In 2022 strategists warned of volatility and major recession ahead, yet 2023 defied most fears and expectations:

- Where forecasts projected modest single-digit gains, major world indices surged 20-30%.

- Yield curves remained inverted as rates doubled from 2021 lows.

- GDP showed crosswinds — manufacturing weakened, but consumers felt confident in taking credit and spending.

- Prices declined unevenly: food and gas and electricity prices dropped significantly, while restaurants-tourism-services part of the economy kept inflation expectations afloat even after the most aggressive rate hike cycle in recent history.

During the last 12 months the US stock market has staged an impressive recovery from the 2022 bear market, erasing heavy losses in just two years rather than the extended declines seen in previous downturns. Powering this sharp rebound has been an astonishing tech rally of the Magnificent Seven, surprisingly solid GDP growth above 2% despite Fed tightening, and increased investor confidence the central bank will soon pivot to rate cuts in 2024 as inflation peaked in the mid-2023.

Table of Contents

Key Highlights of the year:

- Stocks had their best 3 months at the end of the year since late 2020, rising 12.1% in that period. Since hitting their low point in October 2022, stocks have jumped 36% higher.

- Technology companies had a great year, with their stocks rising 59.1%. That was their best year since 2009. Companies like Nvidia and Advanced Micro Devices more than doubled in value.

- Stocks in the communication services sector, like social media and internet companies, rose 54.5% which was the second best performing sector.

- Seven big tech companies contributed 47,8% of the overall stock market gains. Large growth companies, which aim for faster growth, rose much more than value companies.

- Utility stocks, which provide essential services, fell 7% YoY — their worst year since 2008.

- Smaller US companies didn’t do as well as the Magnificent Seven, but they still had their share of decent gains. The Russell 2000, an index of small US companies, returned 17.3%. Most of this return happened in the last two months of the year.

- International stock markets also did well. The MSCI EAFE index, which measures stocks in developed countries outside the US and Canada, returned 18.9%. Emerging markets stocks, as measured by the MSCI Emerging Markets index, returned 10.3%.

- The Bloomberg U.S. Aggregate Bond Index, the main index tracking the boadest variety of U.S. bonds, did well, returning 5.53% for the whole year. High-yield or “junk” bonds, which are riskier, did especially good returning 13.4%.

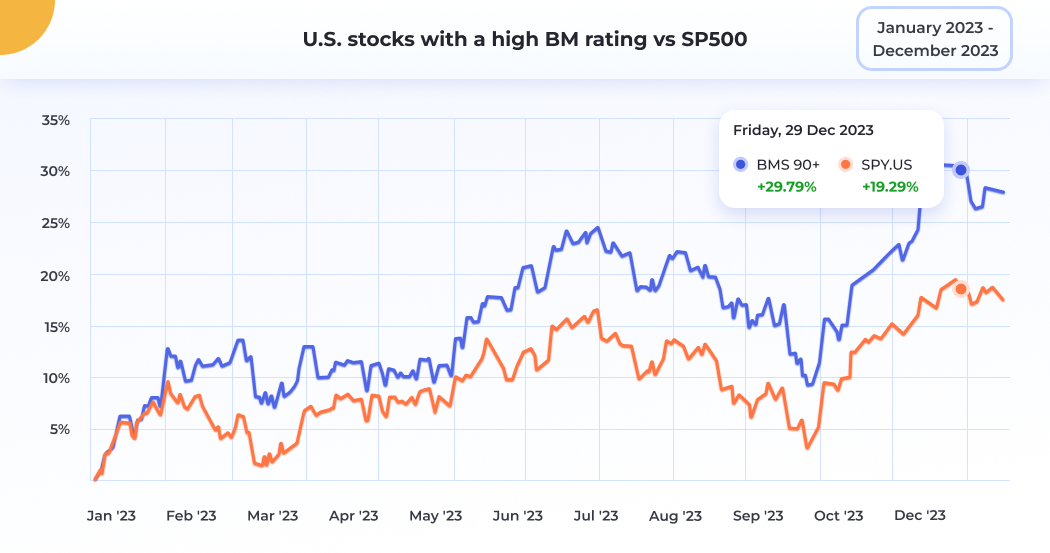

The US stock market did much better in 2023 than experts predicted. Many thought stock returns would be low, but the S&P 500, a popular index of large US companies, had a return of 24.4% for the whole year, nearing the ATH of the early Jan 2022.

At the same time, BeatMarket’s index BMI (top rated stocks BMS 90+) that tracks top performers, returned almost 30% for the whole year:

In two years (since August 2021), the BMI has outperformed the S&P 500 by 21.5%.

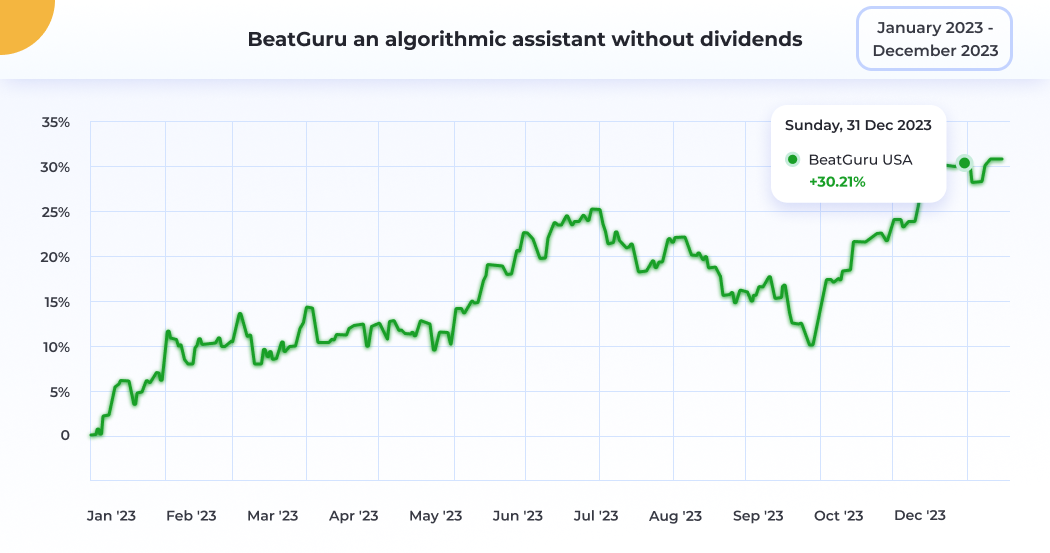

Without dividends the BeatMarket’s assistant tool BeatGuru returned 30% in 2023:

After two years led by inflation concerns, price pressures have eased in most countries. Yet understanding inflation’s path remains elusive — monthly increases contrast slower annual rates. Central banks pause until March, while investors expect multiple rate cuts in 2024.

However, risks still abound that could challenge the sustainability of the bounceback, such as volatile commodity costs, the potential for inflation to take hold again, and inflation expectations remaining unanchored. While investors have welcomed the swift reversion from recent highs, fully easing inflationary pressures back down to the Fed’s 2% target may end up being a lengthier process requiring deft policy steering to avoid overtightening or recession.

Looking Forward with Discipline and Caution

After the most impressive market comeback in 2023, many investors believe a repeat is guaranteed. However, economic tailwinds that aided last year’s recovery may not persist when the effects of the rate hikes will come to fruition.

Though GDP growth is expected to continue, leading indicators point to a softening labor market while consumer and government debt loads rise. The full impact of interest rate hikes also remains ahead: typically, a healthy economy feels higher rates after 9-16 months after the first rate hike.

While a soft landing of the US economy remains possible, downside risks like recession cannot be ruled out as most economic experts remain cautious about the 2024 prospects.

This is what Wall Street is saying about the economy in 2024

JPMorgan: “Although the economy has apparently managed to escape recession this year, we believe the risk of a downturn in ‘24 remains elevated. Fading post-pandemic tailwinds, building monetary headwinds, and dwindling fiscal offsets should all contribute to holding growth below trend, and we project real GDP to expand 0.7% in the coming year (4Q/4Q).“

UBS: “We expect economic growth to slow sharply in the next few quarters, with a mild contraction worth half a percentage point in the middle of the year.“

Morgan Stanley: “High rates for longer cause a persistent drag, more than offsetting the fiscal impulse and bringing growth sustainably below potential from 3Q24. We maintain our view that the Fed will achieve a soft landing, but weakening growth will keep recession fears alive. We forecast that GDP slows from an estimated 2.5% 4Q/4Q (2.4%Y) in 2023 to 1.6% (1.9%) in 2024, and 1.4% (1.4%) in 2025.“

Wells Fargo: “There already are some cracks that are beginning to appear in the economy, and these strains likely will intensify in the coming months as monetary restraint remains in place. Our base case is that real GDP will contract modestly starting in mid-2024.“

Goldman Sachs: “With the more daunting problems largely solved, the conditions for inflation to return to target in place, and the heaviest blows from monetary and fiscal tightening well behind us, we now see only a historically average 15% probability of recession over the next 12 months.“

Societe Generale: “In the US, the long-predicted recession will in our view belatedly materialize in 2024, most likely during the middle quarters of the year, though it stands to be brief and shallow.“

BofA: “We see a soft landing – a period of positive but below-trend growth – as the most likely scenario“

Deutsche Bank: “Our forecast of a mild recession in H1 2024 is thus little changed since our last update in October.“

2024 Outlook — Staying Disciplined Amid Shifting Conditions

In equities, valuations have yet to properly align across the board: Japan and the US tech continue to outperform every peer equity class or sector.

Fixed income remains attractive with corporate balance sheets strong and regular issuance of the UST coming every quarter.

Commodity markets saw headwinds in 2023 but some analysts foresee more volatility and even more gains ahead as energy faces ongoing geopolitical influences on supply and demand tables.

Yields now surpass 5%, so cash reserves could be deployed at favorable entry points throughout the year. Coming off heavy losses in 2022, withdrawals from stock and bond funds surged as “Cash is King” became the mantra. But as markets stabilized and then strengthened throughout 2023, cash underperformed virtually every asset class: cash actually lagged a basic balanced portfolio by a whopping 9% last year. Sitting in money markets longer than 12 months meant watching returns of just 5.1% while stocks, bonds and commodities posted gains closer to 14%.

Activity across venture capital, private equity and M&A slowed considerably last year according to Crunchbase. Deal volumes fell nearly 50% while fundraising, distributions and returns all pulled back amid declining private valuations. However, this pullback has many industry investors refocusing on the basics of profitable growth and driving value through operations rather than relying on the steady supply of cheap credit. With the “growth at any price” mentality replaced, GCs and PE firms are now prioritizing helping portfolio companies achieve positive cash flow and implementing strategic improvements to weather choppy markets.

The old adage remains true — the future is unknowable. While economists provide invaluable context, forecasts should not drive investment decisions: last year’s market comeback served as a beautiful reminder that hard facts on paper (recession in the US) can quickly change into something else on the ground (spectacular tech rally).

Rather than reacting to overly negative or positive outlooks, long-term investors should aim to maintain discipline through diversification and strategic mindset — well-crafted portfolios hedge across global markets, balancing and moderating risks appropriately.

The biggest lesson of 2023: forecasts are educated guesses, not destiny. Successful investors focus on market rhythms and asset rotation waves, on sustainable fundamentals year after year, not chasing instant results or trendy Wall Street narratives or short-sellers alarms.

Overall, 2024 brings prolonged uncertainty surrounding inflation, interest rates and economic growth. In the most likely scenario the long-awaited soft landing will coincide with a moderate growth of the economy. This volatility is expected to impact sectors and assets differently — close monitoring of indicators will be important to effectively adapt strategies to the changing landscape.

Several cyclical sectors appear well-positioned for growth in 2024 based on supportive underlying trends. In industrials, manufacturing infrastructure spending is accelerating after policy changes last year. Leading indicators (hard data, not economic sentiment) such as transportation and manufacturing PMIs point to solid demand, while industry experts anticipate a wave of projects moving from planning to implementation. Information technology and semiconductors also stand to benefit as the AI super cycle develops — multiple tech providers and data operators still need more chips. While supply and demand are nearing balance, digital adoption trends ensuring ongoing need for semiconductors across multiple end markets.

Healthcare similarly seems primed for continued expansion. New drug approval activity rebounded in 2023 and industry pipelines remain robust, suggesting ongoing innovation in therapeutics. The huge succes of Ozempic is telling investors that demand drivers like aging populations and increased access in emerging nations furnish a favorable backdrop for chronic illnesses treatment protocols. Private sector interest is rising as well, with large-cap pharmaceutical and device companies actively pursuing M&A and partnerships within adjacent spaces like biotech and medtech. Taken together, these fundamentals supporting industrials, semiconductors and healthcare increase confidence in the growth potential for these sectors through 2024 and warrant closer monitoring by equity investors. Revenue and earnings visibility has improved, representing opportunities for both index investors and active stock pickers.

Disclosures

All opinions expressed above are solely the opinions of BeatMarket Oy and do not reflect the opinions of any other sources. This report contains data from third party sources: although BeatMarket Oy believes these sources to be reliable it makes no representations as to their accuracy or completeness. The information contained herein is based upon certain assumptions, theories and principles that do not completely or accurately reflect your specific circumstances. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security.

This report is for information purposes only and does not constitute a complete description of our services or performance. The information contained in this document is not a solicitation to sell securities or investment advisory services where such an offer would not be legal. Past performance is never a guarantee of future performance. The information discussed is intended to serve as a basis for further discussion with your financial, legal, tax and/or accounting advisors. It is not a substitute for competent advice from these advisors. BeatMarket Oy are not authorized to practice law or provide legal, tax or accounting advice. If a numerical analysis is shown, the results are neither guarantees nor projections, and actual results may differ significantly. Any assumptions as to interest rates, rates of return, inflation, or other values are hypothetical and for illustrative purposes only.

You Might Also Like

- What Is a Dividend Recap? Understanding This Financial Strategy

- Best MLP ETF: Understanding Dividend Stocks and How to Invest in Them

- What Is a Dividend Yield? Understanding This Key Investment Metric