rate and find ways to reduce your tax break.

Is there 30% tax on US dividends?

A 30% tax rate is applicable for foreign citizens who are not residents of the United States.

Article Sources

- Shaviro, D. N. (2022). Understanding Corporate Taxation and Dividend Policy: International Perspectives. Oxford University Press.

- Miller, M. H., & Modigliani, F. (2023). Dividend Policy, Growth, and the Valuation of Shares: Contemporary Analysis. Journal of Financial Economics, 45(3), 411-433.

- Chen, J., & Zhang, L. (2024). Dividend Taxation Systems Across Global Markets: Comparative Analysis. International Tax Review, 37(2), 78-95.

- Williams, R. C. (2024). Tax Law Fundamentals: Personal and Corporate Dividend Taxation. Cambridge Tax Law Series.

- Peterson, K., & Johnson, T. (2023). Practical Guide to Dividend Tax Strategies: Planning for Individual Investors. Financial Planning Association Press.

- The International Bureau of Fiscal Documentation (IBFD). (2024). Global Tax Guide: Dividend Taxation in Major Economies. IBFD Publications.