Table of Contents

Understanding Real Costs Of Investments

Investing Fees To Be Aware Of Before You Invest

Most investment services and trading platforms charge investment fees and costs. The key ones are brokerage and custodian fees used by brokers and retirement accounts. All mutual funds charge expense ratios paid out from portfolio returns.

So before you even start investing, you need to study offers by different mutual funds, banks, and brokers. Look for investment products with the lowest costs. To increase your return on investment, you’d better understand how much total fees you will pay for share purchase and account maintenance.

Expense Ratio Or Internal Expenses

Management of exchange-traded funds (ETFs) and mutual funds requires financial expenses. Typically, the expense ratio is paid out from the net assets of the fund. Thus, the investor’s final profit is somewhat less: an ETF’s return is 10% with an expense ratio of 1.7% — at the end of the day, an investor in this ETF would earn an 8.3% investment return on his shares.

The expense ratio is not deducted from the account of each individual investor. It is withheld from the returns generated by the fund, which could have been reinvested and thus increased the net assets of a fund.

The total annual costs of a fund’s expenses are called the expense ratio. The expense ratio is clearly stated in the fund’s founding documents. It is expressed as a percentage of the total net asset value.

For example, if a mutual fund has $1 million in assets under management and the expense ratio is 0.5%, $5,000 is spent annually to keep it running.

This amount decreases the value of net assets evenly throughout the year. It includes the following expenses:

- management team’s salaries;

- expenses for maintaining the functioning of the company (software providers, commercial office rents, marketing expenses, utilities, etc.);

- payment for depositary services and other administrative expenses.

It is important to understand that these annual fees, including payment to the fund manager, are withheld from investors’ returns and reduce the net asset value of the fund if the used investment strategy makes a loss and the share price falls.

Investment Management Fees

Investing costs depend on a number of factors. The main one is the investment strategy. The costs of actively managed funds are usually higher than those of passively managed funds that simply follow an index. Even lower fees are usually found in exchange-traded funds.

Another factor that affects the cost of a mutual fund is the type of assets in which it invests. For example, a fund that pools stocks from the SP500 will charge lower fees than a fund that focuses on exchange-traded commodities, etc.

A third important factor affecting the expense ratio is the total net asset value. Some components of a mutual fund’s expenses are fixed. In addition, a company that manages significant capital can get the services it needs on more favorable terms, etc.

Therefore, funds with higher net asset values tend to have lower expense ratios as a percentage of total assets than small investment companies.

As a result, expenses for a mutual fund with an active strategy investing in equities can be as high as 2% or even higher. For an exchange-traded, passively managed fund investing in US bonds or stocks, that figure drops to 0.02%.

Below are examples of equity ETFs with low management company expenses.

| ETF (Ticker) | Management fee | Index Tracked |

| JP Morgan BetaBuilders U.S. Equity ETF (BBUS) | 0,02% | Morningstas US Target Market Exposure Index |

| Vanguard Total Stock Market ETF (VTI) | 0,03% | CRSP U.S. Total Market |

| iShares Core S&P Total U.S. Stock Market ETF (ITOT) | 0,03% | S&P Total Market Index |

Advisory Fees Explained

An investor who has no time or necessary skills to create an investment strategy for personal use, but rather seeks out help from financial advisors, will have to pay additional costs. Usually, advisory fees are charged once a quarter.

The average management fee is 1% of the capital managed by a financial advisor. For small portfolios, this figure can go up to 2%.

If it is a large portfolio (above 1 million USD), advisory fees may exceed 1% only if they include complex investment services, such as tax planning, wealth management, etc.

If the strategy recommended by the financial advisor includes ETFs or mutual funds, an investor may end up paying double or even triple the fee:

- the management fee of the chosen mutual fund, charged annually by the investment firm that runs the fund;

- the cost of a financial advisor who manages the investor’s capital and recommends mutual fund investments;

- the purchase fee (front-end load) or the exchange transaction fee for the purchase of an ETF.

A good way to save on the services of a professional investor is not to put your assets under permanent management, but to seek one-time advice. For example, a beginner investor can buy professional advice on how to create a retirement plan.

A one-time consulting session can cost from $700 to $3500, depending on the scope and assets involved. But usually, it is not tied to the size of the investor’s capital.

Understanding Transaction Fees

When trading independently on an exchange, investment costs always include a transaction fee. This is the broker’s fee for facilitating the trade through the platform.

Such commission may be expressed as a percentage of the transaction amount. But more often a broker establishes a flat fee for placing each buy and sell order. Also, brokers can specify a minimum threshold below which the cost of order execution may not fall.

The transaction fee will be a fraction of a percent for a large trading volume. But with small capital, the fee charged when buying and selling stocks and bonds can affect the final investment returns.

The average flat fee is $5-30 per transaction, depending on the broker.

There are already enough discount brokers who do not charge commissions for online transactions at all or at certain service rates. Robinhood was the first to give it up, followed by such companies as Interactive Brokers, Charles Schwab, etc.

On top of the brokerage fees, an exchange commission can be charged. This is the remuneration of the trading floor where the transaction is executed. In the US, transaction fees often include the SEC fees that brokers pay to the US Treasury for access to the regulated stock exchanges.

This fee may be as high as $0.005 per share. But at most exchanges, it is not charged for all transactions but only for those that reduce market liquidity.

Eventually, these investment expenses are partly or fully passed on by brokers to retail investors. Under the terms of the contract, they can either be included in the transaction fee or charged additionally.

Loads & Commissions

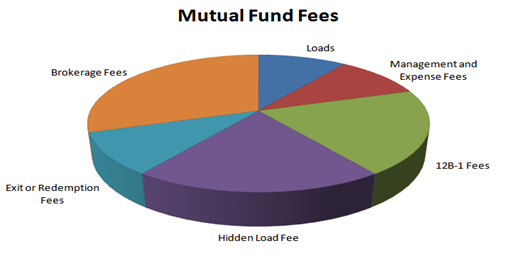

The investment cost of investing in mutual funds is not limited to an annual management fee.

When an investor purchases mutual fund shares, he or she must pay an amount in excess of their estimated value. The difference between the client’s investment and the fair price of the securities acquired is sometimes called the initial charge (front-end load).

This fee is charged once and is the fee of a salesperson who sells shares of managed funds. Its size varies from 3.75% to 5.75% of the invested amount depending on the performance of the fund.

Retail investors do not pay load fees when investing in passively managed index funds (ETFs).

It is also possible to find mutual funds that have waived front-load commissions.

A redemption fee is a fee that is withheld from a mutual fund client when the shares are sold. Depending on an investment vehicle, redemption fees can also be called exit fees, back-end load, or a surrender charge. If an investor decides to cash out early, the insurance contract is terminated prematurely. The insurance company will have to find a way to return its commissions — often it is an investor who pays all kinds of redemption fees.

The amount of this fee is tied to how long and how often an investor trades. During the first year, redemption fees may be up to 5% of the total value of the shares, and then the back-end load gradually decreases over time.

In the case of ETFs, there is no such fee. Shares of exchange-traded funds can be bought and sold every day with no additional fees. The only costs deducted from the investor’s account are transaction fees and income taxes on the profits from the transactions.

What Are Custodian Fees?

Investment costs include another regular fee that is charged for the service of the IRS reporting regulations, as well as for the accounting of transactions, dividends received, 401(k) fees, etc.

Custodian fees are withheld both from investors who trade stocks and exchange-traded funds, and from those who put money under the management of mutual funds and in various retirement accounts.

This fee can be as high as $90 yearly for standard accounts and $80 for retirement plans.

Such fees are usually reduced if a person uses an investment advisor offered by the company where the securities account is held.

In addition to the annual fee and custodian fees, another fee may be withheld at the time the account is closed. Its average size is $25-150.

Annual Account Fee

Often brokers may charge an account maintenance fee. This happens when an investor has not made the agreed amount of transactions in a given period for the operating expenses to cover the minimum investments costs stipulated in the contract.

Mutual funds also have the right to charge such a commission if the investor’s investments are below a certain threshold. It may also be applied to maintain certain retirement plans.

Frequently Asked Questions

Video: https://www.youtube.com/watch?v=NAKcMTsEVnU

What type of investment should I use to keep commissions to a minimum?

The most effective way to keep investment costs to a minimum is to pick individual stocks and bonds yourself and buy them through an online broker.

But this involves additional time and requires an in-depth understanding of the stock market. At the same time, this approach does not guarantee a higher return on investments. The investor may experience asset depreciation events due to market volatility and/or risky portfolio allocation.

To reduce the cost of commissions in passive investing, you need to forgo investing in mutual funds and choose low-cost exchange-traded funds.

Is it possible to reduce taxes at the expense of commissions?

All investing fees are not tax-deductible. Tax deductions related to investment expenses were frozen in 2018. This is covered by the Tax Cuts and Jobs Act.

That law is in effect until 2025. Therefore, there is a tiny possibility that the tax deduction for investment-related expenses will be returned in 2026.

What is the true impact of costs & fees on investment returns?

An investor’s annual return is influenced not only by the strategy executed but also by external factors such as:

- a regular management fee, which is charged if there is a financial advisor involved in portfolio management;

- costs of mutual funds, if this type of investment vehicle is used;

- transaction fees, sales loads commissions;

- custodial fees for assets in retirement accounts, etc.

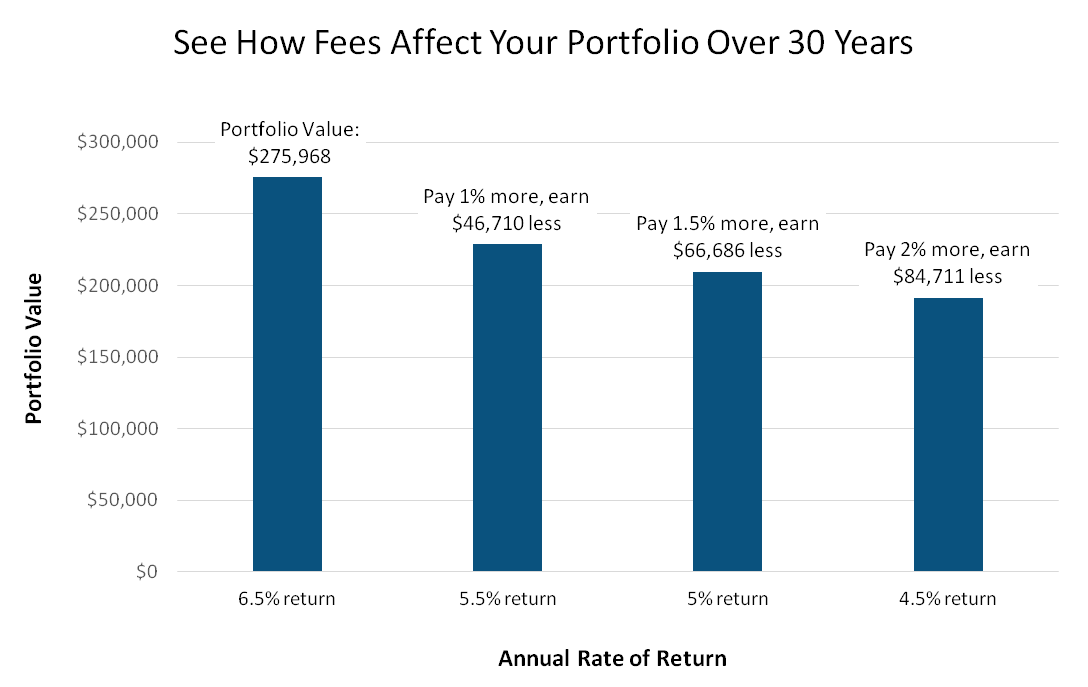

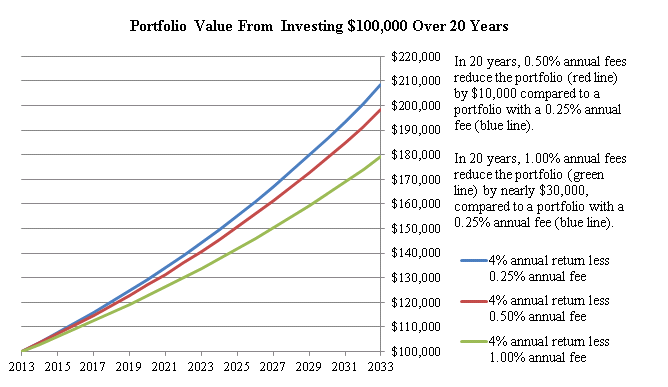

Here is an example with real numbers. Imagine an investor Adam who invests $10,000 in assets that consistently return him 5% per annum for 35 years.

With no fees, even without additional replenishments, the final amount in his account will be $55,160. And if you extend the investment period to 45 years, the overall return grows to $89,850.

If Adam’s portfolio is a single mutual fund investment, which retains 0.5% of capital per year, the actual yield drops to 4.5%.

As a result, without regular annual reinvestment, Adam will only get $46,673 after 35 years. And after 45 years Adam’s portfolio will grow to $72,482.

It turns out that a modest commission of 0.5% over 35 years “eats up” about 15% of total income, and over 45 years — more than 19%. And there are actively managed funds that have expense ratios of 1% or more.

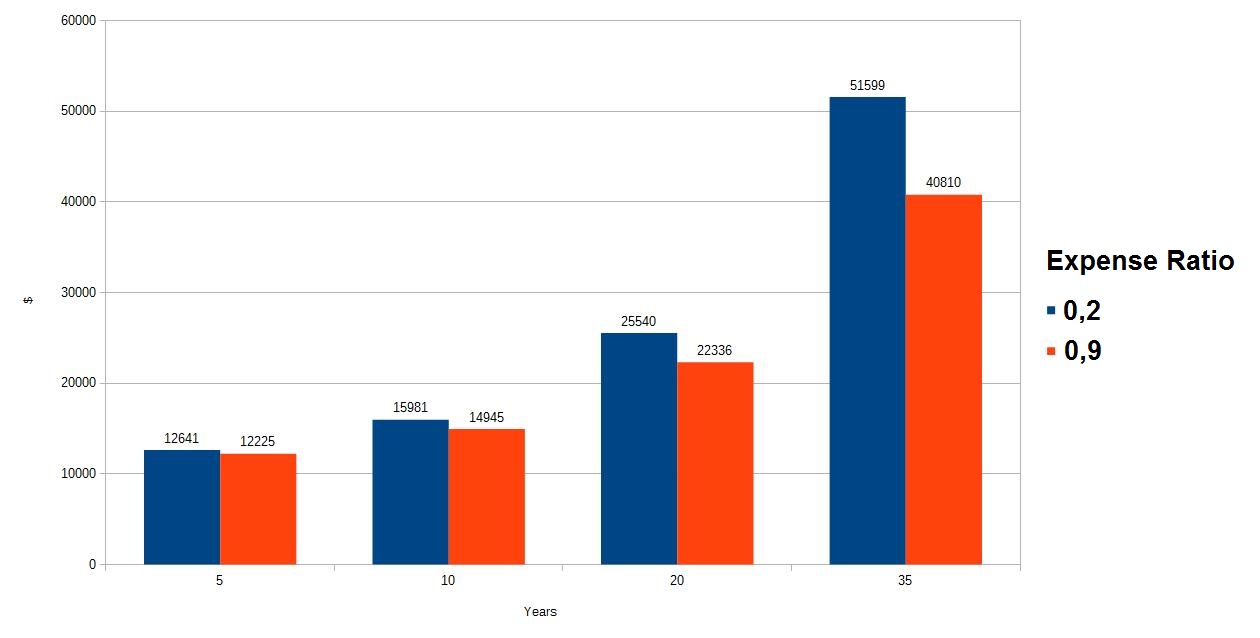

To illustrate how an investor’s capital will change over the years, if he invests $10.000 in mutual funds with an expense ratio of 0.2% and 0.9% of the net asset value. The average annual return of each fund is taken as 5%.

You can use investment calculators to make these calculations on your own, taking into account your situation (investing goals, starting capital, planned investment time horizon, and specific fees for each investment product).

When transaction fees, custodian fees, advisory fees, and costs associated with buying and selling mutual fund shares are factored in, the effect of fees becomes even more impressive.

What can I do to eliminate commissions from my investment strategy?

There are two areas in which you can reduce your investment costs.

The first one is to carefully study the terms & conditions clauses of selected funds, and search for brokers/investment firms with the most favorable costs. It means that investors should:

- invest in index ETFs instead of an actively managed mutual fund;

- when choosing mutual funds, avoid firms that charge front-end load and redemption fees;

- trade independently through an online broker with minimal transaction fees instead of consulting an individual financial advisor;

- look for brokers that do not charge inactivity fees, hidden annual costs, custodian fees, etc.

The second way to reduce investment costs is to use a passive “buy and hold” strategy. Most beginners who try to make money by active day trading end up with an avalanche of investment costs and a pile of realized losses.

Constantly switching mutual funds in an attempt to find a slightly higher yield option makes no difference.

Investing costs are inevitable. However, patience and attention to detail can reduce most fees. Managing investing costs responsibly is the best way to understand where your money is going and how to improve your investment returns.

You Might Also Like

- What Makes a Dividend Qualified? IRS Rules Explained

- Understanding Forward Dividend Yield: The Complete Guide

- High-Yield Dividend Aristocrats: Top Stocks for Consistent Income

- APY vs Dividend Rate: Which Matters More for Your Returns?