Table of Contents

13 Best Asset Classes For Beginner Investors

Contrary to popular belief, investing for beginners is a task that even students and people with little income can accomplish. Thanks to advances in technology and competition among brokers, stock trading is becoming more and more accessible.

But this does not eliminate the need to study the basics of financial literacy. This is the only way a person to make better investment choices, improve them, and achieve her financial goals.

The best asset classes to invest for beginners

There are many asset classes that can be used to preserve and increase capital. Below, we discuss several investment options. Each of them may be suitable for a person who is new to investing.

1. High-yield savings accounts

In fact, it is not an investment tool, but a way to slightly increase your income from temporary placement of free money in short-term funds. These saving accounts are great for keeping a safety cushion and having the necessary cash just in time when the next big pre-planned buying opportunity emerges.

High-yield savings accounts are usually opened through an online bank or credit union. This allows for a small bonus to the interest rate. As a result, a person investing in high-yield savings accounts retains the ability to dispose of her money at any time. Typically, the interest rate of HY savings accounts is higher than the average yield of regular checking and savings accounts, interest is compounded daily and credited every month.

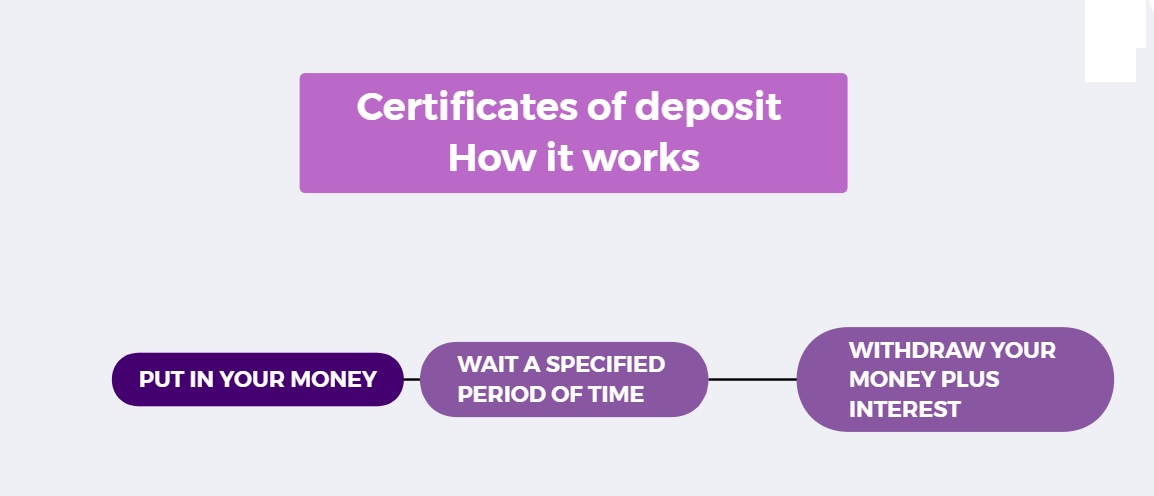

2. Certificates of Deposit

Using certificates of deposit to hold money can earn interest even higher than high-yield savings accounts.

But you should consider that the owner of the capital loses access to it. You can’t get your money back before the deadline. This will result in a loss of interest or even having to pay a “penalty” to the bank.

Usually a certificate of deposit can be purchased for 6, 12, 18, etc. months. But there are also more original terms, such as 13 or 21 months.

The advantages of a certificate of deposit for beginners in investing are a guaranteed return on investment and a full return on investment within a specified period.

3. Bonds

A bond is a fixed-income debt security issued by a corporation or government, and traded at the bond markets. Bonds come in many varieties:

- Government bonds

- Municipal bonds

- Corporate bonds

- Mortgage bonds

- Bond ETFs and bond funds

The most popular are short-term bonds, which regularly pay interest income (coupons) to the bondholder.

For example, an investor buys a $1,000 bond with a coupon rate of 5 percent and five years to maturity. In effect, this investor loans money to the issuer of the bond and the issuer is obliged to pay it back with a fixed interest. As a result, our investor would receive $50 annually for the next 5 years and then will get her $1,000 investment back.

There are types of bonds which do not have to be held to maturity. If, during this time, the market value of these debt securities increases, an investor can sell them for more than he bought them and take profit from the difference in value.

Bonds can be issued by both private companies and the government, represented by the Treasury. Depending on the issuer, credit risk (the likelihood of default on debt) is priced in the bond market. The higher it is, the higher the interest income the bondholder receives.

But when starting to invest in bonds, you need to keep in mind all the risks. For example, the issuer of a bond could file for bankruptcy.

In addition, if an investor wants to get his money back before the maturity date, there is always a risk that the bond price corrects, and an entire bond portfolio can only be sold at a loss.

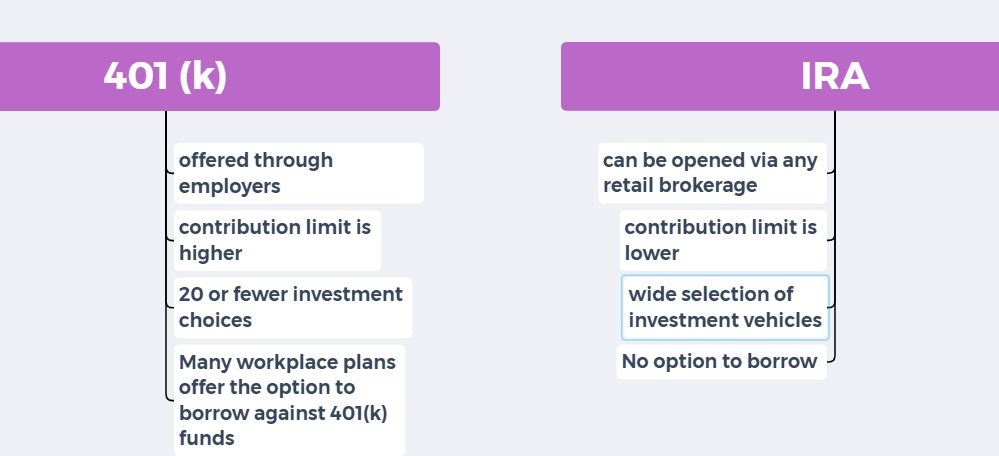

4. Individual retirement accounts

Investing for beginners by investing into retirement plans has a number of solid points worth of consideration:

- can be used by a person with minimal knowledge of the stock market;

- discipline in terms of regular deductions;

- provides an opportunity to receive additional income at the expense of the employer’s pension program.

The essence of investing in a retirement plan is that a person regularly transfers a predetermined amount of money to the fund. The fund manager puts this money into a portfolio of securities and rebalances it regularly — when an investor’s retirement gets closer, the percentage of risky assets in her retirement plan diminishes.

Many companies offer 401(k) retirement accounts to their employees. In addition to contributions from a beginner investor’s salary, the employer transfers an additional amount of its own money to his or her 401(k) account.

With a 401(k) retirement plan, the amount invested is tax-free. But it will have to be paid when an investor reaches the retirement age.

A Roth 401(k) assumes that contributions will be made to the retirement fund after taxes on income. But it won’t be withheld in retirement. This and more should be considered when choosing a traditional or Roth IRA.

5. Mutual funds

This investment vehicle is great for a beginner investor with little spare money who doesn’t want to spend a lot of time learning how the stock market works.

A mutual fund is a pooled capital of hundreds of thousands of investors. The management of a mutual funds then invests money in a wide range of assets.

The price of mutual fund shares owned by an investor is directly related to the value of the net assets in which that fund’s money is invested. If the value goes up, the value of the investor’s assets also goes up. So, she can make money by selling them at a higher price than the purchase price.

The second potential source of income when investing in mutual funds is dividend payments (if implied by the investment strategy). The price of a mutual fund stock is calculated once per day. It changes relative to the previous day after 4 p.m. Eastern time.

Fluctuations in the price of one of the companies whose shares are part of the net assets have little effect on the price of the fund’s securities. This effect is achieved through diversification — investing in a diverse asset types that poorly correlate with each other.

A novice investor with little capital can never achieve such a degree of diversification alone, because it requires hundreds of thousands or even millions of dollars. The price per share of a mutual fund is much lower. The initial fee to participate in a mutual fund investing is usually a few thousand dollars. But one can also find options where $100-500 will suffice.

The difference between a mutual fund with an active strategy and an index fund is that the management company does not simply copy a particular stock index, but tries to outperform its performance.

Often this turns out to be a negative factor. According to statistics, less than 11% of mutual fund management companies consistently outperform the S&P 500 index. The commission of mutual funds with active strategy is noticeably higher than that of index funds. It reaches 0.5-1%.

6. ETFs

An ETF is an exchange-traded collective investment fund. As with mutual funds, the price of a stock is directly related to the value of the net assets owned by the fund.

But there are a few important caveats that make this investment tool more profitable for a novice investor:

- An ETF is an index fund, so management fees are noticeably lower (0.1% or less).

- The price of ETFs changes every second, as well as the price of shares of individual companies, you can buy them at any time when the stock exchange is operating, at a cost closest to their fair value.

- ETFs have minimal investment requirements.

The minimum lot that can be purchased is one ETF share. Its price depends on the chosen fund and sometimes reaches hundreds of dollars. In the list of the most popular funds, there are inexpensive ETFs, whose securities are valued at $10-30.

Most often, ETFs track a certain index. But ETFs’ net assets aren’t necessarily stocks or bonds. They can include metals, commodities and even cryptocurrency.

The principle of earning investment income from ETFs is identical to that of mutual funds. The investor receives regular dividends and can sell the stock at a higher price than he bought it.

7. Stocks

Buying individual stocks is one of the riskiest investment options for a beginner investor. Like mutual funds, stocks can generate two types of income — positive differences between the sale and purchase price and dividends (but not all companies pay them).

If we are talking about long-term investing and capital accumulation, the minimally profitable horizon in stock market investing, according to experts, is 5 years. According to Warren Buffett, “If you don’t think about owning a stock for 10 years, don’t even think about owning it for 10 minutes.”

Short-term investing (day trading) and trying to speculate on stock price fluctuations are not good for novice investors. In fact, even most seasoned traders routinely lose their money in day trading.

The main risk of the stock market investing is a drop in the price of the chosen equities. And a person who pursues a dividend growth strategy may find that a company has reduced its payout due to business problems.

If an investor invests in single stocks, he should not forget to diversify his investment portfolio. To alleviate and mitigate market risks, one should buy shares of companies from different sectors of the economy, countries, different in age, size, and in management strategies.

The main advantage of a more nuanced and differentiated investing strategy is the ability to outperform the broad market and lose less on the market drawdowns. Unlike a manager of an index fund or ETF, a private investor can buy for his portfolio only those companies that he considers to be the best according to his goals.

8. Index funds

An index fund is a type of mutual fund. Index funds are popular because thay are safer than single stock investing: index funds employ passive investing strategies and track a balanced stock index (e.g., S&P 500, DJIA, etc.).

Passive management strategy reduces the commission retained by the management company. This makes index investing cheaper, as they have lower fees than active hedge funds and/or brokers.

The share price of an index fund is calculated once a day and the entry threshold, unlike index ETFs, may exceed $1,000.

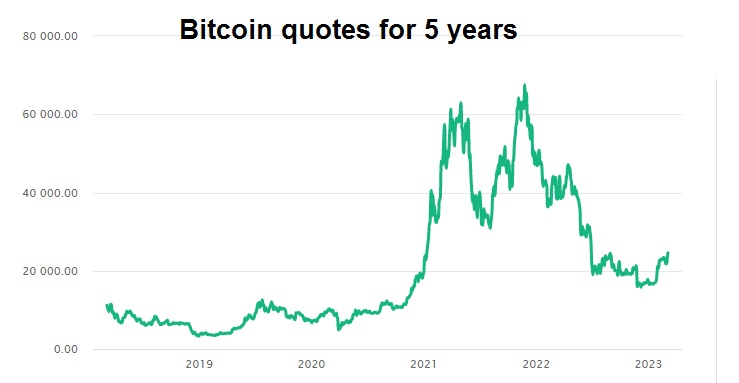

9. Cryptocurrency

Buying cryptocurrency is one of the riskiest types of investments. Investing in crypto is not safe for beginner and intermediate investors.

The main characteristic of cryptocurrency is its high volatility. Although investing in it can bring huge profit, the probability of loss is just as high.

Therefore, it is better for a novice investor to invest in crypto the amount of money that she is not afraid to lose, and to regard crypto markets as a hilarious casino.

Another disadvantage of cryptocurrency is the absence of regular passive income in the form of dividends — all derivative crypto instruments (staking and whatnot) cannot create enough added value to pay back dividends.

You can invest in cryptocurrency not only by buying tokens, but also through shares of cryptocurrency issuers, mining companies and ETFs that invest in crypto businesses or even trade bitcoin futures. Please, always remember: crypto is a high risk asset for most investors.

10. Robo-advisors

A robo-advisor is a computer software run on a digital platform. This type of software is optimizing passive indexing according to your input and financial goals. In order to start getting robo-advisor recommendations, you will need to provide the following data:

- risk tolerance;

- investing objectives and investing horizon;

- available amount of money you can invest.

Most robo-advisors can automate the output of a financial advisor. But due to the fact that no human is involved in the asset selection process, a robo-advisor becomes available to investors with little funds and experience.

The cost of using such programs is lower than that of consulting a financial expert. The minimum investment requirements are also lower. Also, robo-advisor is a great starting point to learn the basics of index investing, to witness how stocks are being selected and portfolio rebalanced.

It is OK to use an advisor provided by a popular online broker. Not only beginner investor but advanced professionals use robo-advisors to automate the boring part of daily research.

Comparison of the best robo-advisors

Below is a table comparing the key conditions for using the most popular robo-advisors.

| Company | Minimum account balance requirements | Service cost |

| Wealthfront | $500 | От 0,25% |

| Betterment | 0 | 0,25% (0,4% for premium users) |

| Interactive Advisors | $100 | 0.08-1.5% for different portfolio tiers |

| M1 Finance | $100 ($500 for retirement accounts) | 0 |

| Personal Capital | $100000 | From 0,49% |

| Merrill Guided Investing | $1000 | 0,85% |

| E*TRADE | $500 | 0,3% |

11. Trust funds

This is another type of mutual fund, similar to retirement saving accounts. In this case, we are talking about collective investments with a predetermined return date for all investors.

Like a retirement accounts, in the early years the trustee of a target-driven mutual fund invests predominantly in high-risk assets. The closer the payback date, the higher the share of bonds and other safer assets.

The advantage for investors is that they only have to make regular contributions. There is no need to manage your trust fund account and no need to understand the stock market.

The disadvantage is that most people won’t be able to match the exact year of return to their retirement date. Trust companies offer target dates in 5-year increments, such as 2045, 2050, etc.

12. Micro-investing apps

A micro-investing app is the best option for financially unstable people. They are also suitable for beginners with very little funds.

Many investment apps allow you to link your credit card and save a few cents each day, rounding up the cost of purchases.

For example, a person pays $11.75 at the supermarket. At the same time, a rounded amount of $12 is deducted from his card account. As a result, $0.25 goes into his micro-investing app account.

Simply by doing everyday chores, going to the groceries, a person accumulates money on her investing account. Healthy habit. For most people, it is much easier than saving a fixed amount of hard cash once a month

Also, many micro-investing apps offer:

- financial education for beginners;

- built-in robot-advisor for asset selection;

- automatic reinvestment in predetermined assets;

- fractional investing (when trading on the stock exchange through a brokerage firm, you can only buy a whole stock).

13. Stock market simulators

This category of computer programs cannot be classified as capital growth tools. But it can help people who are new to investing cope with the fear of losing money.

Such programs allow you to trade stocks and bonds for virtual currency. They track the dynamics of real quotes and show how much money the investor would earn/loss if his transaction were real.

Programs like these help not only get you started in investing. They are used by experienced investors and traders to practice trading ideas.

Investment Strategies

The assets listed above can be included in a portfolio with different strategies. Before you begin investing, you must decide which one is most appropriate for the individual.

Long-term and short-term investing

The time frame in which it is planned to sell the assets and use the accumulated capital is determined by the investment goal of the person.

Short-term investments are capital investments with a term of less than a year. They usually involve low risk assets. High-yield savings accounts, treasury bonds, etc. would be a good option.

By using highly volatile assets, an investor runs the risk of seeing their price drop significantly by the time they plan to exit the investment vehicle.

Speaking of short-term investing, it is impossible not to mention day trading. An investor buys and sells stocks, futures, cryptocurrencies, or other assets in hopes of making a quick profit on price changes. And all trades are closed intraday, in less than 12-hour window.

Day trading is one of the riskiest strategies, very stressful and fun at the same time. According to statistics, less than 10% of traders can consistently show positive results for several years in a row.

Long-term investing typically last three years or more. Long-term strategies can be either passive, for example through mutual funds, or active. In the latter case, an investor selects individual stocks, bonds, cryptocurrencies, etc. on his own. He also regularly spends time to rebalance the investment portfolio.

For long-term investments, it is considered not too risky to use assets with high volatility. In any case, long-terms investing style attracts mentally stable people who do not get easily discouraged by short drawdowns and are able to keep their eyes on a big thing, their ultimate financial goal.

Statistics of the XX and early XXI centuries show that the market is always growing over long periods of time. Therefore, having assembled a well-diversified set of stocks, an investor is almost always guaranteed to make a healthy profit at the end of 20–30 years of investing.

High and low risk investments

Risk in investing is the flip side of profit. The higher the volatility of the chosen asset, the higher its price can rise by the same amount in the same period of time.

But it is just as likely that the value of that asset could fall sharply. This is not a very big problem for someone who starts investing, expecting to use their money in 20–30 years. During that time, the price of a stock or cryptocurrency is very likely to rise.

Even if some of the chosen companies go bankrupt, a properly diversified portfolio will compensate for this loss by increasing the value of other securities.

High-risk investments include:

- cryptocurrency;

- stocks of companies that are in the market expansion cycle (for example, buying McDonald’s is a much less risky investment than investing in Tesla);

- bonds of companies with a high risk of default;

- futures and other money market derivatives;

- binary options, etc.

The best investments for beginners are low-risk assets — certificates of deposit and bonds. This is due to the fact that with a little money, it is more difficult to diversify investments and tolerate losses.

To invest in certificates of deposit, it is best to choose a federally insured bank. The amount of insurance can be as much as $250,000.

Buying treasuries (government bonds issued by the Treasury), it is virtually impossible to lose money. Such securities may fall in value on the exchange, but they will be redeemed on time at face value.

Why you should start investing

Investing is the only way to preserve capital. Money in a bank account loses its purchasing power due to inflation over time.

The only way to outpace it is to make the money “work,” i.e. invest it in bonds, stocks, ETFs, etc. A person with an average income will not be able to save for retirement or to buy real estate simply by funding his or her bank account regularly.

Of course, it’s important not just to buy different assets on an ad hoc basis, but to develop your own style of investing you are comfortable with, to execute your strategy on point and regularly deposit money into a brokerage account.

Investments other than those listed above can also be used to create and preserve capital. For example, buying real estate or starting your own business. But compared to these, there are advantages to investing in securities:

- minimum entry threshold (shares cost starts from a few dollars, penny stocks can get even cheaper);

- low cost maintenance (brokerage fees are minimal, the costs of a real estate agent are more expensive);

- liquidity (you can sell a stock in a few minutes, while real estate or business can take months to sell);

- simplicity (bonds and stocks can be bought online working from home).

Even a small return on a bond or savings account can make a big difference in your financial situation after many years. This is due to reinvestment effect and the power of compound interest. Therefore, beginner investors should not be reluctant to start investing because they don’t have huge money to buy all the hot stocks. It is absolutely fine to take your time and start slow.

Key points to consider for beginner investors

In addition to the timing of investments and types of assets, you need to decide on several other aspects.

Risk tolerance

Many investors have a hard time accepting even a so-called paper loss (a decline in the value of a stock below its purchase price, recorded in a brokerage account). This leads them to sell the asset for fear of further price declines and to make a real loss.

Such people should avoid risky assets and stick to investing only in low-volatility bonds or use instruments that give a guarantee of capital preservation (TIPs, treasuries).

Financial goals

Investing goals are the main thing to consider when planning personal finances.

They should be both short-term (e.g., buying a new car) and long-term (e.g., children’s education or retirement).

Active or passive investing

Passive investing implies that funds are deposited into mutual or index funds, ETFs, or a retirement account.

This investment path looks preferable for beginners because it requires less time to manage capital and reduces trading costs.

Active investing is a constant search for new ideas, studying quotation charts and company reports in the hope of outpacing the growth of indices.

On your own or with a financial advisor

It is equally important to decide whether an investor is going to manage their own portfolios on their own or plans to seek professional advice from financial experts.

One should not turn down professional help in making decisions. Although it comes with additional fees, it can significantly increase profits.

But when you turn to an advisor, there are often minimum deposit requirements that are beyond the means of beginners. In this case, an automated robo-advisor comes to the rescue.

Taxes

Any income is taxable, and there is no way to avoid it. But it is possible to legally optimize taxes through the use of various benefits available to investors.

For example, long-term investors should consider an alternative to a taxable brokerage account in the form of retirement programs or trust funds. It is also possible to reduce the taxes on dividend income, etc.

Conclusion

There are many types of investing goals and strategies that are both simple and profitable for a beginner investor. The main thing is not to stop at one of them. To get the best results, you need proper diversification.

By using a wide range of assets, you can not only reduce risk, but also increase the profitability of your portfolio. Index funds, ETFs, and micro-investing apps make diversification affordable even for people with minimal experience and 500 USD.

Frequent questions

How much money do I need to start investing?

New investors can start trading in the stock market with $100 or even less. For this purpose, it is necessary to choose a broker who is ready to work with retail investors. It is also important to pay attention to broker fees. In some companies, they are unprofitable for people with little funds.

Is $200 enough to start investing?

Yes. If you put $200 into your account every month, taking into account compound interest and reinvestment of income, you can accumulate more than $150,000 over 20 years.

How to invest with little money?

People with little money can use micro-investing apps. They usually have no minimum deposit limit. Micro-investing apps can offer numerous low-value assets, cheap stocks and bonds — the most accessible environment for those who want to get used to investing on a regular basis.