Modern financial industry pays special attention to the portfolio theory of investing. It is based on the division of all existing financial instruments into several groups. Here is a brief overview of what is an asset class, enumerating the main asset classes and explaining their key features. The information provided does not constitute financial advice.

Table of Contents

Key Takeaways

- Assets are grouped into classes based on their similarities. Assets of the same type are considered to have a commensurate degree of risk and their quotes are subject to the same factors.

- Understanding asset classes is a key issue in portfolio investment theory. Appropriate capital allocation between different financial instruments is a prerequisite for accomplishing a goal.

- There is a correlation between different asset classes (the relationship between the way their quotes move). The best way to diversify is to add assets with low or inverse correlation to your portfolio.

Asset Class Definition

An asset class is a group of investment vehicles with similar characteristics. They share common risk factors and show similar reactions to changes in economic conditions. And their trading rules are governed by the same regulations and norms.

Major asset classes:

- cash and cash equivalents (highly liquid short-term debt with low credit risk);

- fixed income assets;

- equity securities;

- collective investment funds;

- alternative assets.

Within one asset class, assets are divided into subcategories. They differ in terms of risk, profitability, liquidity, etc. But the basic parameters are the same. For example, bonds are debt securities. They can be classified according to the issuer’s credit rating, maturity, etc. Stocks are divided into:

- by economic sector;

- market capitalization of the company;

- the type of capital markets the issuer belongs to (developed and emerging markets);

- expected income and growth potential (growth companies and value companies).

Allocation of capital across different asset types helps to reduce investment risks. To build a diversified portfolio, you need to understand the characteristics of each instrument and take into account their correlation. Beginners on the stock market can benefit from the help of a financial advisor or a robot advisor.

In order to better understand what is an asset class, let’s discuss the main ones in detail.

Liquid Financial Assets

Cash and cash equivalents are the most liquid compared to other asset classes. They are characterized by very low risk. They allow the investor to quickly access capital and guarantee its safety. Minimal profitability is a drawback.

The simplest instruments of this asset class are savings certificates, term bank accounts, etc.

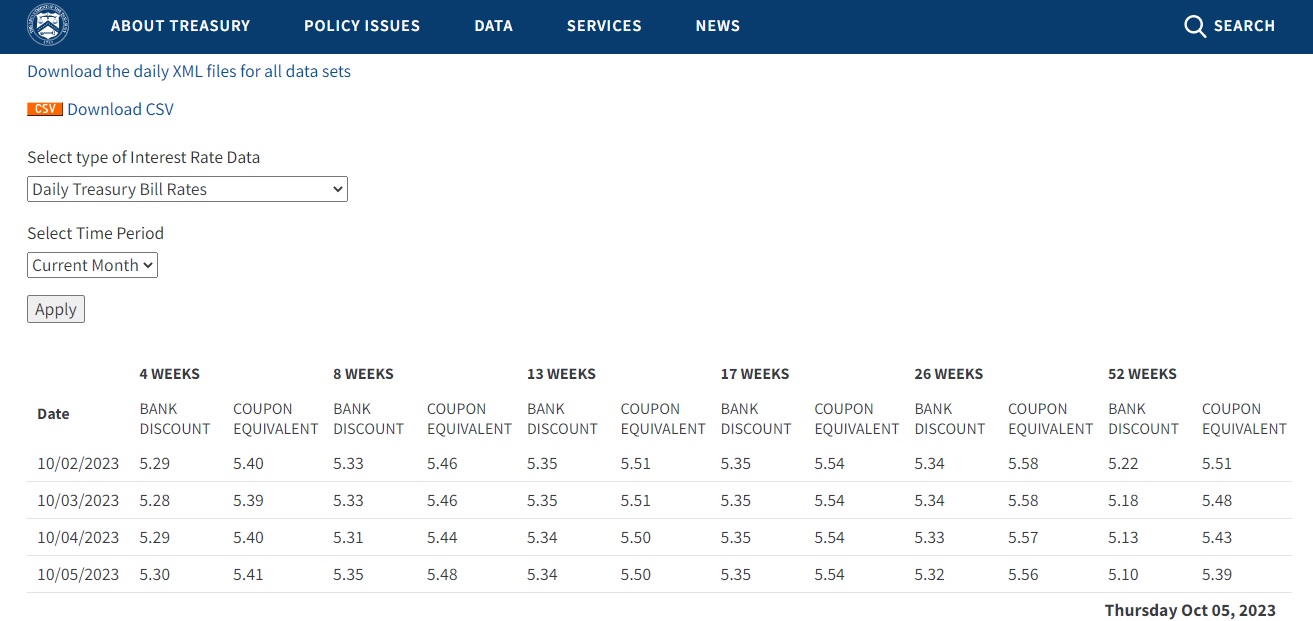

Short-Term Government Securities: Treasury Bills

Treasury bills are government debt obligations with short maturities ( between 4 and 52 weeks). This type of fixed income investment has no interest payments. Therefore, the securities are sold at a discount. On the appointed date, the owner receives an amount equal to the face value (more often $1000).

Treasury bills can fall in value on the secondary market due to rising interest rates. However, the short maturity period allows the investor to wait until maturity and avoid losing money.

Secure Returns with Guaranteed Investment Certificates (GICs)

This is a popular fixed income financial product in Canada. It is very similar to a bank deposit, but it is a type of loan commitment. In this case, it involves lending money to a financial institution.

The investor places capital for a certain period of time at a fixed interest rate. In most cases, GICs assume a longer investment term than deposits in the US. But there are also short-term programmes (from 30 days).

Diversifying with Money Market Instruments

Private investors can make money by opening a money market account or buying stocks in a money market mutual fund. A person earns a profit in the form of interest on the account or when the stock is sold.

Money market funds are proper for investors with an investment horizon of less than a year. Their high liquidity makes it possible to return the money at any time.

Stable Income Generators: Fixed Income Securities

The most popular type of bonds are issues with coupon income. The purpose of the issuer is to obtain financing. The investor earns on regular interest payments, and receives an amount equal to the face value of the bond on the scheduled maturity date. An example is US Treasury bonds issued for 20-30 years.

The risks and yields of bonds depend on the credit quality of the issuer. The latter can be the government, as well as any company. The higher the rating of the borrower, the lower the probability of default and the lower the coupon rate.

Such investments are no longer a guarantee of capital safety. The bond may become cheaper on the secondary market due to the growth of interest rates. This makes the fixed income from the security commensurate with that of new issues.

In times of low interest rates, the price of the bond, on the contrary, may exceed the face value. Having bought it at an increased value, the investor will fail to recover the entire amount invested at maturity.

The Dynamic World of Stocks & Equities

Equity securities are among the most common asset classes. A common stock entitles its holder to:

- to receive part of the profit as dividends (not all the companies distribute it);

- to vote at shareholders’ meetings.

Preferred stock entitles you to dividends only. However, the payments are almost guaranteed. The investor can also receive income when selling the paper at a higher price than it was bought.

The broad US stock market is believed to outpace inflation. With this asset class, you can not only preserve the purchasing power of capital, but also multiply it. But investing in individual companies is a high-risk investment. Dividends and growth of quotations are hardly guaranteed.

The risk level and quotation growth potential depend on the chosen company. A dividend aristocrat is not likely to go bankrupt, but also will not show a multiple growth of quotations.

The market valuation of stocks is influenced by:

- macroeconomics in general;

- the situation in the specific industry the company belongs to;

- corporate events;

- financial performance and other factors.

To reduce risks, at least 5-10 companies from different sectors are added to the investment portfolio.

Diversified Portfolio Builders

The simplest and cheapest diversification option is investing in funds. These are alliances of many investors with total capital allocated according to investment strategies. It may include different asset classes – from government bonds to precious metals and other alternative instruments.

The fund’s risk and return depend on its net assets. The main disadvantage is the management fee and other costs associated with it. They reduce the final return on investment.

The Versatility of Mutual Funds

This is the most popular type of collective investment. A mutual fund participant can earn profits by:

- dividend payments;

- capital gains that the fund distributes;

- an increase in stock value.

There are more than 40 thousand mutual funds in the USA, owing to which it is possible to realize any strategy. They are divided into many types:

- actively and passively managed funds;

- funds working with one asset class ( just stocks, bonds, etc.);

- mixed funds (holding multiple asset classes at the same time).

There are so-called target date funds. These are mixed funds, which at the beginning of their existence invest mainly in risky asset classes (stocks, etc.). As the payback date gets closer, the greater the share of conservative instruments. Thus, such funds save the investor even from rebalancing.

The peculiarity of mutual funds is that management companies calculate the unit price only once at the end of the trading day. Additional commissions may be charged on purchases and sales.

Tracking the Market: Index Funds

These are ETFs and passively managed mutual funds. As the name suggests, the investment strategy boils down to tracking a particular index that reflects the performance of major asset classes. For example, S&P 500, LBMA Gold Price, etc.

More often, the fund manager allocates investors’ capital so that the set of stocks/bonds repeats the basket for calculating the index. But in some cases derivatives market instruments may also be used.

The advantages of a passive fund are that they generally have lower fees than actively managed funds operating with the same underlying assets. One of the main characteristics is tracking error. It shows how much the fund’s performance deviates from the benchmark return.

Real-Time Trading with Exchange-Traded Funds (ETFs)

Exchange traded funds are similar to mutual funds in many ways. The key difference is that their stocks are traded on the secondary market, just like the stocks of individual companies. Due to this, the price changes almost every second, so you can buy/sell at any moment when the stock exchange is open. Liquidity and low spread relative to a fair price is provided by a market maker.

Other major differences:

- ETFs do not distribute capital appreciations, which is more tax efficient.

- More than 99% of ETFs are passively managed funds. Among mutual funds, there are many active strategy options.

- When compared to mutual funds, ETFs offer a fairly limited number of strategies.

When buying and selling ETF stocks, the investor pays a commission to the broker, not the management company.

Exploring Alternative Investments Asset Classes

This asset category includes many types of financial instruments. They can differ greatly in their investment characteristics. What they have in common is that they are non-public company securities.

The main types of alternative asset classes are:

- real estate;

- gold and other precious metals;

- exchange-traded commodities (oil, gas, etc.);

- cryptocurrency;

- private equity;

- investments in hedge funds;

- collectibles, etc.

Instruments from this asset class are often illiquid, inaccessible to a wide range of investors. But the financial industry offers many options to make it easier to work with them. For example, you can trade futures and options on exchange-traded commodities, buy stocks of real estate investment trusts (REITs), etc.

This asset class is considered to require more knowledge than buying bonds or funds that invest in the broad market. The profits an investor makes are highly dependent on the specific instrument. For example:

- Collective investment funds in alternative assets are available to provide dividends. Growth in stock prices is another source of income.

- When trading options and futures, the trader earns on the difference between the strike price of the contract and the actual commodity prices or other underlying asset.

- Investment residential buildings and commercial properties generate rental income. The owner can also sell them and make a profit by increasing the real estate value.

Another issue is the tax ramifications. For example, REIT dividends cannot be recognised as qualifying dividends. And for collectibles, the long-term capital gains tax rate will be 28%. For securities, it ranges from 0-20% (depending on the amount of the investor’s taxable income).

Tips to Acquiring Diverse Investments

Portfolio investment theory is based on the idea that it is possible to pick a ratio of different asset classes that will give:

- maximum return at a given risk level;

- minimum risk at the required level of return.

However, the calculations are quite complicated for a beginner investor. Therefore, there are many model portfolios offering different asset allocations depending on risk tolerance.

It is assumed in an ideal situation that an investor will add asset classes with low or even inverse correlation to their portfolio. But in reality, it is difficult to find such couples.

Several variations of simple portfolios contain the following types of asset classes:

- Conservative. 60% stocks and 40% bonds. Some financial advisors add gold, cash or real estate in varying proportions.

- Moderate. 70-75% stocks, with the rest in bonds, real estate or bank deposits.

- Aggressive. 90% stocks, 10% other asset classes.

Portfolios recommended by various famous investors are also popular. For example, Buffett’s Bequest portfolio – 90% stocks in broad market index ETFs and the rest in bond funds. Other portfolios include Harry Browne’s portfolio, comprising stocks, long-term and short-term bonds, and gold in equal proportions.

There is no universal option that would suit any investor. Everyone should choose a proper strategy based on their investment objectives.

FAQ

What are the major seven asset classes?

The division of investment instruments into 7 asset classes is as follows:

- cash;

- foreign currency;

- bonds;

- stocks;

- real estate;

- commodities (metals, raw materials, agricultural goods, etc.);

- other alternatives (collectibles, etc.).

What are the available asset classes?

The financial industry has made all 7 asset classes listed above available to the private investor. Instruments such as cash, currency, stocks and bonds can be owned directly. Mutual funds and ETFs make investing in property, commodities and other alternatives feasible for people with little capital.

What are the most popular asset classes?

The most common asset classes are stocks and bonds (often in the form of mutual fund holdings). Many people prefer holding cash and cash equivalents.

Which asset class has the best historical returns?

The broad stock market is considered to be the most profitable of all types of asset classes over the horizon of many decades. For example, investing $100 in 1928 in the S&P 500 index could yield more than $727k by the end of 2022 (assuming reinvestment). Such results are presented in a study presented by the Stern School of Business. A similar investment in bonds would have turned into as little as $7,000. A bit more profitable would have been the purchase of gold, which is usually recommended for inflation protection.