Both certificates of deposit (CDs) and bonds are relatively low risk investments that can generate fixed income. Fears of recession have caused interest in them to surge.

The article takes a closer look at what these assets are, answering the question of whether they can be considered completely risk-free investments. It will also compare CDs vs bonds. This will help to choose a more proper financial instrument for everyone.

Table of Contents

Bond vs CD: How to Compare? на What Is the Difference Between CDs and Bonds?

A CD is a type of bank savings account. Credit unions offer a similar financial instrument, but the instrument is called a stock certificate. However, the functions and features are identical to a CD. The only difference is the type of institution the contract is signed with.

The advantage of a CD compared to a traditional savings account is a higher yield. In most cases, the bank pays higher interest rate as a reward for not disposing of your money till the contract expires.

The main characteristics of CDs that should be compared when choosing one:

- Expiration Period. Typically, a bank or credit union offers programmes with terms from three months to five years. Although, shorter/longer options can be found.

- Minimum deposit. It is often set at $1. But some banks require a deposit of $1,000 or even $5,000. Deposit cannot be replenished during the term of its validity.

- Interest rates. CDs typically have a fixed interest rate. In 2023, offers with an APY of 4.8% and higher can be found. This is more favorable than typical savings accounts.

- Early withdrawal penalties. The contract specifies how much of the initial deposit or/and interest the customer will lose if the contract is terminated.

CDs and stock certificates, just like traditional savings accounts, are considered a risk-free investment. They are insured by the Federal Deposit Insurance Corporation or the National Credit Union Administration for $250,000 per person.

An investor’s income coming from a CD account is the interest the bank pays for depositing the money. Under the terms of the contract, they are usually added to the body of the deposit once a month. The investor receives them together with their capital when the contract expires.

Types of CDs

Traditional CDs offering the features described above are the most widely used. However, some banks offer modified versions.

The most popular types of CDs are:

- No-penalty. Such CDs do not incur a penalty for early withdrawal. But the yield on them is lower.

- Add-on. These types of CDs can be topped up during the term of their validity.

- Bump-up. These CDs have no fixed rate. Their yield increases as the Federal Reserve rate increases. In fact, the investor never knows the final return in advance.

- Step-up. The interest rate also changes, but on a predetermined schedule.

What are bonds and how do they work?

Bonds are debt obligations of the issuer (government or corporate). The money raised is used to finance operations.

Bond’s issuers pay back the loans on a specified date, i.e. extinguish the bonds. The bondholders receive an amount equal to the face value. When bonds are traded on the stock exchange, an investor can sell them at any time without waiting for the maturity date. In doing so, the interest earned while holding the security will be retained. But there is a risk of losing part of the money invested when selling due to falling bond market prices.

The main parameters of bonds to be considered when choosing an asset:

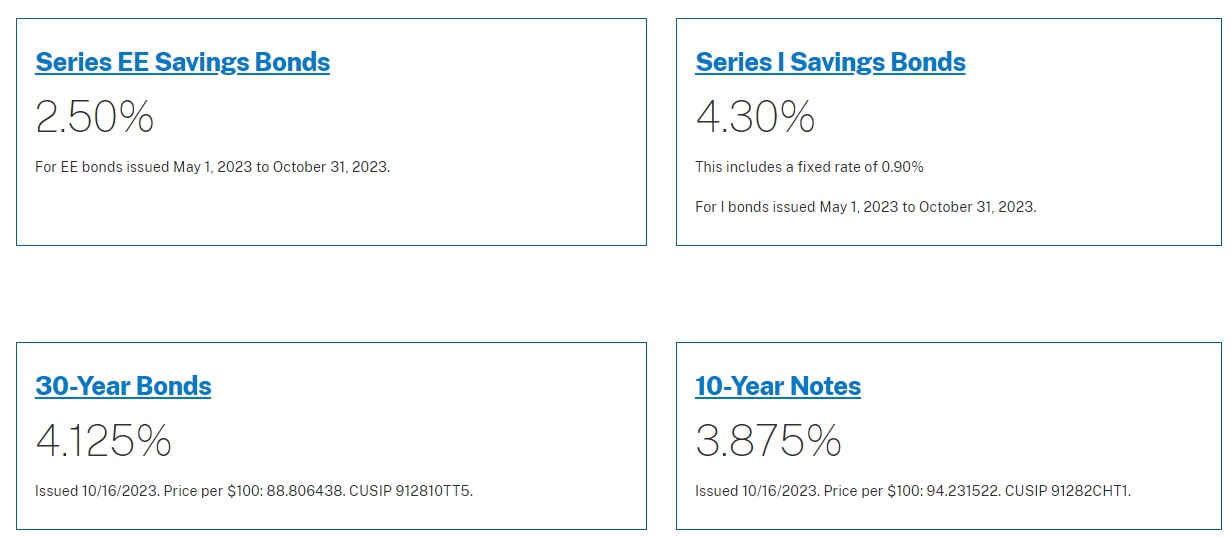

- Bond maturities. Bonds may be issued for a period of up to 30 years.

- Minimum investment. This parameter depends on the type of bond. For example, government securities Series I can be bought for a multiple of $25. The most common face value of corporate bonds is $1000, municipal bonds can offer $5000.

- Coupon rate. In most issues this parameter is constant. But the income may vary, for example, depending on the inflation rate.

The investor’s profit from owning a coupon bond consists of 2 components. The first one is coupon income. Most issues provide interest payment twice a year. This money can be both reinvested and spent.

The second source of income is a positive difference between the purchase and sale/redemption prices of bonds. Their market value increases when the Fed Funds rate goes down. On the contrary, when interest rates rise, older issues become cheaper. Redemption is always at par, even when the investor bought an individual bond at a higher price.

However, not all bonds pay a fixed income stream. For instance, the terms of investment in Series I and EE government securities should be capitalized – interest is added to the initial deposit. While some types of debt are non-couponable, like Treasury bills.

Investment risks depend directly on the issuer’s credit rating. In case of default, the investor is likely to lose the money. Treasury securities are considered the most reliable ones. Corporate and municipal bonds are inferior to them.

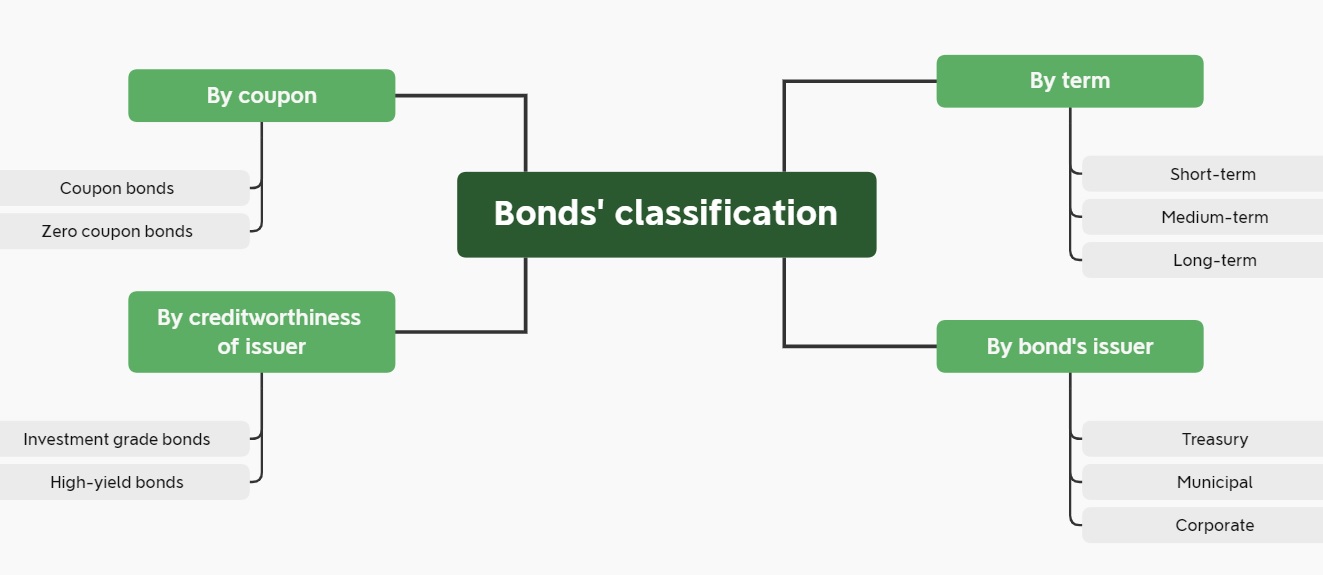

Types of bonds

There are many ways to categorize debt securities. The most popular one is by bond issuer. This parameter is used to distinguish between:

- Treasury. They are issued on behalf of the federal government, so they have the highest credit rating.

- Municipal. The emitters are cities, counties, etc. They are used to finance publicly significant projects. Coupons of most such securities are not subject to federal income tax.

- Corporate. They are issued by large companies with high credit ratings. Yields are usually slightly higher than that for the first two types. But the risk is considered low. Such issues are referred to as investment grade bonds.

- High-yield bonds. These are debt obligations of issuers with low credit rating. There is a high probability of default on them. But the coupon rate is noticeably higher.

Treasury bonds are divided into several types. For short-term investments ( from several days to a year), promissory notes are proper. For medium-term (up to 10 years) – treasury notes. For long-term (up to 30 years) investments, Series I and EE savings bonds, as well as treasuries with a maturity of 20 or 30 years, are suitable.

How to invest in bonds

There are 3 ways of investing in bonds:

- invest money directly through TreasuryDirect.gov (government securities only);

- buy bonds on the secondary market of securities (stock market) through a broker;

- participate in bond mutual funds (or buy stocks in a similar ETF).

There are several CD strategies that are used to protect against interest rate risks. For example, split the money into several accounts with different contractual maturities. A similar approach can be used in bonds. Investments are diversified not only by issuer but also by maturity.

What is better: a CD or bonds?

The answer to this question depends on the investment strategy. To make it easier for readers to choose, let’s compare CDs and bonds by their main features in the table below.

| Parameter/Asset Type | Traditional CD | Bonds |

| Interest rates | Fixed | Fixed (with few exceptions) |

| Total income | Equal to interest income | May be higher than the interest income due to an increase in the value of the bond |

| Risks of loss of fixed capital | Low (only upon early termination of the contract) | Low (when held to maturity).Medium (at early sale) |

| Validity period | Up to 5 years | Up to 30 years |

| Minimum deposit | From $1 | From $25 for direct investments From $1 for investments in mutual bond funds |

| Replenishment option | No | Yes (through purchasing additional securities) |

| Withdrawal option | No | Yes (due to sale of bonds on the stock exchange) |

| Who offers the asset | Bank, credit union | Federal and municipal government, large companies |

| Bankruptcy insurance | Yes | No |

As the table shows, bonds are a potentially more profitable financial instrument. They are characterized by greater liquidity and flexibility. However, investing in them involves higher risks than opening a CD.

Bond vs CD: How to Compare?

Before comparing CDs and bonds, an investor should consider the following:

- investment horizon;

- risk tolerance;

- desired return.

CDs are preferable for risk averse people. It is also proper for short-term investments, e.g. for saving for a holiday or a down payment. The main advantages of this financial instrument are predictable profitability and flexibility in terms of investment duration.

Traditional CDs are illiquid. Therefore, only the money the investor can certainly do without should be placed on such type of savings accounts. This is the main disadvantage. But there are a small number of programmes, upon which banks do not withhold early withdrawal penalties.

In addition, this disadvantage can become an advantage and help people with low financial discipline to achieve their investment goals.

When bonds are a better choice

Bonds are preferred when an investor is looking for:

- higher yields than those offered by banks;

- options for long-term investments (more than 5 years);

- fixed income sources for passive earnings.

Unlike CDs, bonds are not insured in case of the issuer’s bankruptcy. Therefore, investments in corporate issues are considered more risky. But securities of large companies and the US government are considered conservative investments on a par with bank accounts.

In order to diversify the investment portfolio, bonds are used as a stable element that reduces the volatility of the total value.

This type of securities gives you flexibility in terms of investment timeframes. There are issues that will be repaid in just a few months. They are proper for short-term “parking” of free capital in anticipation of a new investment idea.

But the main advantage of this asset is liquidity. Bonds issued by the government and large corporations can be sold on the exchange within a few minutes. And the spread between bids to buy and sell is minimal.

Thanks to the accumulated coupon income, the investor retains interest for each day of real ownership of the asset. When comparing CDs and bonds, this is an important argument in favor of the latter.

Factors to consider in current environment

When an investor chooses an investment horizon and asset type, expectations about the Fed’s interest rate behavior need to be taken into account. The current period (2023) is characterized by rising rates. There are reasons to believe that the cycle of their growth is not over yet.

In such a situation, short-term CDs and bonds with close maturity, such as treasury bills, may be preferable.

When the Fed Funds rate rises, bond prices fall. Thus, at its next increase there will be an opportunity to buy them at an even more favorable price. When a person hurries to do so, there is a risk of losing part of the principal investment in the subsequent sale.

On the other hand, most risk averse investors are already actively building their positions up in long-term bonds. Current interest rates have raised yields on debt securities to their highest levels since 2007. For many, locking in now is preferable to looking for a better investment entry point.

When the economic outlook changes and the market waits for interest rates to fall, long-term bonds will become even more attractive.

Firstly, they provide an opportunity to lock in high yields for years. Secondly, when the cost of borrowing falls, the market price of old issues will start to rise. As a result, the investor will be able to sell them at a higher price and the profit will be higher than it was expected.

How to buy CDs and bonds

It takes a few minutes to invest in CDs and bonds online.

To open a CD account or stock certificate, it is necessary to:

- compare bank and credit union offers in terms of APY, minimum deposit, and deposit terms;

- contact the organization chosen (your personal information, such as national insurance number, address, etc. are required);

- apply for a contract under the programme you prefer;

- transfer capital from your main account to a CD account.

A CD can be opened offline as well. To do this, visit an office in person. But online banks offer more favorable rates in 2023.

The method of buying bonds depends on the type of these securities chosen:

- To invest in Treasury bonds, all you need to do is create an account on TreasuryDirect.gov and apply to buy the desired number of securities for the amount available.

- To get a well diversified investment portfolio from bonds, you need to invest in them through mutual funds. This will require you to contact a management company. In 2023, this can also be done online by registering on the company’s website.

- To invest in individual corporate bonds or exchange-traded bond funds, you need to open an investment account directly through a broker. You should choose one by comparing tariffs and commissions.

Once a person opens an account with a broker/management company and funds the account, they can buy bonds or stocks of bond funds with a few clicks.

Other savings options

In addition to CD’s and bonds, there are 2 other types of fixed income investments for short-term investments. These are money market accounts and high yield savings accounts.

A few facts about these savings options:

- the owner can use their money at any time with no early withdrawal penalty or loss of interest accrued;

- current yields are comparable to corporate bond yields (APY up to 5%), while standard savings accounts can yield less than 1%;

- minimum deposit depends on the bank’s policy and can be as low as $1 or as high as thousands of dollars.

The key difference between CDs and bonds is the accessibility of the funds deposited. A money market account can be linked to a card and money can be spent directly from the account.

A high-yield savings account usually has no such option. To manage one’s capital, an investor must first transfer money to a checking account (e.g., through online banking). Most banks and credit unions allow you to do this with no commission, but no more than 6 times a month.

The main disadvantage of money market accounts and high-yield savings accounts is the floating rate of return. The bank can lower it at any time. For CDs and fixed-income bonds, it is not possible.

FAQs

Is it better to invest in CDs or Treasuries?

The answer to this question depends on the investor’s needs. When looking for a long-term asset or potentially higher returns, bonds are the preferred option. Also, most bond issues pay interest, bringing their holders a steady income. To create a well-diversified portfolio, it is advisable to use bonds, CDs and other financial instruments.

Are CDs safer than stocks and bonds?

CDs are safer than stocks. Banks guarantee the safety of the funds invested, provided that the investor waits until the contract expires. Also, CDs are safer than corporate debt securities. However, government bonds are loans that are considered to be low risk investments, just like CDs (when one plans to wait until maturity).

Are CDs and bonds taxed differently?

Interest earned on CD is subject to state and local taxes as ordinary income. No exemptions are provided. On Treasury bonds, the investor pays federal tax, but they are usually exempt from state tax. In contrast, for municipal bonds, no federal income tax is withheld on most issues.

You Might Also Like

- Understanding Qualified Dividends: Tax Benefits & Criteria

- How Forward Dividend & Yield Works in Investing

- The Complete Dividend Aristocrats List for Reliable Returns

- Dividend vs APY: How to Calculate Your Actual Earnings