The default risk premium serves as a reward for risk tolerance. It is a return that compensates for the threat of capital loss. This concept is one of the key aspects of the debt market. It is applied to corporate bonds.

No premium makes no sense to invest in securities that are likely to default. Bidders always choose the least risky security with equal yield. When an unreliable issuer does not pay higher interest rates, it will not attract capital.

The default premium depends on the credit rating. That is, directly on the risk level. Economic conditions and risk-free rates of return are also important factors.

Table of Contents

Definition of Default Risk Premium

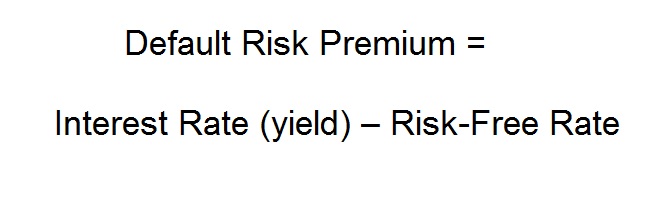

The default risk premium is a compensation to investors. It is paid to investors for choosing risky securities instead of risk-free instruments. The latter are typically Treasury bonds.

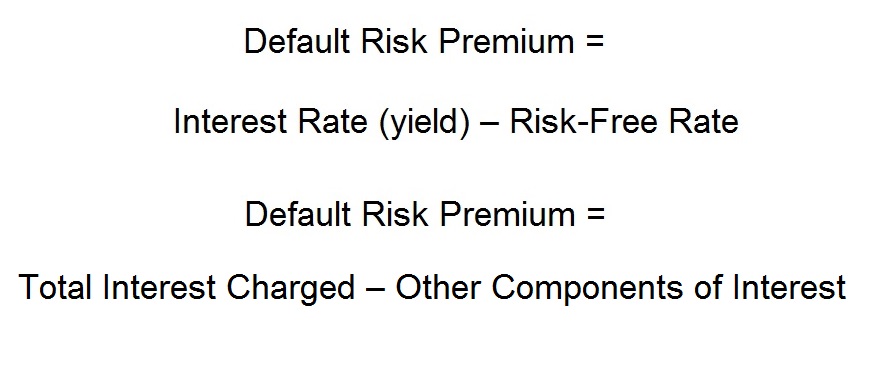

The Institute of Corporate Finance defines it as the difference between the available interest rate and the risk-free rate.

The formula is used to calculate the amount of premium a security will bring.

The higher the issuer’s credit risk, the higher the chance of an implied default. As a result, the reward for investing in its securities increases. When a company issues bonds, it must take into account the rate of return required by the market. The interest rate must be offered to attract investors.

Explanation of Default Risk Premium

There is a concept called risk-free rate. This is the pay back earned on securities with a minimal default risk.

When an investor deposits money in corporate bonds, they agree to assume the default risk of the issuer. The company may experience difficulties with debt servicing and interest payments.

At best, the company will make the required payments later than the due date. At worst, it will fail to remit principal and interest at all.

The default risk premium (DRP) serves as a lender’s incentive. Higher yields encourage investment in corporate securities. Otherwise, it would make sense to choose government bonds. The opportunity for potentially higher returns offsets the threat that the borrower will default.

Purpose of the Default Risk Premium

The higher the chances of a borrower’s default, the higher interest rates the borrower must set on these bonds. Otherwise, the latter may become unclaimed by the market.

Higher interest rates in this case act as investor incentives. When the DRP fails to meet the lenders’ assumptions, they will not buy the security.

Therefore, rewarding the possibility of default solves the problems of both parties. The lender or investor gets a return that exceeds the risk-free interest rate. The company gets the opportunity to borrow money.

The value of the DRP depends on many factors. Reliability is the key one. It is determined by the creditworthiness when it comes to a bond issuer. This parameter is assigned to large companies by rating agencies. For example, Moody’s.

For individuals, the rate will depend on their credit records. When a person has previously made late payments, they are considered an unreliable payer. The bank will only give them a loan at a higher interest rate.

It follows that it is advantageous for a company to have a high credit rating. The higher it is, the lower the DRP the potential investors will want to receive. This widens the circle of people who will be interested in buying securities.

Due to the higher creditworthiness, the cost of borrowing is reduced. The bonds will also be attractive if the issuer’s interest rate is charged at a lower rate. This reduces the company’s capital costs and has a positive effect on its financial performance.

The same is true for a private individual. A good credit history increases the probability of loan approval. It also gives a chance for a lower interest rate.

Default Risk Premium Formula

An unreliable borrower must pay a higher interest rate. The following formulas can be used to calculate the interest rate for a particular bond.

The exact figure that the market expects is much more difficult to find. In general, the following components determine the interest rate:

- risk-free rate;

- reward for the issuer’s poor credit rating;

- liquidity premium;

- maturity premium;

- expected inflation premium.

The higher the liquidity premium, the lower the trading volume of the company’s bonds. It is likely that the owner will not be able to sell the asset quickly at market value. Besides, such a security has higher volatility. The additional amount of the annual percentage yield offsets this risk.

The maturity premium depends on the bond’s maturity. The shorter it is, the lower the chances of the issuer’s default risk and any other negative scenarios.

Nasdaq expert recommendations suggest that this premium should be determined using treasuries.The interest rate of an annual Treasury bill and the yield of ten-year bonds may differ.

The inflation premium does not depend on the issuer’s quality. It reflects the market’s expectations about the inflation rate. Its objective is to make investments favorable to preserve capital from depreciation.

What is important is to answer the question of what is considered the risk-free rate. This is typically taken as the yield on ten-year Treasury bonds.

The DRP considered acceptable by the market fluctuates over time. It falls when demand for so-called junk bonds increases. This happens when the yield on low-risk instruments is minimal. Another reason for the increased interest in such assets is the high estimated rate of inflation. In the contrary circumstances, the reward for a potential default claimed by investors grows.

How to Calculate the Default Risk Premium

The following steps must be carried out to calculate the bond’s default risk premium:

- find out the rate of return on risk-free assets;

- calculate the liquidity premium;

- calculate the maturity premium and inflation rate;

- subtract the values obtained in the previous steps from the interest rate offered by the issuer.

A liquidity premium is calculated when the security is illiquid. Corporate bonds issued by major companies are typically highly liquid. They can be sold within a day with a minimum spread, just like treasuries.

The yield on ten-year government bonds is often taken as the risk-free rate. When different maturity assets are discussed, another benchmark can be chosen. Such as, for example, one-year Treasury bills for short-term investments. Or government securities with a 30-year maturity for a long time horizon.

Such an approach would simplify the calculations. No allowance will be required for longer maturity and inflation.

An online calculator can be used to calculate the DRP.

Example of Default Risk Premium Calculation

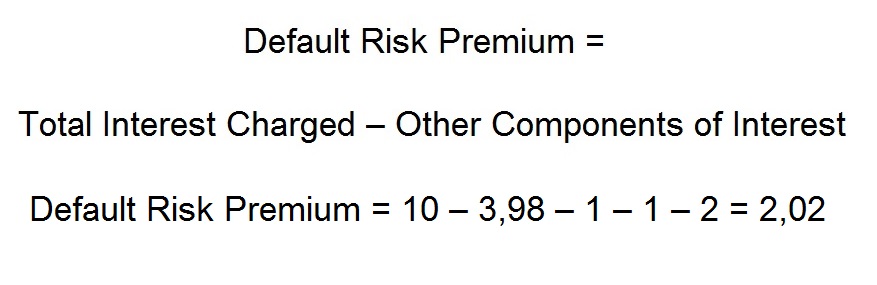

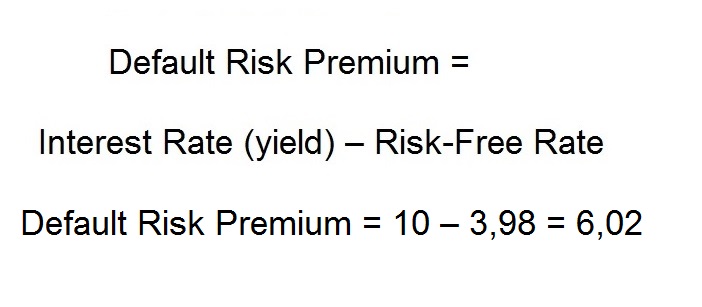

The current yield on ten-year treasuries is 3.98%, as provided by investing.com.

Here is a calculation of the DRP for bond No.1, taking into account the following input data:

- annual percentage yield of the chosen bond – 10%;

- risk-free rate – 3.98%;

- liquidity premium – 1%;

- maturity premium – 1%;

- inflation risk premium – 2%.

Using the second formula for calculating the DRP, the following is obtained:

The issuer’s credit risk premium is 2.02%.

Now consider security No.2 with the parameters close to ten-year treasuries. Here the liquidity premium, etc. can be neglected. It is a rather simple calculation of the DRP. The first formula is used. The return for risk-free investments is subtracted from the annual rate of return on the bond.

Factors Determining Default Risk Premium

The DRP value that the market considers acceptable depends on the following factors:

- credit history;

- credit worthiness;

- company profitability.

When a company has made late interest payments, it is considered unreliable. The requirements for the default risk premium will be significantly higher.

Current creditworthiness is determined by a rating agency. Financial and non-financial indicators of the issuer are taken into account.

The company’s revenues are also important. They should significantly exceed the cost of loan servicing. Such an issuer is more reliable. When profits barely cover required debt payments, there is a high threat of defaults.

Lower default risk of the company increases the liquidity of its bonds. This rule is valid, all other things being equal.

Interpreting the Default Risk Premium

The DRP is not just an abstract figure. It reflects the market’s faith in the issuer’s solvency. It also affects the company’s equity capital implicitly. It should be taken into account by equity investors.

When financial difficulties arise, the issuer is more likely to default. Meanwhile, the borrowing cost for the company increases. It can still refinance existing debts and raise new funds. But only at higher interest rates than before. This means higher interest payments and lower profitability.

In such a situation, both bonds and stocks fall in value. This moment can be considered a good point to enter a position. When the business overcomes difficulties, the investor will get profit. It will be provided by higher bond yields and stock prices growth.

But there is still a chance of default. A person can lose the invested capital. Below is the chart of Loyalty Ventures quotes. In March 2023, it went into default. As a result, management filed for Chapter 11 protection.

It is crucial to determine the risk-return tradeoff on your own. And do not invest in securities bearing a risk higher than the specified one.

When planning a financial strategy, it is worth considering factors other than the reliability of the issuer:

- maturity of the bond;

- the chance of a loss after inflation adjustment;

- the chance of the risk-free rate increasing, etc.

For a variety of reasons, interest rates on risk-free assets may rise. As a result, the cost of borrowing for all issuers increases. This creates a higher default risk for a company that has struggled to service its debts.

Relevance of the Default Risk Premium (181 words)

Moody’s gives a disappointing forecast by March 2024: “The default rate on junk bonds could approach 4.9%.” Therefore, a proper assessment of an issuer’s risk rating comes to the fore.

Bonds with a high DRP allow for the required investor returns. At the same time, there is an opportunity to stay within a moderately aggressive strategy. Junk bonds have a higher risk of default. But debt instruments are still considered safer than stocks of issuers of the same level.

The DRP is not only an investor’s compensation for additional risks. It is also an instrument that:

- helps to make the right financial decision;

- clearly reflects the situation on the credit market;

- serves as an indicator of deteriorating economic conditions;

- influences monetary policy.

It is essential to calculate the DRP and compare the performance of different companies. This gives the investor a clearer picture.

An increase in the DRP relative to the historical average indicates economic instability. This indicator is a factor that the Federal Reserve takes into account when making a rate decision.

Frequently Asked Questions (FAQs) (405 words)

H3: Who pays the default risk premium?

The DRP is paid by the issuer of the bond. Companies offering low credit ratings must offer higher interest rates. This is the only way to attract lenders. If additional yield is not provided, an investor will not invest money in assets with higher risk. As a result, securities will not be in demand at initial public offering. The same applies to bank loans. They are issued to unreliable payers at a higher rate.

What is the default risk premium quizlet?

Quizlet is a website that helps to prepare for exams on various topics. Among other things, assignments from financial quizzes concerning investing in debt securities can be found. It is useful to take them before buying bonds.

What is the impact of the default risk premium on interest rates?

The DRP increases the interest rate that the issuer must set on newly issued bonds. When a company’s credit rating has fallen, its debt securities on the secondary market will become cheaper. As a result, these assets’ buyers will receive a higher yield.

Can default risk premium be negative?

There is no concept of negative risk premium for the issuer’s insolvency risk. Government bond yields are taken as the risk-free rate. There is no more reliable payer.

Why does the extra charge for default risk change sometimes?

The reward for possible default may vary from period to period. It depends not only on the quality of the borrower. It is influenced by market conditions. It normally increases when economic difficulties are expected, when the Federal Reserve rate is expected to rise, etc. So when the risk-free yield falls, the risk reward falls as well.

Conclusion

Fitch Ratings says: “In 2024, the DRP may exceed 5 per cent. From 2025, it will gradually begin to decline.”

The current year is a great period to lock in higher yields. But while every company strives to honor its debt obligations, defaults are inevitable.

With any form of lending, one should study the disclosure statement thoroughly. No less important is to learn as much as possible about the issuer when an investor buys junk bonds. This is one of the most unreliable types of debt securities. It is advisable to consult with financial advisors. At the very least, it is necessary to study all the information available, including the white papers.

Join BeatMarket and get instant access to a selection of promising assets. Find out which securities offer above-market returns with no additional risk. Register for free and take advantage of all the service’s features.

You Might Also Like

- How to Calculate Dividend Payout: A Simple Guide

- Top Undervalued Dividend Stocks to Buy in 2025

- Dividend Deposit Explained: How It Works & Why It Matters

- Is Dividend Reinvestment Taxable? Understanding the Rules