Table of Contents

Definition of Net Interest Income (NII)

Net Interest Income (NII) denotes the disparity between a bank’s aggregate interest income derived from loans, securities, and diverse interest-generating assets and the cumulative interest expenses paid out on deposits and other interest-bearing liabilities. This financial metric acts as a pivotal measure of a bank’s profitability rooted in its interest-driven operations.

Interest revenue, constituting earnings from loans, bonds, and similar interest-generating assets, forms a significant portion of NII. Conversely, interest expenses embody the costs associated with interest payments on deposits, borrowings, and liabilities.

NII calculation involves subtracting the total interest expenses from the total interest income, revealing the net earnings derived purely from the bank’s interest-oriented endeavors.

Various factors influence NII, notably the composition of the bank’s portfolio encompassing both variable and fixed-rate instruments. Variable rates susceptible to market fluctuations and credit risks associated with loans and securities influence interest income and expenses. Moreover, prevailing economic conditions, including interest rate fluctuations and overall economic dynamics, significantly impact NII.

Banks actively manage NII by adjusting their asset and liability mix, assessing risk factors, and implementing strategies to navigate changes in economic conditions or interest rate fluctuations.

Importance and Use of Net Interest Income Metric

Net Interest Income (NII) stands as a crucial performance measure for banks, especially amid fluctuating interest rates. It reflects a bank’s earnings from interest-bearing assets after deducting interest expenses, offering insights into loan quality and interest rate risk management. NII plays a pivotal role in assessing overall profitability, aiding investor analysis and stock performance evaluation. By analyzing NII, stakeholders gauge a bank’s ability to generate income from its core lending and investment activities, making it a fundamental indicator for comprehending a financial institution’s fiscal health amidst varying economic conditions.

Interest Rates in the Economy and NII

We can analyze financial indicators that influence NII among FDIC-insured organizations.

- Net Income: The net income of commercial banks and savings institutions insured by the FDIC decreased by $9.0 billion (11.3 percent) to $70.8 billion in the second quarter of 2023. This decrease may impact interest income, as reduced profit might signify a decrease in net interest income.

- Non-interest Income and Provision Expenses: It was noted that the decline in net income was due to a reduction in net interest income and an increase in provisions. This suggests that besides interest income, other revenue and expenses like non-interest income, securities gains or losses, and reserves for potential losses can impact NII.

- Return on Assets (ROA): The ROA stood at 1.21 percent in the second quarter of 2023, which could serve as an indicator of the efficiency of utilizing assets to generate profit. A higher ROA might indicate a higher Interest Income, showing more effective asset utilization for income generation.

- Net Income of Public Banks: Public banks witnessed a 3.4 percent increase in net income in the second quarter of 2023. This might imply an uptick in non-interest income, which can significantly contribute to overall NII.

- Deposit Insurance Fund (DIF) Indicators: Growth in the DIF balance and its components such as estimated income, net investment income, and operational expenses might signal changes in the financial health of the banking system, potentially impacting NII through various channels.

Formula to Calculate Net Interest Income (NII)

The formula to calculate Net Interest Income (NII) involves two components. Interest revenue, derived from the effective interest rate multiplied by the total gross carrying value of interest-earning assets (like loans and securities). Interest expenses, determined by the effective interest rate multiplied by the total gross carrying value of interest-bearing liabilities (such as deposits). The formula subtracts interest expenses from interest revenue to obtain Net Interest Income. It can be expressed as:

Interest Revenue = Effective Interest Rate × Total Gross Carrying Value of Earning Assets

Interest Expenses = Effective Interest Rate × Total Gross Carrying Value of Interest-Bearing Liabilities.

This calculation quantifies the income generated from interest-earning activities after subtracting the associated expenses.

Example Net Interest Income Calculation

Let’s consider Bank X with a diverse loan portfolio comprising mortgages, personal loans, and business loans. The interest revenue is calculated by multiplying the effective interest rate (5%) by the gross carrying value of earning assets ($500 million). Meanwhile, interest expenses are determined by multiplying the effective interest rate (2%) by the gross carrying value of interest-bearing liabilities ($300 million). Consequently, the interest revenue amounts to $25 million, while interest expenses total $6 million. Hence, Bank X’s Net Interest Income (NII) is $19 million.

Residual income = Net income – Expenses on equity.

To illustrate variance, we compare Bank X’s NII with other leading banks. Bank Y, with a similar loan structure, reports an NII of $22 million, while Bank Z, predominantly focused on corporate lending, shows an NII of $15 million. These comparisons highlight the varying NII among banks due to differences in loan structures and interest rate management strategies.

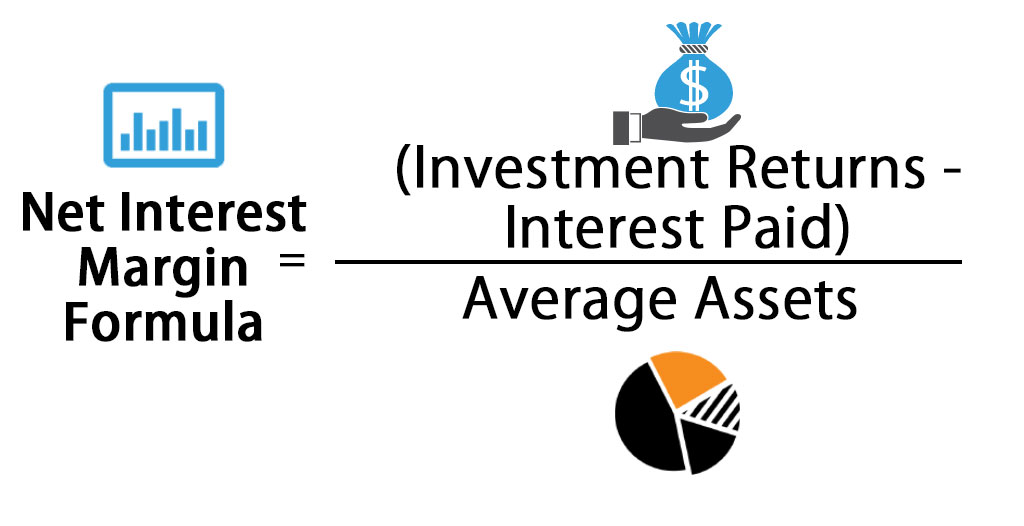

Net Interest Margin (NIM) Formula

The Net Interest Margin (NIM) is computed by dividing Net Income by the average total interest-earning assets. This formula yields the NIM percentage, a standardized metric enabling historical comparisons and assessments against industry peers. The NIM indicates a financial institution’s efficiency in generating income from its interest-bearing assets relative to the average asset base.

Factors Influencing Net Interest Income

Specific factors influencing Net Interest Income (NII) can be illustrated as follows:

🔹Variable Rates: Consider a bank holding a portfolio of loans with variable interest rates. If market rates increase, the interest on these loans will also rise in interest, augmenting the bank’s income. Conversely, if rates decrease, income from these assets will decrease as well.

🔹Rate Spreads: Suppose a bank offers mortgage loans at a rate of 5% while collecting deposits at a rate of 2%. The rate spread is 3%. The wider this margin, the higher the bank’s Net Interest Income.

🔹Non-Performing Assets (NPAs): If the bank holds loans where customers default and these are classified as NPAs, it will reduce the bank’s income due to lost interest or principal on these loans.

🔹Default Rates: An increase in the percentage of customers unable to repay their loans (default) can lead to higher losses for the bank due to reduced interest or principal repayment.

For example, if a bank holds a $22 million mortgage loan portfolio at 4% interest per annum and pays 2% on deposits, providing a 2% interest rate differential. If the bank can increase this differential by 0.5% by changing the terms of the loans or attracting deposits at higher rates, this will increase net interest income.

However, if the default rate in this mortgage loan portfolio increases from, say, 1% to 3%, the bank may experience an increase in losses due to non-performing loans, resulting in lower net interest income, and their net income would only be $880.

Special Considerations

Net interest income, though pivotal, isn’t the sole determinant of bank profitability. Considerations beyond NII, such as expenses, ancillary revenues, and the broader financial landscape, play a crucial role. Non-interest expenses and diverse revenue sources are integral in assessing overall profitability. Evaluating the complete spectrum of profit and loss elements is essential for a comprehensive understanding of a financial institution’s profitability.

Conclusion

In conclusion, while net interest income serves as a significant metric for performance evaluation, true profitability hinges on a holistic view that includes non-interest income and expenses. To grasp the complete financial health of an institution, it’s imperative to consider all profit drivers comprehensively. Evaluating not just the interest earnings but also other income sources and expenses is essential for a more accurate assessment of overall profitability.

Frequently Asked Questions (FAQs)

The authors bring a wealth of experience and expertise in the finance industry, with backgrounds spanning banking, financial analysis, and investment management. Their combined tenure of over two decades includes roles in leading financial institutions, academic contributions in finance-related research, and practical insights shared through publications and seminars. Their extensive knowledge establishes credibility in addressing financial queries and providing nuanced perspectives on diverse financial topics.

Is net interest income the same as NIM?

Net Interest Income (NII) represents the difference between interest earned and interest paid, while Net Interest Margin (NIM) is a percentage calculated by dividing NII by average interest-bearing assets. They’re related but not the same; NIM measures NII relative to assets.

What is a good NIM for a bank?

A good Net Interest Margin varies by institution and economic conditions. Generally, a higher NIM indicates better profitability, but an ideal figure depends on the bank’s business model and risk profile.

What are NPAs?

Non-Performing Assets (NPAs) refer to loans or advances that have stopped generating income for the lender. They typically include loans where interest or principal payments remain overdue for a specified period.

Which factors can affect the net interest margin of a bank?

Factors impacting Net Interest Margin include changes in interest rates, asset quality, loan-to-deposit ratios, funding costs, and overall economic conditions.

How do non-performing assets (NPAs) affect interest income?

NPAs can significantly impact interest income as they lead to reduced interest earnings or write-offs due to defaults or non-repayment of loans, affecting the overall profitability of a bank.

How to analyze net interest margin?

Analyzing Net Interest Margin involves reviewing interest-earning assets, interest-bearing liabilities, and their associated rates. Comparing NIM over time and against industry benchmarks aids in understanding a bank’s performance.