The possibility of spreading some costs over a period of several years is one of the most important accounting concepts. Amortization and depreciation were introduced to make this possible. This topic is quite confusing, but extremely important for business owners and start-up investors.

Asset impairment assessment is not just a financial concept. The concept is used, among other things, to reduce the taxes a company pays. Therefore, it is essential to understand when an asset should be paid off or when to charge depreciation.

Table of Contents

What is Amortization?

It is the allocation of the cost of intangible assets over their entire period of use. It is usually done on a straight-line method: the value of the object is divided by the number of years during which it will be used by the company.

Each year the asset is used, its value is paid back by the same amount. By the end of the assigned “object’s” useful life, its book value is 0.

These are examples of intangible assets to which amortization can be applied:

- copyrights, patents;

- trademark;

- franchise agreement;

- issue of bonds (expenses related to their placement).

As an example, a patent has been acquired by a company which plans to manufacture products for 10 years. Its price is $1 million. Using the straight-line method, the annual amortization expense would be $100,000.

The term amortization can also be used in another sense. It is used when talking about loan repayment. Here, the term “amortization schedule” means a payment schedule, each including part of the debt and interest accrued.

What is Depreciation?

When it comes to fixed assets, i.e. tangible assets of an enterprise, the concept of depreciation is applied. The costs of acquiring an object are allocated to the period of its useful life, just as in the case of depreciation. But there are several issues that change the calculation scheme.

In the case of intangible assets, amortization is more of an accounting concept. It is also important from the point of view of taxation. Among other issues, depreciation reflects the actual obsolescence and breakdown of fixed assets. Therefore, it can be calculated either on an accelerated method.

Here are examples of tangible assets to which the concept of depreciation is applicable:

- buildings;

- transport vehicles;

- machinery equipment (machine tools, etc.).

An important issue is that tangible items most often have a real value at the end of the asset’s useful life. For instance, a building can be sold and equipment can be recycled.

Therefore, the book value of such items cannot be reduced to zero. It is assumed to be equal to the salvage or resale value.

How to Calculate Depreciation

The 3 input parameters are important to determine devaluation:

- The price of an asset is the company’s cost of acquiring it.

- Useful life – the period of time over which the object will generate profit for the company. However, other factors, such as the quantity of production, may be taken into account in the calculations instead of the time indicator.

- Salvage value (resale price) – the amount that the company is expected to receive from the object once its use is completed.

The parameters listed above are required regardless of which method of calculating depreciation is applied.

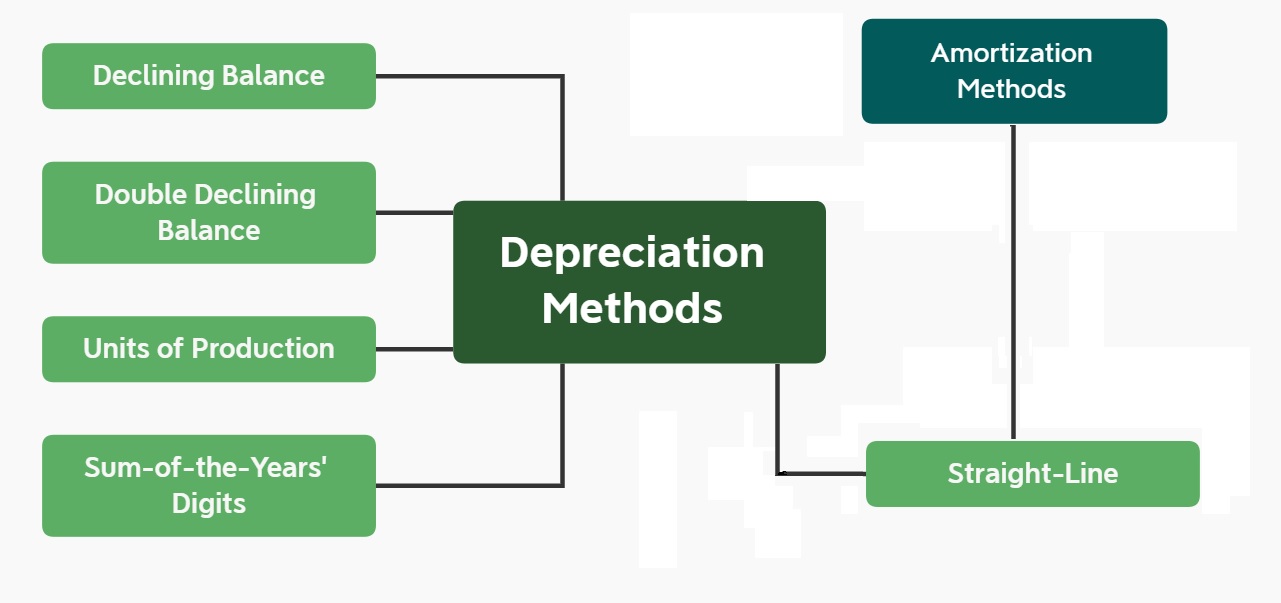

Depreciation Methods

Typically, a company has the option to choose which of the several allowable methods to use to count devaluation. The most common approaches are as follows.

Straight-line method

The method is proper for items that lose their value evenly. Throughout the period of fixed assets use, the value shown in the balance gradually decreases. Each year it is reduced by the same amount.

Declining balance

The declining balance is an accelerated depreciation method. It can be used for items that become obsolete quickly. Such as computers, cars, etc.

The idea is that a certain coefficient is established, which remains unchanged for the entire useful life of the object. A new amount of depreciation is counted each year with the help of this coefficient. It is deducted from the current residual value.

For example, the original price is $10k and the depreciation factor is assumed to be 0.1. If so, then:

- In the first year, the carrying value of the property will be reduced by $1000 ($10000 * 0.1) to $9000.

- In the second year – by $900 ($9000 * 0.1) and will be $8100;

- In the third – by $810 to $7290, etc.

That is, the older an object is, the slower its price decreases.

Double declining balance

Double declining balance is another option for accelerated depreciation. It is also proper for objects that are rapidly becoming obsolete.

The essence of the method is that in the first few years the book value is reduced by double the rate the straight-line method would use.

Sum of years digits

Calculation based on the sum of years digits also accelerates depreciation. It is done as follows:

- The useful life of the asset (N) is determined.

- All digits from 1 to the set value are added up. 1+2+3+…+N = M.

- The percentage of total depreciation to be written off in the first year is counted using the formula 100*N/M.

- The amount of depreciation for the second year is calculated by the formula 100*(N-1)/M.

- The counting is repeated for the following years, gradually approaching 1.

Units of production

This approach takes into account production units rather than years. Let’s say, for example, that a company buys a machine and plans to use it to produce 1 million parts.

To determine how much depreciation should be recognised in the current year, proceed as follows:

- Count the percentage of depreciation per part.

- Count how many parts were produced per year.

- Multiply the first 2 figures.

When a company plans to produce 1 million parts, it means that each part has 0.0001% depreciation. Suppose 200,000 units were produced in the first year. Then the depreciation for this period will be 20% of the total.

Tax vs. Book Depreciation

Allocating the cost of the asset over its useful life has several purposes.

From a financial perspective, depreciation affects the net profit/loss ratio. Thus, by making a large purchase, a company reduces its net income for several years.

When it comes to taxes, depreciation is an expense that a company shows on its tax return. By doing so, it gets a deduction and reduces its final tax bill.

Accordingly, the depreciation method used has a strong impact on the financial result. With the straight line method, the company reduces its net profit evenly. With accelerated accounting, the impact of the cost of purchasing fixed assets is stronger in the early years.

In addition, there is a difference in the methods of calculating balance and tax depreciation. The first reflects real aging and takes into account the actual period of fixed assets’ use.

The second is calculated taking into account certain rules. Its value depends on the classification of the object. As a result, balance depreciation can be estimated using the straight line method, while tax depreciation is based on one of the accelerated methods.

Key Differences Between Amortization and Depreciation

There are several key differences between the concepts of amortization and depreciation. These are summarized in the table below.

| Parameter | Amortization | Depreciation |

| Object type | Intangible | Tangible |

| Method of calculation used | Almost always linear | More often, one of the accelerated |

| Accounting for the salvage value of an item | Absent | Obligatory |

| Use of subsidiary account in balance sheet | Obligatory | Optional |

The main difference between amortization and depreciation arises from the fact that these concepts are applied to different assets – intangible and tangible.

In this regard, it is possible to grasp the difference in the meaning of the terms. Depreciation is a decrease in the value of an object over time as a reflection of the real deterioration of its operational qualities. Depreciation is the gradual writing of the value of an asset off the balance. I.e. the purposes behind the application of these concepts are different.

The difference in calculation methods is also due to the different characteristics of intangible and tangible assets. The former can be realized in the future. But most of them lose a significant part of their value already in the first few years. This explains the need to take into account the salvage value and use accelerated methods of evaluation.

For example, a car on the secondary market, even when the vehicle is only a year old, will be worth considerably less than a new one from the showroom. Meanwhile, the difference in price between cars that are 10 and 11 years old is not significant.

When intangible assets are involved, the company will not be able to resell or dispose of them. This gives grounds to reduce their book value to zero.

During the entire period of use such assets do not lose their properties. For example, a patent on which products have been manufactured for 5 years is no different from one that has just been taken out. Therefore, the straight line method of calculating amortization is applied.

Depreciation vs Amortization Examples

Let us give an example of amortization by the straight line method. Suppose a company takes out a patent. The annual amount of amortization can be determined as follows.

- Determine the period for how long the item will be used. For example, 3 years.

- Divide the purchase costs (for example, $60 thousand) by the period of use (3 years). I.e. annual amortization will be $20 thousand (60/3).

- When the “object” is put on the balance, indicate its full value.

- Next year reduce it to $40 thousand (60-20).

- One year later – to $20 thousand (40-20).

- After 3 years, take the book value of the item to be 0.

When it comes to tangible objects, the calculation becomes more complicated. Here is an example of depreciation by the sum of digits method over the years of use.

The percentage by which the book value of an object should be reduced is determined as follows:

- Set the useful life of the asset. For example, 10 years.

- Add up all the digits from 1 to the specified value. For example, 1+2+3+…+10 = 55.

- Determine the percentage of the value to be written off in the first year using the formula 100*10/55. That is, the car loses 18% of its value in the first year.

- Estimate the amount of depreciation in the second year using the formula 100*9/55. I.e. the asset loses 16% of its value.

- Repeat the process for the following years. In the tenth year the formula takes the form 100*1/55.

But these steps alone are not enough. It is necessary to determine by how much of the initial costs the object will depreciate by the end of its useful life. This depends on the salvage value.

For example, a company has purchased a new truck for $200 thousand and plans to sell it after 10 years for $40 thousand. This means that during 10 years of use the value of the truck should fall by $160 thousand (from $200 thousand to $40 thousand).

Therefore, the carrying amount will decrease as follows:

- in the first year – by 18% of $160 thousand, i.e. by $28.8 thousand;

- in the second year – by 16% of $160 thousand, i.e. by $25.6 thousand;

- in the tenth year – by 1.8% of $160 thousand, i.e. by $2.88 thousand.

This assumption is rather conditional. The Company cannot predict exactly how long it will use the truck and how much it will be sold for in the future.

However, vehicles are rapidly depreciating assets. Therefore, the assumption that a truck loses much more of its value in the first year of use than in the tenth year is correct.

Below is an example of how these processes are reflected in the company’s final report.

| Apple Inc.CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (Unaudited)(In millions) | |||

| Three Months Ended | |||

| December 31, 2022 | December 31, 2022 | ||

| Cash, cash equivalents and restricted cash, beginning balances | $ 24,977 | $ 35,929 | |

| Operating activities: | |||

| Net Income | 29,998 | 34,630 | |

| Adjustments to reconcile net income to cash generated by operating activities: | |||

| Depreciation and amortization | 2,916 | 2,697 | |

| Share-based compensation expense | 2,905 | 2,265 | |

| Other | (317) | 849 | |

| Changes in operating assets and liabilities | |||

Similarities Between Amortization and Depreciation

The concepts under consideration have not only differences, but also several similarities. Both amortization and depreciation:

- reduce the carrying amount of the asset;

- spread the cost of fixed assets over the entire period of their use through gradual depreciation;

- annually recognised in the income statement even though they are non-cash expenses of the company, i.e. they do not entail actual costs.

Special Considerations

The objects used in business are diverse. They include not only tangible and intangible assets, but also minerals and other natural resources. In this case, the methods discussed above are not proper. The concept of depletion should be applied.

The essence is that the costs of organizing extraction (e.g. drilling a well, etc.) are spread over the entire period of its exploitation. Depletion can be estimated in two ways:

- interest – assigns a fixed depletion rate to a certain level of gross revenue derived from the deposit;

- value – takes into account the ratio of volumes extracted during the period to the total reserve; the calculation formula also includes the adjusted property value.

There are also types of tangible assets that cannot be devalued for tax purposes. For example, plots of land.

Another special type of company resources is loans. They are classified as intangible assets, so they are paid off. This is because the cost of borrowing does not actually decrease as the debt is repaid. I.e. the “object” does not change its properties as it is used in the same way as trademarks etc.

Amortization and depreciation when preparing the income statement are treated as non-cash transactions. The Company recognises expenses with no reference to cash flows. These concepts are introduced because they simplify capital expenditure planning. However, they reduce the company’s equity capital. This is reflected on the balance – the share of assets decreases.

How Do I Know Whether to Amortize or Depreciate an Asset?

The decision is made on the basis of GAAP. Under the general rules, intangible assets are paid off, tangible assets are devalued.

But accounting guidance provides no clear-cut answer for any situation. For example, difficulties may arise with software.

In some cases, it may be necessary to consult an expert. They will help to determine which type of asset the fixed assets at the company’s disposal should be attributed to.

Bottom Line

Both amortization and depreciation are methods of allocating the costs of various assets and property, plant and equipment over their entire period of use. This approach is fair as the company benefits from these items over a long period of time.

These concepts have many common properties. But there are also differences that prevent them from being considered synonymous. The main difference is that amortization is used for intangible assets, while depreciation is used for tangible assets. This leads to other less significant differences, for example, in the methods of calculation and the way they are recognised in financial statements.

FAQs

What is amortization in simple words?

It is the gradual reduction in the value of an intangible resource on the balance. This is to spread the cost over the period that the company will earn a profit from the asset.

What is the difference between depreciation and amortization and depletion?

The concept of amortization is used only when referring to intangible assets. Tangible assets cannot be paid back. They are subject to depreciation and devaluation.

How do you separate depreciation and amortization?

Determining whether an asset should be depreciated or amortized can be made using the guidance provided in national accounting standards.

Is software depreciated or amortized?

There is no unambiguous answer to this question. Many companies account for software on their balance as a type of fixed asset. Therefore, it is charged with depreciation, not amortization. But for this to be possible, the software must meet a number of requirements. When it fails to meet them or was acquired for research and development purposes, the concept of depreciation cannot be applied.

You Might Also Like

- What Is Dividend Yield? A Complete Guide to Calculation and Interpretation

- How to Calculate Dividend Yield: A Step-by-Step Approach for Investors

- What Is a Dividend Yield? Understanding This Key Investment Metric