The FIRE strategy boils down to building equity to cover financial needs. This allows a person to become independent of active sources of income or social support.

The first challenge is to determine how much money you’ll need in order to retire comfortably. It should be enough for a longer-than-average life expectancy. Another challenge is choosing the best savings rate.

Everyone has a unique path to economic independence. The FIRE allows 5 main approach variations. Their adherents differ in their savings rate and retirement plans.

Table of Contents

What Is Financial Independence, Retire Early (FIRE)?

The acronym FIRE stands for Financial Independence, which allows you to stop working for money. It is not known who first suggested the use of this acronym.

The idea of early retirement gained momentum in the 1990s. It gained popularity largely due to the book Your Money or Your Life by Vicki Robin and Joe Dominguez. This best-selling book was published in 1992. In the decades since, the number of people who want to retire early has grown.

What is the FIRE movement?

FIRE is a movement that prioritizes financial independence. The main goal is to build a capital that will allow you to fully support yourself and your family. Thanks to this, a person can maintain the desired lifestyle without a salary and social benefits.

Full financial independence makes it possible to retire earlier. We are talking about the age of 35-40 years. The traditional retirement age of 65 in Canada and 67 in the United States.

In most cases, FIRE requires 3 factors to be achieved:

- extreme savings;

- steady increase in active income;

- investment and creation of passive income streams.

FIRE often has a connotation of retirement from activism. But in fact, many FIRE participants continue to work after going into business for themselves. They also devote time to volunteer work and other community service.

The Cons of the FIRE Movement

There are some cons of pursuing FIRE movement:

- The danger of sacrificing too much in an effort to save and invest as much as possible. FIRE supporters rob themselves of the joy of living in the here and now.

- The concept of the FIRE movement may create the perception that having to work is a problem. Delayed Life Syndrome contributes to this negative perception.

- Retiring early may lead to a sense of loss of purpose and empty time.

- Followers of FIRE family and friends are often interested in different lifestyles. The idea of over-saving can lead to conflict and isolation from loved ones.

One of the main negative aspects of the FIRE is that the Fire may be the risk of running out of money in old age. Life is unpredictable and makes adjustments to any plan. A person may face unforeseen medical expenses, a sharp increase in inflation rates, etc.

The best option is to save enough so that your passive income can cover living expenses. The capital is not used in this process.

But this means that a much larger amount will be needed for retirement. This can lead to a situation where people spend decades on everything. At the same time, they work less for only 5-7 years.

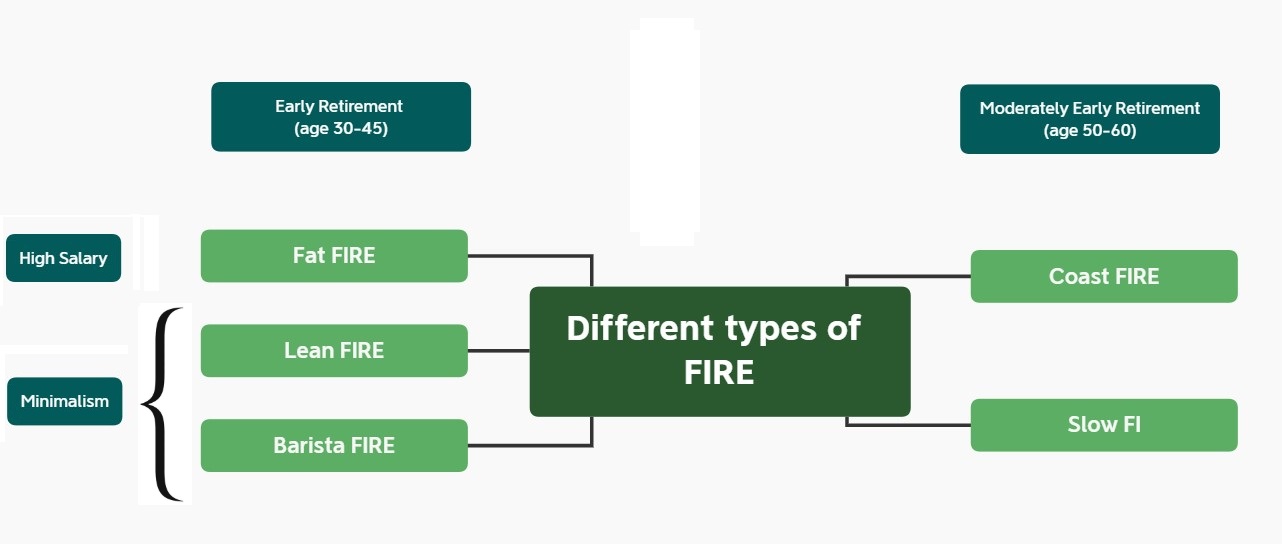

5 Types of FIRE & Variations Of Financial Independence Early Retirement (F.I.R.E)

Adherents of the savings and investments ideology have one goal – become financially independent. But everyone views the FIRE lifestyle differently.

Followers of this movement are divided into several subgroups based on criteria such as:

- the degree of asceticism one observes;

- current income level and savings rate;

- plans for life after reaching the financial goals, etc.

There are 5 different types of FIRE, which are discussed below.

Fat FIRE

Fat FIRE may eschew the idea of extreme frugality. They live comfortably, do not skimp on clothing and equipment, and travel extensively.

The main way to achieve financial independence in this case is a high salary. It allows us to build up capital without limiting consumption. Often such people achieve greater financial success than followers of radical austerity.

Lean FIRE

This is the classic stereotypical image of a person seeking financial self-sufficiency. The idea requires minimizing cost of living.

Followers of this movement invest most of his or her income. At the same time, they plan to retire and live the same modest life. This form allows you to shorten the period of active work by reducing capital requirements.

It is possible to reach financial independence on a low salary by living a minimalist lifestyle.

Barista FIRE

This form cannot be considered fully independent. It is level 5 on Grant Sabatier’s Stages of Financial Liberty scale.

The essence is that a person strives for minimal spending. At the same time, they do not want to give up work completely. They plan to switch to a light part-time job.

Thanks to their part day jobs, Barista employees have plenty of time to pursue their hobbies. They still receive health insurance and other benefits from their employer.

In addition, the person receives a small income. This means that much less capital is required, one does not need to save as strictly. The willingness to keep working reduces the time needed to make the FIRE journey.

Coast FIRE

The Coast FIRE approach is not about retiring early. Its proponents want to maximize the benefits of compounding.

Coast FIRE also follows a strategy of maximizing savings and accumulation between the ages of 20 and 40. During this time, they build their retirement nest egg.

For the remaining 20 years, the money you put aside is multiplied. This is accomplished by reinvesting dividends and increasing the value of securities.

Let’s say a representative of the Coast FIRE movement accumulates $1 million in the first 20 years. Consider how that amount changes over the second 20 years. Assume an average annual return of 6%.

Coastal FIRE participants typically retire at age 60. By that time, they have enough capital to live comfortably.

Slow FI

This is the name given to people who move slowly toward their FIRE goals. Advocates of the classic early retirement approach focus on ages 35-40. Slow FIs are ready to reach their FIRE number by age 50-55.

There are several reasons for this:

- unpreparedness for extreme savings;

- low income;

- desire to have a large family, etc.

Followers of the Slow FI approach give up the obsession of trying to achieve financial freedom as quickly as possible. They combine reasonable savings with a comfortable level of consumption.

The core concept of Slow FI is that life should be as comfortable before you achieve the Fire goal of yours as it is after. This helps to lower stress and build a healthier relationship with money.

How does FIRE work?

The most popular financial advice is to put 10-15% of your income into a retirement account. Most followers of the FIRE movement work on extreme saving. Their goal is to save 50-75% of their paycheck.

Determining your savings rate is considered one of the most important steps. It depends on your current income, marital status, and other factors. The main thing is that a person should be able to keep around financial discipline for many years.

In addition to cutting expenses, FIRE followers try to increase their active income. This is done through career advancement and part-time work in their spare time.

The money saved is used to create sources of passive income. First of all, we are talking about investments in securities. For example:

- treasures (on November 16 United States 30-Year Bond Yield is 4.599%;

- stocks or ETFs (SPDR® S&P 500 (SPY) gives dividend yield about 1.19%);

- REITs (on November 16 Realty Income Corp (O) gives dividend yield about 5.59%).

You may also want to consult with a certified financial planner. He or she can help you develop investment strategies that are consistent with your risk tolerance.

The traditional FIRE number is a person’s annual expenses multiplied by 25. But this is only one of many recommendations. Everyone must decide for themselves what amount of capital is acceptable.

How Many People Achieve FIRE?

The number of people who have completed a FIRE plan and met their financial objectives is unknown. There are no official statistics on the movement.

Motley Fool experts conducted a study between 2016 and 2022. According to their data, only 3% of Americans will retire between the ages of 40 and 49. Another 17% will retire between the ages of 50 and 59. But these percentages are calculated from the country’s total population, not the number of FIRE adherents.

The Employee Benefit Research Institute published different information in 2023. According to their data, 33% of Americans surveyed stopped working before age 60.

FAQ

What is the 4% rule for FIRE?

The rule means that a retiree can safely withdraw only 4% of the accumulated amount in the first year. In the second year, the amount is increased by the official inflation rate. The same happens in the third and subsequent years.

What are the 3 major types of financial?

There are several forms of FIRE. The main 3 are Lean, Barista, and Fat one.

What is the 5 rule for financial freedom?

Capital generates passive income. For example, dividends or interest on a deposit. The rule is that this money must cover at least 5% of the investor’s expenses.

What is the 25x rule for retirement?

This rule helps you calculate the amount of money you will need for retirement. It states that the amount of savings should be 25 times your current annual income.

What is the logic behind the 4% rule?

The 4% rule was invented for people who stopped working at the traditional age of retirement. It is based on a relatively short life expectancy. Early retirees are advised to reduce their withdrawal rate.

How long will money last using the 4% rule after retirement?

If you withdraw 4% of the initial amount, the capital will last for 30 years. This duration is based on favorable circumstances (low inflation, prevailing bull market in stocks). Much also depends on the asset allocation chosen by the investor.

What is the $1000 a month rule for retirement?

Financial advisors say that $240,000 in an account allows you to spend $1,000 per month. For example, a person who has $960,000 (4×240,000) set aside can spend $4,000 each month.

You Might Also Like

- What Makes a Dividend Qualified? IRS Rules Explained

- Understanding Forward Dividend Yield: The Complete Guide

- High-Yield Dividend Aristocrats: Top Stocks for Consistent Income

- APY vs Dividend Rate: Which Matters More for Your Returns?