Key Takeaways:

- Form 1099-DIV is one of the IRS (Internal Revenue Service) tax forms that serves as an investment income reporting. For investors wondering what is 1099 div, this document includes qualified dividends, ordinary dividends, capital gain distributions, payments on foreign securities, and others.

- This document is often referred to as a dividend tax form. It contains all the information needed to calculate taxes on passive income from investing in company and fund stocks. Investors should use it when filing their tax returns.

- Brokers and other financial institutions send out the 1099 DIV to clients annually if they have received dividends and capital gain distributions.

In this article, we will explain ‘What is a 1099-DIV form?’ and ‘Why is this document important for investors with a taxable brokerage account?’

Table of Contents

Who Receives a 1099-DIV and When?

An individual will receive 1099-DIV from their broker if their investment income in the form of dividends exceeds the $10 threshold. When it comes to mutual funds, the same form is provided in case of capital gain distributions. The latter arise from the sale of stocks that are part of the fund’s net assets.

As income from assets held in retirement accounts is not taxed in the year it is received, dividend tax reporting is not required for these accounts.

All brokers and financial institutions must send investors a Form 1099 DIV by the January 31 deadline of the year following the tax year.

If the document is not received in time, the investor should contact their broker or management company (if investing directly in mutual funds). Alternatively, taxpayers can request information from the IRS to complete Form 1040. Another option is to use brokerage reports, but this approach is more labour-intensive.

If there are mistakes on the Form 1099 DIV, the investor should contact the issuer. If this is not possible, they must report the correct information on their tax return. Once the IRS has received this file, they will contact the taxpayer to resolve any discrepancies.

If a mistake is found in the income reported, an amended return should be filed.

Understanding What Is 1099 DIV: Information on Your 1099-DIV Form

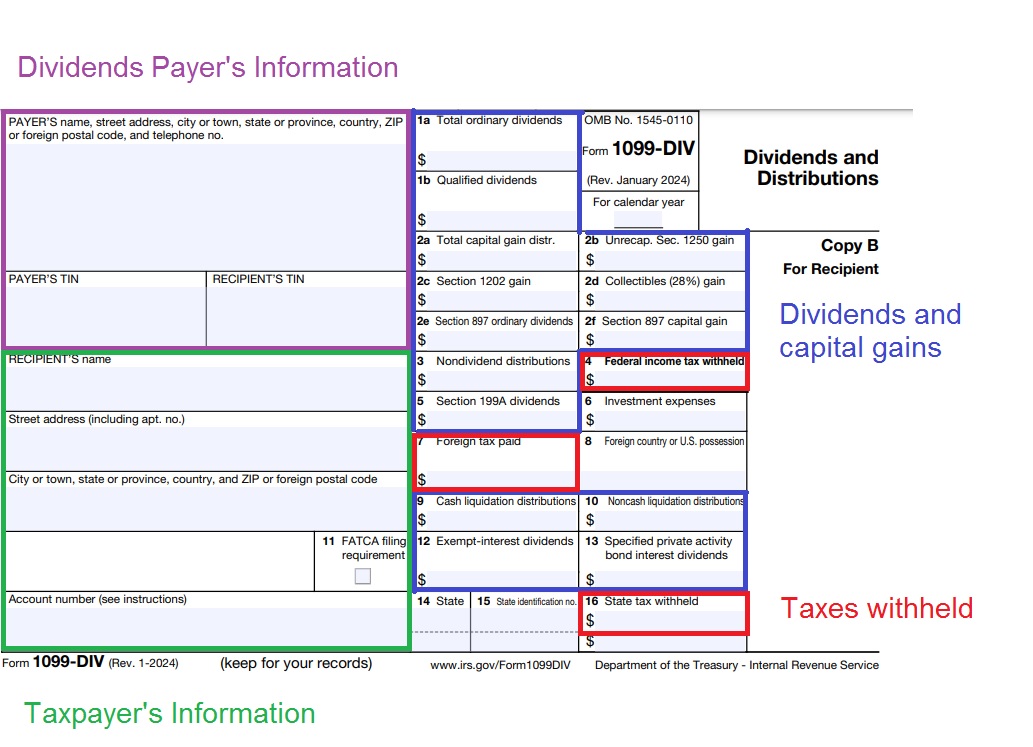

A common question among beginner investors is: what is a 1099 DIV form? Let’s take a look at the sections that make up this document. The first part of the 1099 DIV reports detailed information about the source of payments and the recipient of the investment income. This includes the recipient’s name, full mailing address and TIN.

The remaining sections of the 1099 div report the following details about investment distributions:

- dividend reporting (ordinary dividends, qualified dividends, liquidation dividends);

- information on paid capital gains (including from collectibles, real estate, etc.);

- data on other distributions not related to dividends;

- reporting of dividends on foreign securities and ADRs;

- information about investment expenses;

- details of exempt-interest dividends.

The 1099-DIV boxes also include information on federal taxes, state taxes, and foreign taxes withheld. The taxes already withheld can be found in boxes 4, 16, and 7.

The most frequently used information from the Form 1099 DIV dividends and distributions — details about qualified and non-qualified dividends. Box 1a shows all ordinary dividends received by the investor. Box 1b shows amounts that meet IRS requirements and are taxed at reduced rates.

Box 2a of the form includes details of any capital gains distributions received by the investor during the year. This primarily relates to payments from mutual funds.

Ordinary vs. Qualified Dividends: Important Tax Distinctions

The main advantage of qualified dividends is the tax benefits they offer. This type of income is taxed at the long-term capital gains rate. Depending on the investor’s income, this rate is either 0%, 15% or 20%.

Only regular dividends from U.S. corporations that pay income tax or from qualified foreign corporations can be considered qualified dividends. Income from pass-through companies, money market funds, and others is classified as ordinary dividends.

To be considered qualified, dividends must meet certain holding period requirements. For common stocks, the minimum holding period is 61 days, which must fall within a 121-day period starting 60 days before the ex-dividend date. For preferred stocks, these periods increase to 91 and 181 days respectively.

If the dividends are from a mutual fund, both the fund itself and the investor must meet IRS requirements. Hedging positions through short sales, options, or futures disqualify dividends from qualifying status for tax benefits.

All dividends that do not meet these requirements are classified as non-qualified. In this case, dividend tax rates range from 10% to 37%, depending on the investor’s taxable income.

Capital Gain Distributions Explained

Mutual funds and ETFs can generate profit from selling net assets, such as stocks and other securities. At least once a year, funds distribute capital gain distributions among their shareholders. Investors can withdraw the money paid to them or reinvest it in new fund shares. This does not affect the investment taxation.

Income received from mutual fund distributions is subject to federal taxes at long-term capital gains rates (0%, 15%, 20%). This applies regardless of how long the investor has held the fund’s securities. However, if the income is earned in a retirement account, it is not taxed in the year of distribution.

However, there are several exceptions to this rule:

- Income falling under section 1202 gain (box 2c) is not subject to federal tax.

- Capital gains from the sale of collectibles (box 2d) are taxed at a rate of 28%.

- Gains from amortizable investment real estate (box 2b) are taxed at up to 25%.

It is important to distinguish between profits from distributions made by the fund and capital gains resulting from the sale of stocks owned by the investor. If a taxpayer sells securities that they have held for less than a year, they realize short-term capital gains. This income is taxed at ordinary federal taxes (up to 37%).

What Is 1099 DIV and How to Report This Information on Your Tax Return

The tax return (Form 1040) must include a complete report on dividends. Therefore, the investor needs to obtain Form 1099 DIV dividends and distributions from each payer.

Next, a reporting on dividends must be prepared. This involves transferring information from all copies of the 1099 DIV into the appropriate boxes on Form 1040. Details of qualified dividends are reported in box 3a. Total dividends (from box 1a) should be included in section 3b. The next step is to enter information about received distributions (box 4) into the tax return.

Several important specific cases:

- If, for the tax year, the investor received dividend income exceeding $1,500, their dividend tax reporting must include Schedule B.

- If the total income of a single filer or head of household exceeds $200,000, they will also need to pay the net investment income taxes. This requires completing Additional Taxes Schedule 2. For married filing jointly and qualifying surviving spouses, this threshold is $250,000.

- Investors who own foreign securities and have had taxes withheld at source may be eligible for a foreign tax credit. To claim this credit, they must complete Form 1116 as well.

There are numerous online services that can help investors properly report their investment income tax. For individuals with substantial capital, it is advisable to consult a tax professional. A tax expert can give tax advice to ensure that income is reported correctly and that taxes are optimised.

When to File Schedule B with Your Tax Return

The tax filing requirements include the conditions under which Schedule B must be completed. Investors with interest and ordinary dividends totalling more than $1,500 must fill out Schedule B.

This document requires indicating:

- the name of each company and fund that paid dividends or interest;

- the exact amount received from each payer.

Information about interest income should be obtained from Form 1099-INT, while dividend income details are reported on 1099 DIV. Completing Schedule B does not affect the calculation of the final tax owed — it is purely for informational purposes.

Schedule B is not only required when the dividend reporting threshold is exceeded. It is also necessary when there are accounts in foreign banks or with foreign brokers, holdings in foreign trusts, and in other similar cases.

FAQ

Do I need to report a 1099-div?

Any income information reported on this form must be reflected in the tax return. If an investor receives multiple forms of this type, they must include all the data.

Why did I receive a 1099-div?

All taxpayers whose annual income from dividends or capital gains distributions exceeds $10 receive this document.

Is a 1099-DIV tax exempt?

The amounts reported in Boxes 2c and 12 are not subject to federal tax. Box 2c includes earnings from small business stocks held for over 5 years. Box 12 covers dividends from municipal bond funds, some liquidation payments, and others. However, in some cases, income that is exempt from federal tax may still be subject to state taxes or the alternative minimum tax.

What is the difference between a 1099-Div and a 1099?

Form 1099 reports income that does not fall into the wage and tip categories. This includes freelance fees, interest on deposits and savings accounts, dividends, and others. For investors wondering what is 1099 div, it is one of the types of IRS forms that contains information about investing income and dividend distributions.

Article Sources

- Graham, J. R., Michaely, R., & Roberts, M. R. (2003). “Do price discreteness and transactions costs affect stock returns? Comparing ex-dividend pricing before and after decimalization.” The Journal of Finance, 58(6), 2611-2636. https://doi.org/10.1046/j.1540-6261.2003.00617.x

- Desai, M. A., & Gentry, W. M. (2004). “The character and determinants of corporate capital gains.” Tax Policy and the Economy, 18, 1-36. https://doi.org/10.1086/tpe.18.20061890

- Poterba, J. M. (2004). “Taxation and corporate payout policy.” American Economic Review, 94(2), 171-175. https://doi.org/10.1257/0002828041301416

- Blouin, J. L., Raedy, J. S., & Shackelford, D. A. (2011). “Dividends, share repurchases, and tax clienteles: Evidence from the 2003 reductions in shareholder taxes.” The Accounting Review, 86(3), 887-914. https://doi.org/10.2308/accr.00000038