One of the most popular ways to create a diversified portfolio is factor investing. It is based on the assumption that a company has certain qualities that allow it to outperform the market and generate excess return for the owner of its stock. The easiest way to implement this approach is through single-factor or multifactor ETFs.

But investing always involves risk. A number of factor investing strategies are no exception. If applied incorrectly, such a method can only increase the chances of portfolio drawdown. Its implementation requires a deeper understanding of the market than buying a fund on the S&P 500, which is usually advised to beginners.

Table of Contents

Key Takeaways

The key thing to know is:

- Factors, or attributes, are quantitative investment characteristics that are easy to calculate.

- The essence of factor investing is that to explain the dynamics of quotations, attributes characteristic for one class of assets or affecting the financial market as a whole are used.

- Among multiple factors there are 5 key ones. Most strategies are based on them.

- The CAPM model and the Fama-French three-factor model are considered to be the foundations of this investment direction.

What is factor investing? Introduction

Factor based investing is a fairly new way of managing capital. The first works related to this method date back to 1964. The modern five-factor model was created only in 2014.

This approach to portfolio composition emerged in response to changes in the stock market – rising asset correlation, increased volatility, etc. The strategy is based on the Capital Asset Pricing Model (CAPM).

The essence of factor investing boils down to the fact that the selection of assets in the portfolio is based on a certain attribute or set of attributes.

All existing factors can be categorized into 2 types:

- Style, or smart beta (e.g. capitalisation). These are certain quantitative investment characteristics that explain price dynamics within a single type of financial instrument.

- Macroeconomic (e.g. inflation rates) – indicates broad investment risks, applies to multiple asset classes at once.

Certain factors, such as momentum, work through market inefficiency. It is caused by investors’ behavioral biases. These can be briefly described as the fact that most people sell “winners” too early and hold “losers” for too long.

The modern financial industry makes investing accessible even with little spare time or lack of knowledge. Factor strategies are not an exception. You can build a portfolio based on it with the help of a factor fund that copies the corresponding index. For example, iShares MSCI USA Quality Factor ETF, iShares MSCI USA Momentum Factor ETF, etc.

There are a number of advantages to this style of investing:

- More competent diversification and asset allocation. Achieved by avoiding a link to market capitalisation. Given that different factors are more effective in different periods of the economic cycle, a multi-factor approach will work best.

- Potentially higher returns. Factors are properties of assets that in the past have generated higher returns at similar or lower risks.

- Lower pairwise correlation of factors (compared to the correlation of different asset classes).

The factor approach has several disadvantages. The key one is that the return on a particular attribute can be cyclical. But the same property exists across most asset classes.

Another important disadvantage occurs if an investor emphasizes only one of the factors. This leads to deterioration of portfolio diversification and increased risks.

For example, one possible factor is the size of the business. Small-capitalisation companies are believed to generate higher returns than market giants over a long horizon. But trying to focus only on this attribute is fraught with severe portfolio drawdowns.

Types of factors

The most important types of factors available to apply in an investment strategy are discussed below.

Macroeconomic factors

This category includes events and conditions affecting all asset classes. They capture the broad risks that affect the market as a whole. This includes such investment factors as:

- Economic growth. This is a positive period during which consumers increase their spending. As a result, companies’ profits increase. As a consequence, their valuation by investors increases. Therefore, this is a favorable time to invest in stocks.

- Real rates. The higher the Fed Funds rate, the more expensive it is to lend. This leads to slower business development. First, companies find it harder to borrow money to expand. Second, consumers shift to a savings model and cut back on their spending. That means profits are falling. Rising interest rates are negative for equities.

- Inflation. This is another negative factor for the broad market. Customers’ incomes cannot keep up with prices. As a result, people reduce their consumption. And consumables and other stuff become more expensive. As a result, company profits fall. In periods of high inflation, the business whose customers cannot reduce consumption, such as utilities, health care, etc., wins.

- Credit. An attribute such as the creditworthiness of a company is under consideration here. By investing in stocks and bonds, one assumes the risk of default. Selection of assets by the probability of the latter occurrence is one of the options of factor investing.

- Emerging markets. These markets have higher potential returns on both stocks and bonds. However, there are additional risks relative to developed markets. First of all, political and sovereign risks.

- Liquidity. The liquidity of an asset is assessed by the trading volume and the spread between sell and buy orders in the stack. There are additional risks associated with illiquid assets. For example, if an investor wants to sell them quickly, they will be forced to sacrifice part of their income.

Style factors

Style factors affect returns and risks within the same asset class. When it comes to equities, this category includes:

- Value. How fairly or unfairly the company is currently valued by the market.

- Minimum volatility. The beta coefficient, or market risk factor investing, is considered the first factor proposed. The author of this concept was W. Sharpe, who published his work in 1964.

- Momentum. By mentioning this we mean medium-term dynamics of quotations. In fact, investing on the basis of this factor alone turns into trend trading on large timeframes.

- Quality. This refers to the properties of the business that are reflected in the company’s balance sheet, such as equity return.

- Size. Public companies are divided into several categories depending on their market value (capitalisation).

- Carry. This refers to an incentive that encourages an investor to invest in riskier assets. That is, the yield on equities should be higher than the rates on risk-free instruments, such as treasuries.

What are the 5-factor funds?

There are many attributes that can be used to form a portfolio. But 5 of them are considered key ones. They are discussed in detail below.

Value

This is the well-known value investing based on the works of B. Graham. There are stocks that are valued by the market below their “intrinsic fair value”. They may yield higher returns in the long run than overvalued, popular stocks.

It is believed that this theory works because market participants are pessimistic about slow-growing securities. Meanwhile, they are too optimistic about stocks demonstrating stable and fast growth of quotations. But over long horizons, a company’s quotes inevitably follow its earnings. This means that stocks having low prices relatively have much more potential.

Statistics show that value investing can yield higher returns than buying “popular” higher priced stocks. But it may take a few years for quotes to approach “fair” value.

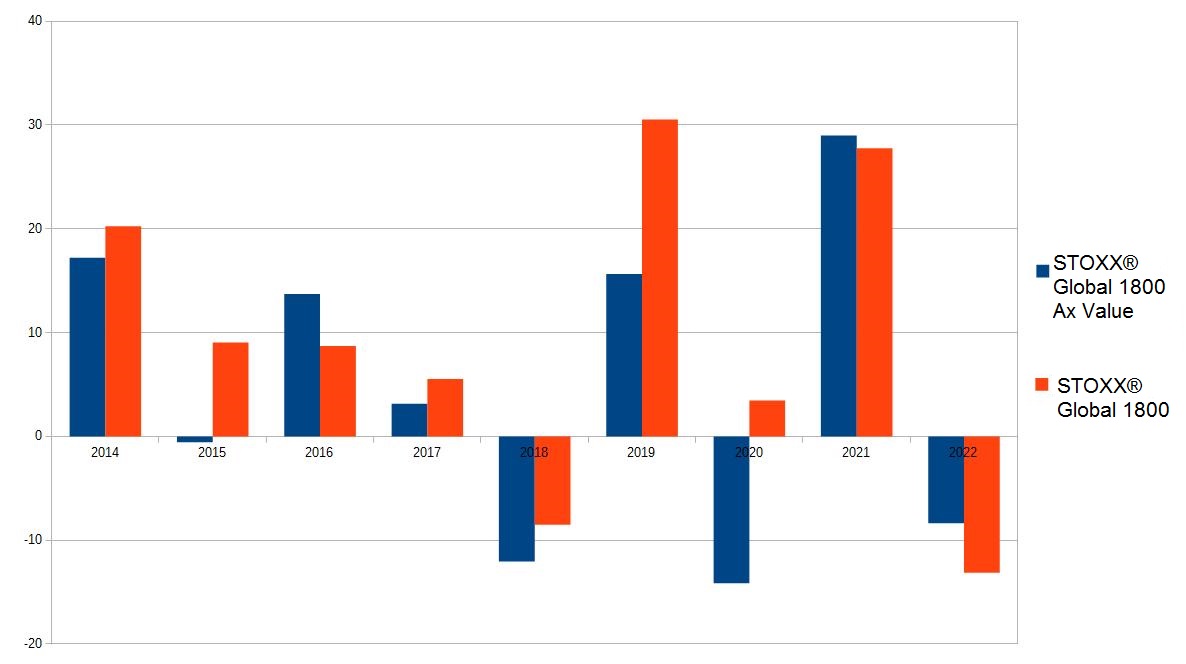

For example, in the past decade, growth companies won. Below is a chart based on the STOXX® Global 1800 index family. The values for the last trading day of the year are taken to create the chart. It shows in percentages how the general index and the value stock index have risen or fallen.

The cumulative growth of the company value-based index over the years reviewed was 41%. While the underlying STOXX® Global 1800 Index grew by 106%.

The main difficulty in using the low cost factor in your strategy is to correctly value the stock. The simplest method to find out if a stock is overbought is to calculate P/E and P/B multiples and compare them to competitors.

Quality

This is one of the most controversial sections. Experts have no consensus on what qualities a promising company should have in terms of profitability. The following factors are most often mentioned:

- high profitability;

- stable cash flow;

- moderate borrowing capacity.

Also, a “quality” company should have a strong competitive advantage compared to market participants.

The minimum criterion for building a portfolio on the basis of “quality” is high return on equity. There is statistical research confirming that on average quotations of such companies outperform the market.

High-quality stocks can be called securities that have a higher Sharpe ratio.

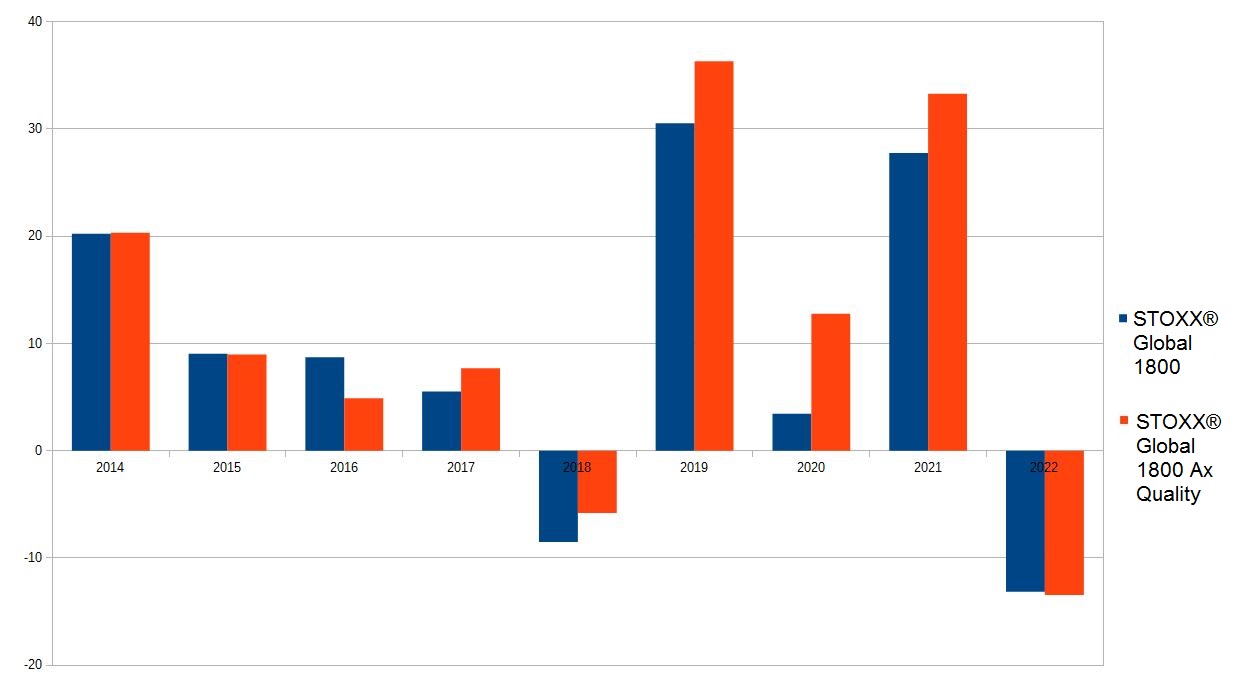

The chart below demonstrates that the stock selection strategy for the “quality” factor has been effective for most of the 2014-2022 period.

The cumulative growth of the STOXX® Global Ax Quality index over the years considered was 147.5 per cent. While the benchmark STOXX® Global 1800 Index grew by 106 per cent. The idea of investing in quality companies has proven its worth.

This index performed the best over the period under review, outperforming even the multi-factor strategy. But the evidence that quality companies are more profitable has not been available for a long time. In the early years of the factor investment theory, no statistical evidence could be found.

Momentum

The investment strategy that takes into account the momentum factor is based on the works of N. Jegadish and Sh. Titman. The idea was first published in 1993. The idea boils down to the fact that stocks that have shown strong dynamics in the medium term will continue to grow. A period from 3 months to a year is used to search for proper securities.

The reason for this phenomenon is explained by the inefficiency of the market. Many private investors underestimate the real performance of the company. They pay their attention to it already after the quotations started to grow. Under the influence of FOMO, they enter the asset, which has performed well in recent months. This gives even more bullish momentum. The price continues to rise.

This lasts until an important negative factor appears. For example, the company will become overvalued and experienced market participants will start fixing profits. It will lead to a decrease of quotations. Further the “crowd effect” will come into work again and the price of stocks will continue to fall.

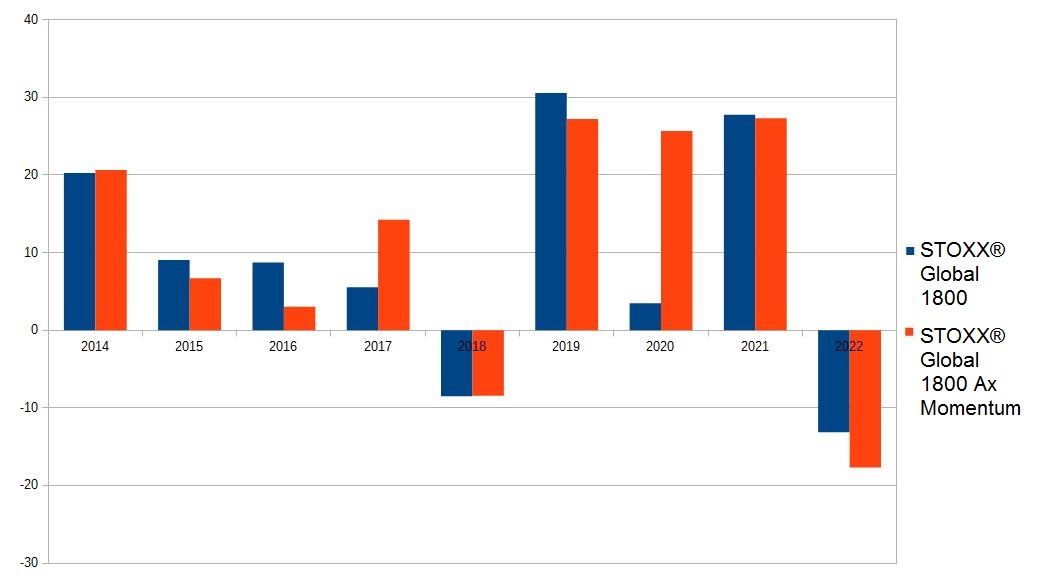

The diagram below shows how the dynamics of the STOXX® Global 1800 Ax Momentum index differed from the movement of the underlying STOXX® Global 1800 index.

The total growth of the STOXX® Global 1800 Ax Momentum Index over the years reviewed was 132%. While the benchmark index grew by only 106%.

Size

This paragraph refers to the classification of companies by capitalisation. It is believed that the business, which belongs to the Small Cap category, gives a higher yield in the long term. High growth potential is due to the fact that such issuers are usually at the extensive development stage.

High returns are a risk premium. The probability of bankruptcy of a small company is higher than that of a market leader. In addition, such businesses often do not have a stable cash flow.

Another important factor is less liquidity of stocks. An investor may face high spreads or not find a counterparty at all when trying to sell assets. Therefore, it is more advisable to invest through ETFs rather than directly.

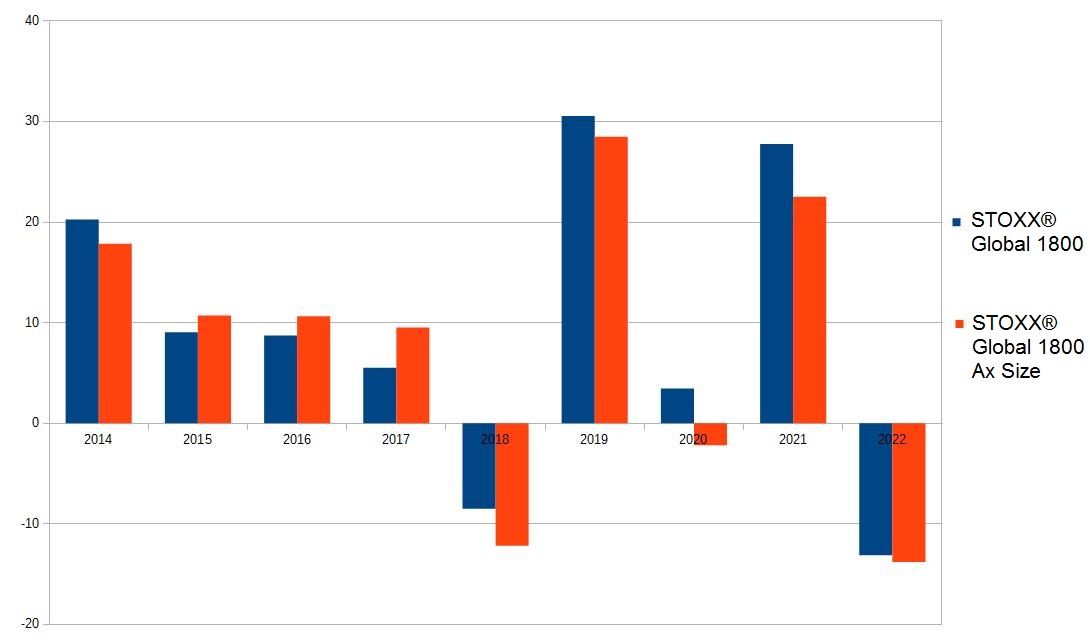

A comparison of the performance of the STOXX® Global 1800 Ax Size Index with the underlying index is shown in the chart below.

In terms of the final result for the period, the idea of selecting companies by size did not pay off. The growth of the STOXX® Global 1800 Ax Size index was only 84% against 106% for the base indicator. To a large extent, this loss was due to the fact that investors looked for more reliable assets in times of crises.

Minimum Volatility

The idea of selecting stocks in a portfolio based on this factor is that stocks with lower volatility have higher Sharpe ratios. They yield higher returns than highly volatile assets. But only when considered on a risk-adjusted basis. Such investments are more proper for conservative and moderate investors.

The main criterion by which you can quickly determine the stock price volatility is the beta coefficient. It determines how much the quotes of an asset move faster than the broad market. It can be found on various investor services.

When beta is above 1, it means that the stock price fluctuates more than the underlying index. When beta is less than 1, the stock is considered low volatility, proper for conservative investors. This indicator is calculated relative to the average market volatility. For US companies, the S&P 500 is usually taken as the “benchmark”.

The key disadvantage of this approach is that the beta coefficient reflects only past performance. It does not take into account the current situation in the economy and changes in business.

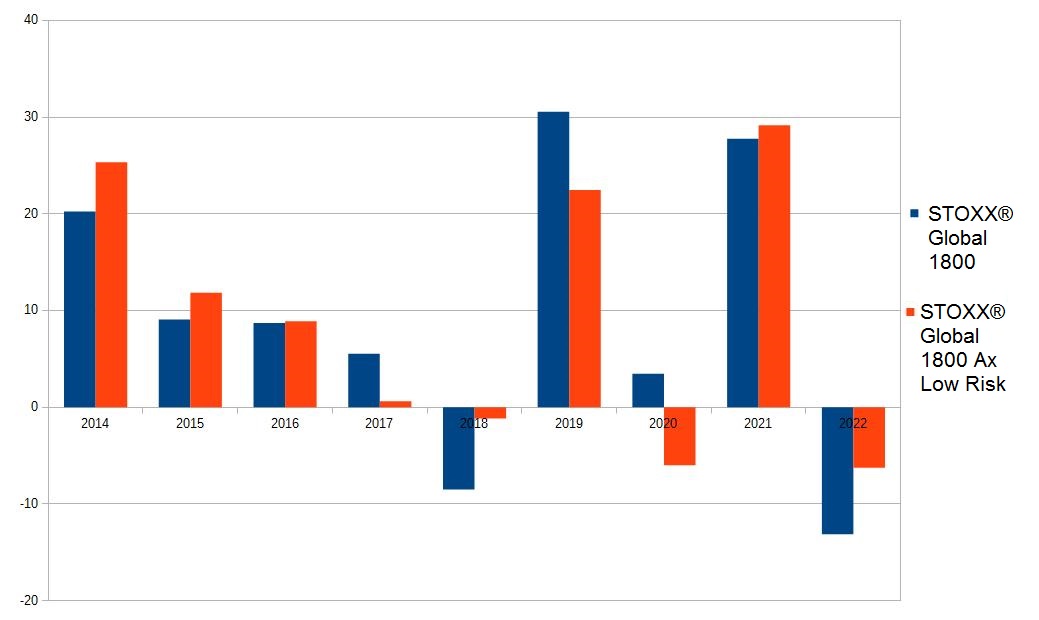

By results of the period the factor index of minimum volatility has not exceeded the basic one. It grew only by 111% against 106%.

Factor-based strategies

Factor based strategies can be implemented by themselves or through the purchase of ETFs. The key objective of such funds is to outperform classic options based on asset allocation by capitalisation. The commission of such ETFs is usually lower than that of actively managed funds.

Let’s consider the advantages and disadvantages of several popular strategies.

Outperformance

BlackRock Management Company refers to this factor investing strategies as all funds based on a single style factor.

Most of these ETFs follow an index that reflects the attributes listed above. For example, a fund that invests in quality companies is based on a benchmark that considers 3 indicators:

- the return on equity of the company;

- variability of earnings;

- debt-to-equity ratio.

In addition to stock funds united by one of the above mentioned style attributes, factor bond funds are represented on the financial market. We can distinguish 3 investment factors on the example of corporate bonds:

- duration;

- inflation protection;

- credit risk.

For stocks, besides the 5 main factors listed above, there are many other less popular factors. For example, companies can be categorized according to the following criteria:

- growth rate;

- buyback activity;

- dividend stability;

- dividend size, etc.

But these criteria are less popular. Not every management company offers funds based on such attributes.

A factor strategy is not always a low-risk investment. For example, for some institutional investors, regulatory requirements prevent them from using leverage. They can get potentially higher returns through a factor such as maximum volatility.

The disadvantage of factor based funds can be understood by studying the charts above. They clearly show that none of the 5 popular factor based investments provide results that outperform the broad market year after year. According to the results of several years, some factors managed to show returns above the broad market. But when another period was used as a basis for calculations, the result would be different.

For example, such a factor as the company’s being among dividend aristocrats. For 2005-2020, the average annual total return of the S&P 500 Dividend Aristocrats index was 11.9% versus 10.9% for the S&P 500. When the last 10 years are taken as the basis for the calculation, the result is the opposite – 12.81% versus 11.83% in favor of the S&P 500. This is due to the strong performance of growth companies, which typically do not pay dividends.

Reduced volatility

This is a single-factor strategy, the essence of which is to select low-risk stocks. At the same time, the investor has the opportunity to diversify the portfolio by adding companies from different countries.

Examples of funds that follow such a factor strategy:

- iShares MSCI EAFE Min Vol Factor ETF (EFAV) – invests in large and mid-capitalisation companies in developed markets excluding the US and Canada;

- iShares MSCI USA Min Vol Factor ETF (USMV) – net assets consist of stocks of U.S. companies with low volatility;

- iShares MSCI Emerging Markets Min Vol Factor ETF (EEMV) – invests in low volatility emerging markets stocks.

The combination of these 3 funds represents a well-diversified portfolio in terms of country affiliation of issuers and currency of assets. This compensates for the fact that the factor investing strategy is based on just one attribute. An alternative to them is the iShares MSCI Global Min Vol Factor ETF, which covers both developed and emerging markets at once. The companies listed are an example, not investment advice.

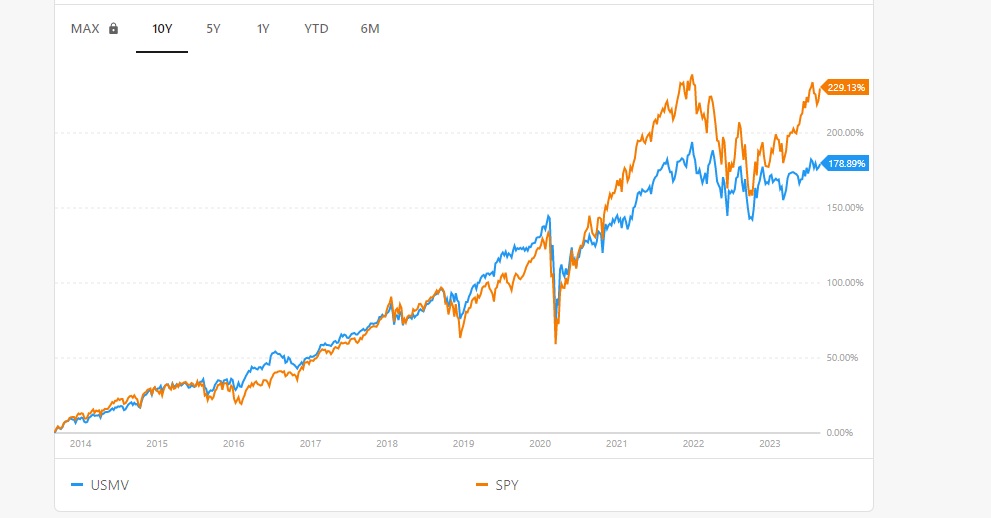

When diversification is ignored and only U.S. stocks are taken into account, you can see that this strategy does not always work. Below is a comparison of the portfolio growth graph over the last 10 years when investing in USMV and SPY funds.

The figure shows that from mid-2020, the low volatility strategy began to lose out to the S&P 500 index. The example of the STOXX® Global 1800 Index showed above that in the international format, this strategy slightly outperforms the broad market over the 2014-2022 period.

The USMV fund quote chart has a smaller amplitude of fluctuation than SPY. This may be important for investors seeking to minimize risk factors. That said, there is no guarantee that ETFs with minimum volatility will not show large price swings. At some point, the strategy may not be effective.

Diversification

As the name suggests, a multi-factor portfolio strategy includes several factors at once. The key challenge for the investor is to choose which factors should be considered and how much importance should be attached to them.

A multi-factor strategy can be of several types:

- Combined. In fact, it is a combination of several single-factor models. Leading stocks in each segment selected by the investor are added to the portfolio.

- Consecutive. With this approach, the investor first sorts assets by the first selected attribute, then by the second, etc.

- Intersectoral. When it is implemented, stocks are selected that overlap in terms of factors. That is, the company should be a leader in a number of criteria at once.

The multi-factor investments model can be applied not only to stocks. When macroeconomic indicators are taken (inflation, interest rates, etc.), this strategy can be used to build a diversified portfolio from different asset classes. An example of a fund is the Total Factor Fund (BSTIX) from BlackRock. In addition to stocks, it invests in debt securities, derivatives, real estate, etc.

When an investor is only interested in stocks, an example of a multi-factor strategy is the iShares U.S. Equity Factor ETF (LRGF). It combines U.S. companies selected based on the 5 characteristics listed above.

In fact, applying multi-factor strategies is one of the many ways to diversify a portfolio. Its advantage is in removing the link to the company’s capitalisation.

Any fund that replicates popular indices possesses this disadvantage. For example, the NASDAQ-100 ETF includes 100 companies. At first glance, this is good diversification. But about 60% of net assets are in only 10 of them.

Funds that use factor investing are devoid of this disadvantage. They are well diversified. And this is one of the cornerstones of investing.

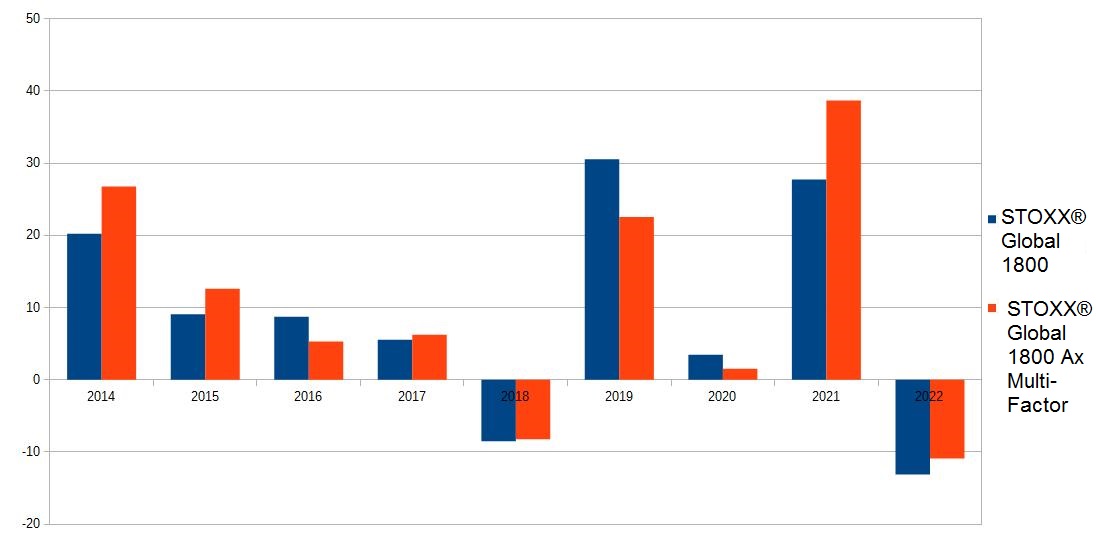

The chart above demonstrates that the STOXX® Global 1800 Ax Multi-Factor Index outperformed the STOXX® Global 1800 Index not each year between 2014 and 2022. On a compounded basis, it was up 125% versus 106%. This is a strong argument for the strategy’s effectiveness over the long term.

Risks of factor investing

There are a huge number of strategies based on a combination of different factors. But in any of them, several key risks factor investing will play an important role.

Cyclicality

You can find statistical evidence that companies grouped by some attribute yield higher returns than the broad market. But there is no single factor that produces this result over decades. In different periods, one property or another is favored.

Distribution of yields

Statistical calculations show that the distribution of portfolio returns when investing based on one of the factors is very different from the normal distribution. Large performance outliers appear more often than when investing in the broad market.

Reliance on historical data

Factor investing is based on finding common characteristics in companies that have shown above-average returns in the past. It takes into account only historical data and tries to make forecasts of future profits using this data.

It does not take into account that the current market situation is different from that of even a decade ago. All investors are well aware that past returns are no guarantee of future results.

Risk of data mining

Here we are talking about the so-called selection bias. When publishing the results of statistical studies, the emphasis is on those factors that have shown a good result in retrospect. However, it may be difficult to say which of the 2 causes led to it:

- factor exposures are indeed a prerequisite for high profitability;

- the time period analyzed was fortuitous for companies with this attribute.

In addition, most historical data is based on periods when little money was invested in factor based strategies. An influx of capital can change the situation and negate the advantage of a factor.

Is factor investing good?

Factor funds are an efficient and low-cost alternative to actively managed funds in terms of fees. They can be used to achieve different investment objectives, for example:

- increase portfolio diversification by not being tied to capitalisation;

- manage risk (e.g. buying a fund on low volatility companies reduces the overall portfolio volatility);

- implement strategies related to a negative factor (e.g., in anticipation of a recession, add a low-volatility stock ETF to the portfolio), etc.

Multi-factor ETFs are a well-diversified set of assets. It is believed that their use allows an investor to worry less about portfolio rebalancing.

Factor investing is the answer to the declining performance of classic strategies. However, it is by no means devoid of its own disadvantages. We cannot ignore the fact that it took 50 years for this idea to gain popularity.

Some experts believe that the concept of factor investing in its current form is flawed. In their opinion, it cannot be used as a full-fledged substitute for funds copying classic stock indices (S&P 500 and others).

In reality, there is no guarantee that the performance of exchange traded funds selecting companies on some basis will be better in the future. On the contrary, certain factors may reduce a company’s performance in certain market environments.

An ETF must adhere to the targeted investment factors stated in its prospectus. Even when the underlying index strategy that the fund copies is not profitable, it cannot be changed. That means such an asset may remain unprofitable for years.

Independent factor investing or investing in appropriate ETFs is useful for someone who has a good understanding of when a factor provides an advantage. For a beginner or a passive investor who wants to stick to a buy-and-hold strategy for decades, this approach may not bring the results expected.

Conclusion

The idea of relying on certain attributes to select stocks dates back to 1964. It took 50 years to evolve into its modern form. The main disadvantage of factor strategies is that they only consider past performance. That said, they are subject to cyclicality. Periods when a factor performs well are followed by periods when the stocks that possess it, on the contrary, perform worse than the market.

Despite this, multi-factor ETFs are a promising alternative to the classical approach to investing. There are already about 300 such funds on the US market. Their use is one of the ways to reduce portfolio risks. When an investor only focuses on one factor, there is a chance that the opposite will result in a worse-than-average performance.